The Mining Report: This year we've seen a modest rally for specific rare earth elements (REEs), namely terbium, dysprosium, praseodymium and neodymium. Has this bolstered the near-term outlook for rare earth exploration and development projects outside of China?

Ryan Castilloux: It has. The recently announced supply agreement between Molycorp Inc. (MCP:NYSE) and Siemens AG (SI:NYSE) is a reflection of how the outlook is improving. The rally we saw earlier this year is an indication that markets for certain rare earth elements are becoming increasingly tight. Without a boost in global production to meet growing global demand, we will see continued strength behind magnetic rare earth prices and several others.

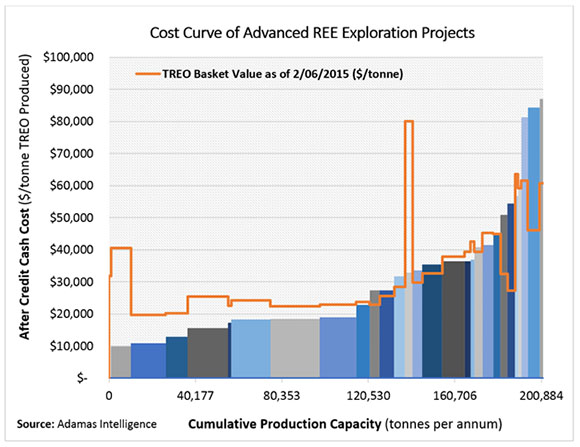

"Namibia Rare Earths Inc.'s Lofdal has relatively low preproduction capital requirements."

Until a few weeks ago the Chinese FOB price of terbium oxide was up nearly 50% year-to-date and dysprosium oxide and neodymium oxide were up about 30%. Prices for these oxides have since given up some of their gains as a result of slow buying ahead of China's upcoming export tariff changes, but I expect the prices of these rare earths will resume their upward momentum once buying resumes midyear. Exasperating the future supply/demand imbalance of certain rare earths is China's continued effort to suppress unregulated rare earth production, particularly in China's heavy rare earth-rich southern provinces, which will result in declining global production of terbium, dysprosium, yttrium and other heavy rare earths if new sources of supply don't come onstream.

TMR: Do you think this will spur much investor interest?

RC: The rally in the early part of 2015 pushed a lot of marginal projects into the economically attractive category, but with the volatility that we've seen in recent years we need to see prices not only rise, but maintain a level that will restore investor confidence. We're not likely to see investors flood back into the market in the near term. We need to see sustained support at these prices, perhaps even a rise moving forward.

TMR: With sparse amounts of investment capital entering the REE space, how are these tiny companies creating value?

RC: In many cases there's been a shift from creating external value through things like exploration drilling, defining larger resources and identifying high-grade zones, which are generally capital intensive activities, to creating greater project value internally through improved flow sheets, innovative processing methods and other means that boost margins at relatively low costs.

TMR: What are three or four projects that continue to advance despite a stagnant market?

RC: As many as 20 projects continue to make tangible headway despite the tough economic conditions of recent years. Among those that have recently issued major announcements are Tasman Metals Ltd. (TSM:TSX.V; TAS:NYSE.MKT; TASXF:OTCPK; T61:FSE), Northern Minerals Ltd. (NTU:ASX), Greenland Minerals & Energy Ltd. (GGG:ASX) and Namibia Rare Earths Inc. (NRE:TSX; NMREF:OTCQX).

TMR: Let's start with Tasman.

RC: In January Tasman announced results of a prefeasibility study for its Norra Kärr project in Sweden. That study proposed a 20-year initial mine life, producing around 5,000 tonnes of rare earth oxides yearly, including more than 200 tonnes of dysprosium oxide. These rare earths will be contained in a mixed REE concentrate product that Tasman will look to have toll separated by a third party. The initial capital required for Norra Kärr development is under $400 million ($400M), which is a plus considering Norra Kärr's relative richness in heavy rare earth elements (HREEs) versus lights. What's also a plus is the project's proximity to existing infrastructure, Solvay's processing facility in La Rochelle, France, and European end users, particularly in Germany.

TMR: How has Tasman factored in the cost of that third-party processor and are there any negotiations underway with a particular party?

RC: Tasman is undoubtedly talking with several potential processors and it is likely looking close to home, which would be Solvay's La Rochelle facility. As for toll separation costs, typically companies take the anticipated revenue from REE production and deduct from that revenue the anticipated toll-processing costs. Essentially, they're skimming toll-processing costs off of future revenue. That allows a company to keep on-paper operating costs looking better. Tasman, however, has taken the responsible approach and incorporated its toll-processing costs into its cash cost structure in its prefeasibility study. Tasman is recognizing that toll processing is a cost it is incurring on its value chain from ore to final product, but other companies generally ignore that. On paper, Tasman's cash costs versus similar projects are seemingly higher, but when you look at those fine details you see that it all comes out in the wash.

TMR: Does Siemens' deal with Molycorp preclude a deal with Tasman or any other emerging rare earth recovery (REO) producers?

