.jpg)

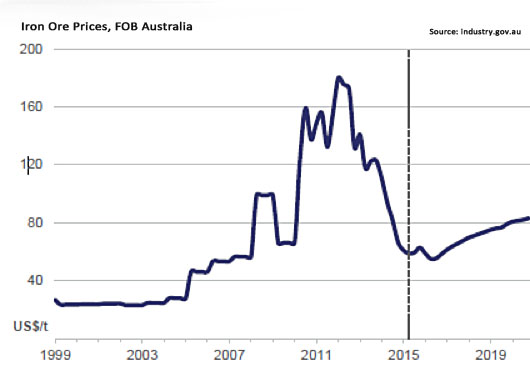

The Gold Report: You recently wrote a paper called "Stagnation: The New Paradigm?" where you put current commodity prices in perspective by showing charts going back to 1999. What happened over the last five years in iron ore and copper and what can we expect going forward?

Raymond Goldie: The price of iron ore from 2011 to 2015 dropped more than 70%. If you look at the other great indicator of the mining industry—the price of copper—you find a similar, but smaller, decline over the same time period.

[Copper chart located above. Data: London Metal Exchange.]

TGR: What were the fundamentals both behind iron ore and copper's astronomical moves up going back to 2004 and the subsequent falls?

RG: Iron ore prices really started to rise in 2008 because of increasing demand for infrastructure needs globally. Copper received added attention in China as it became seen as money right alongside gold. Chinese bankers started using copper, especially for foreign trade financing, which helped push copper prices up to levels that may not have been sustainable.

In both cases, the main reason for the following shift down was that supply had increased faster than demand.

Both iron ore prices and copper prices are, even at their relatively depressed levels today, higher than any price that they'd ever seen before 2006.

TGR: The continuing trend lines that you have on both iron ore and copper in these charts show slow, steady growth going forward. What prices are you expecting in 2016 and beyond?

RG: One of the things I've learned is that I'm not particularly good at forecasting prices. The forward strip markets, the futures prices on the London Metal Exchange, incorporate the aggregate of expectations and are better at forecasting prices. That seems to be calling for a steady increase in copper prices over the next 10 years.

"Trevali Mining Corp. is one of the best zinc plays."

In the case of iron ore, there is no forward strip market, so I relied on the Australian government forecast. We're at a pretty flat bottom now and the best estimate is a steady increase in iron ore prices.

TGR: What would steadily increasing commodity prices mean for the commodity equities market?

RG: That's a very good question—how strong is the relationship between commodity prices and commodity equities? One of the answers is that stocks of companies that produce copper, like Freeport-McMoRan Copper & Gold Inc. (FCX:NYSE), the biggest one, and some of the smaller producers—the biggest one in Canada is First Quantum Minerals Ltd. (FM:TSX; FQM:LSE)—follow the larger equity market closer than the commodity prices.

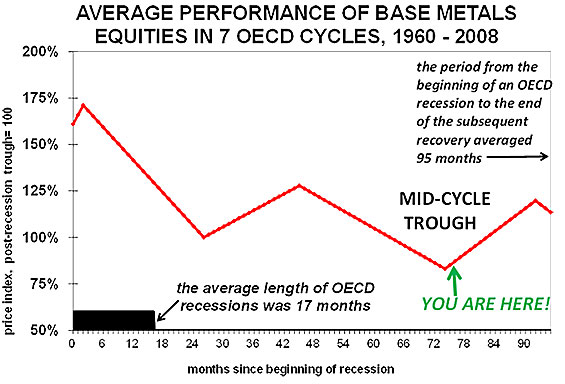

One of the charts that I've put together shows the relative performance of the Toronto Stock Exchange diversified mining index against the overall Toronto composite index. It shows seven clear economic cycles since 1960. In every one of those cycles, equities have experienced two peaks and two troughs. One of the peaks happens as you recover from the end of the recession. Then in the middle of each cycle, those equities tend to languish and decline and form a second trough, finally running up to the cycle end peak. I believe we are at the middle of one of these mid-cycle peaks right now.

Source: TSX data, analysis by Salman Partners Inc. The index is of non-precious metals equities' performance relative to that of the TSX Composite, recalculated to 100 being the low point in each cycle immediately after the end of the recession that began each cycle.

Source: TSX data, analysis by Salman Partners Inc. The index is of non-precious metals equities' performance relative to that of the TSX Composite, recalculated to 100 being the low point in each cycle immediately after the end of the recession that began each cycle.

TGR: Is there anything different about this cycle than the previous cycles? Is it acting as predicted?

RG: Many have said we are experiencing uncommon demand, but if we look at the Western world's demand for base metals in this cycle compared with some of the previous cycles, we find that the trend of the line for demand has been pretty much in the middle of previous cyclical trends. Even China's export data is, on average, sideways. There may, indeed, be strong growth in China in demand for copper, but there's also been strong growth in production of copper in China. The net result is that China's impact on the rest of the world copper market is pretty flat. So it's not a demand story.

I think it's a supply side story that is resulting in copper prices that are stronger than at any time before 2006.

TGR: What is causing the lack of supply and will that continue?

RG: At the beginning of every year, copper mining companies publish their production goals, and typically up to 2005, they achieved that. One of the ways they did that is by tucking away some high-grade ore so they could kick up the pounds if needed at the end of the year. But since 2005, the world's copper industry has consistently produced 7% less copper than planned. One of the reasons we've had these shortfalls is that those areas of high-grade ore don't exist anymore. They've been mined out.

That is why we have a supply side issue at existing mines. When it comes to building new mines, not only are we not finding sparkling new copper deposits at the rate we used to, but also it takes longer to get mines into production—12, 15, 20 years—because of new environmental compliance regulations.

That is why this isn't a typical cycle. This is a cycle constrained by government compliance and governmental regulations.

TGR: Can the junior companies fill that demand in the coming cycle?

RG: Many juniors have superb projects, but they're lacking financing. Banks generally want to lend to big companies. So the juniors are sitting, waiting to be taken over or engage in a joint venture with a big company. But big company shareholders often do not want to see their companies underwriting big new expansion projects. They'd rather see that cash returned to them.

TGR: What are the companies that have some money to move projects ahead?

RG: First Quantum has become a big company by growing internally and through the recent takeover of Inmet Mining Corp. That big company interest will allow Cobre Panama to come on stream roughly as planned.

NovaCopper Inc. (NCQ:TSX; NCQ:NYSE.MKT) has an equally good project. In fact, it's smaller and higher grade. It's in Alaska, which many people would consider to be a more stable jurisdiction than Panama, but it can't yet get full financing. The project continues to be studied and permitted, but we don't have the financing to bring it all the way through to production yet. The company has managed to get enough interest from investors that it's staying alive, but it doesn't have financing all the way through to production.

Nautilus Minerals Inc. (NUS:TSX) is a small company, but it was able to find financing, largely through partnering. One of those partners is the government of Papua New Guinea, which is in for 30% of that project at the bottom of the ocean off the country's coast. That has provided enough financing to move the project all the way through to production.

TGR: Has Nautilus answered the risk question associated with underwater mining and proved it can be economical?

RG: Nautilus is merging mining technology and deep ocean oil and gas drilling technology. I have confidence that the engineers have figured out a way to make it work.

TGR: Are you following other copper companies?

RG: Reservoir Minerals Inc. (RMC:TSX.V) has a joint venture with Freeport-McMoRan, which has named Reservoir's Timok Project in Serbia as one of its top priorities. This is a country that has been wracked with war; only recently has there been calm. The political instability resulted in a lack of new technology used to explore ore deposits in a seasoned mining area. The Timok project combines a known occurrence of large, high-grade ore deposits with modern exploration methods to find some humdinger resources. The company is working on permitting and engineering in preparation for raising final financing.

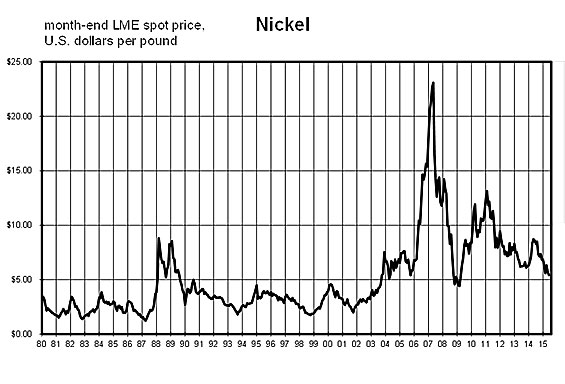

TGR: Is nickel following the same pinch-point curve™* as copper?

Source: London Metal Exchange

Source: London Metal Exchange

RG: Nickel is also in a mid-cycle low, something that occurs well before the end of an economic cycle. As long as economic growth continues, we will see a recovery in the price of commodities that relate to that recovery. Nickel is one of them. In fact, I'm more optimistic about nickel than most other commodities because it is a supply side story. The demand is growing fairly consistently at about 4% or so a year.

The supply side issue is that in January of 2014, the government of Indonesia, the Saudi Arabia of nickel, banned exports of raw nickel as part of a move to producing finished nickel. China had been making lots of cheap nickel from this high-grade Indonesian ore and stocked up before the door shut. We're not quite sure when the Chinese will run out of that ore, but it's almost certainly before the end of this year. Once that happens, a shortfall of 200,000 or 300,000 tons a year could push the price up from the current $5 a pound ($5/lb) range to something more like $11, 12 or 13/lb. Remember, the price of nickel got into the $20/lb neighborhood in 2007.

TGR: What junior companies do you follow in the nickel space?

RG: Royal Nickel Corp. (RNX:TSX) and Sherritt International Corp. (S:TSX) are covered by my colleague, Nik Rasskazovskiy. What's driving the price of both companies is the nickel price. Royal Nickel has a project in Quebec and is looking for a big brother to help develop it. Sherritt is North America's go-to play on nickel. It has operations in Cuba, Canada and Madagascar and is one of the world's lowest-cost producers of nickel. Once we see confirmation that the Chinese have run out of Indonesian nickel ore, nickel prices will turn up, and then we could start to see joy in the share prices of Sherritt and Royal Nickel.

TGR: Looming supply challenges have been reported in the zinc space. What is your outlook in that market?

RG: A few months ago a lot of investors noticed that many of the big world zinc mines are closing down. Some speculated we were running out of zinc and that the price might go from the current $0.91/lb to as high as $2/lb in a couple of years. The problem is that because of that prediction, a lot of production—particularly in China, Peru and at Vedanta Resources Plc's (VED:LSE) projects in Africa and Asia—ramped up fast. The net result is the price of zinc isn't $2/lb. It's about $0.91/lb and likely to stay in that range for the next few years.

TGR: Are there junior companies that can still be successful?

RG: Trevali Mining Corp. (TV:TSX; TV:BVL; TREVF:OTCQX) is one of the best zinc plays. It has a joint venture with Glencore International Plc (GLEN:LSE), the world's biggest zinc producer and trader. Also, it has mines in Peru and Canada, so it's already in production. Better yet, that production is low cost.

Zazu Metals Corp. (ZAZ:TSX) is an Alaskan play on a zinc deposit that, fortunately, can make money at $0.94–0.95/lb. But it needs a big brother.

TGR: Do you have any words of wisdom that can help investors re-engaging with the market as the summer comes to a close?

RG: We have seen the bottom in copper. We are still waiting for the bottom in nickel, and zinc could be a couple of years out. I would focus on copper equities. Start with the big, liquid copper producers. That used to mean Freeport McMoRan, but it also now has huge interests in oil and gas. I have really no idea what's going to happen to oil and gas prices in the foreseeable future. So I turn to First Quantum, which is Canada's go-to copper play. This is probably the best performer among base metals equities between now and the end of this year. Looking out further will be the time for other junior copper plays and then later, nickel, and even later, zinc.

TGR: Thank you for your time.

*Pinch-point curve™ is a term trademarked by Raymond Goldie.

Raymond Goldie, vice-president of commodity economics and senior mining analyst at Salman Partners, has extensive experience in the investment business, including more than 20 years as a mining analyst covering non-precious-non-ferrous and precious minerals (gold, silver, PGEs, diamonds) and fertilizer companies. In geology, Goldie holds a Bachelor of Science from Victoria University in Wellington, New Zealand; a Master of Science from McGill University; a Ph.D. from Queens University; and a Diploma in Business Administration from the University of Toronto.

Read what other experts are saying about:

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) JT Long conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report and The Life Sciences Report, and provides services to Streetwise Reports as an employee. She owns, or her family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Trevali Mining Corp. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Raymond Goldie: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.