RC: Not necessarily. The Siemens/Molycorp 10-year deal announcement didn't discuss any specific numbers for offtake tonnage. It's my understanding that Siemens had a previous deal with Lynas Corp. (LYC:ASX) that is still alive. It could just be that Siemens is looking to diversify its supply sources.

TMR: Tell us about Northern Minerals.

RC: Northern Minerals has also been plowing ahead with its Browns Range HREE project in Australia. In October 2014 it announced an increased mineral resource, as well as encouraging prefeasibility study results, and then announced a further mineral resource increase in February 2015. A month later the company announced an increased ore reserve for the Browns Range project and simultaneously announced the results of a definitive feasibility study. That's an unprecedented advance for the REE industry. Northern Minerals also signed a AU$49.5M partnership in February with Jien Mining, the Australian subsidiary of Jilin Jien Nickel Industry Co. Ltd. The funding will help move the project to production. Like Tasman's Norra Kärr, the Browns Range project also has an initial capital requirement under $400M, with the aim of producing over 200 tonnes of dysprosium oxide annually.

TMR: Browns Range is situated in Western Australia and a steady stream of ships containing raw materials like coal and iron ore travel from Australia to China. Does its location give it a significant advantage over others?

RC: The location helps but its richness in valuable heavy rare earths, namely dysprosium, has had the project in the sights of Chinese investors for some time now. A major shareholder in Northern Minerals is Australia Conglin Investment Group, which has deep roots in China's resource and steelmaking industries. And the partnership with Jien Mining is giving Northern Minerals the funds to bankroll the project from definitive feasibility study to bankable feasibility study and engineering and construction. Browns Range has moved at record pace compared with any other REE project in the last 20 years. Lynas took about 15 years to go from acquiring a project to developing it into production. Northern Minerals has cut that by almost 10 years.

TMR: What about Greenland Minerals and Energy?

RC: Greenland Minerals and Energy's Kvanefjeld project is on the southern tip of Greenland. The project's future was hit with uncertainty in late 2014 when the Greenland government collapsed, but the newly elected government leadership has reaffirmed its commitment to mining. In February the company announced an updated mineral resource for Kvanefjeld and in March announced the purchase of an outstanding 2% net profit royalty on the project from the previous owner. And in April it announced the signing of a second memorandum of understanding with NFC, its Chinese processing partner. The company should announce the results of a feasibility study on the Kvanefjeld project in the coming weeks. I expect the feasibility study to come with a smaller, staged-growth production plan that aligns future output volumes from Kvanefjeld with NFC's processing capacity in China. As a result, I also expect to see costs reduced from the initial Kvanefjeld development plan, which aimed to separate REE oxides in-house.

TMR: And Namibia Rare Earths?

RC: Lofdal is located in Namibia and Namibia Rare Earths announced the results of a preliminary economic assessment (PEA) on Lofdal in late 2014. It proposes an initial 7.3 year mine life producing approximately 1,500 tonnes of REE oxides per year, of which 94% will be HREE oxides—an extremely high proportion of heavy rare earth content. The PEA proposes production of a mixed REE concentrate in Namibia and further toll separation by a third party overseas, which eliminates a lot of technical risk for the project. It also has a low initial capital requirement, under $150M. Like the Tasman example cited earlier, Namibia Rare Earths also incorporated a toll-separation cost into its cash cost structure for the Lofdal PEA, which is a transparent and responsible practice.

TMR: Does the concentration of heavy rare earths at Lofdal provide Namibia with an advantage over some of its peers in attracting investment capital?

RC: It certainly helps, but having the right mix of rare earths in the project basket, whether it is HREEs or light REEs, is only important if they can be produced at the right price. Other factors in favor of HREE projects, like Lofdal and Browns Range and Norra Kärr, are the relatively low preproduction capital requirements, which in most cases can likely be funded by one or two major investors. You don't need a baker's dozen of different companies with investment capital; you can cover the bill with one or two.

TMR: Could the project be fast tracked to production given that it's in Namibia?

RC: It can likely be fast tracked given that it's located in mining-friendly Namibia and the preproduction capital requirements to develop the project are relatively low. But there are no risk-free projects in the rare earth industry. The future balance of the yttrium market, of which Lofdal is heavily endowed, hinges largely on China's continued ability to reduce illegal production in the nation's south going forward. Ongoing consolidation of China's rare earth industry will help enable that reduction but over the long term the proof will be in the pudding.

TMR: A number of companies are touting new methods for processing and separating REEs. Can you separate the pretenders from the true innovators?

RC: In my opinion there are no pretenders but a limited number of innovators. A lot of the new methods and processing innovations are coming from third-party expertise. Technical consultants who have applied innovative processing methods in other metal industries are finding that these methods may be amenable to REE extraction and separation. For example, in March Ucore Rare Metals Inc. (UCU:TSX.V; UURAF:OTCQX) announced that through the use of molecular recognition technology (MRT) the company had recovered and separated 15 REE carbonates of 99% purity or greater from feed stock from its Bokan Mountain project in Alaska. MRT technology is used in metal processing operations globally, generally for platinum group and other high-value metals. Ucore's lab-scale results suggest that it may also be amenable to commercial processing and separation of REEs.

In March, Orbite Aluminae Inc. (ORT:TSX; EORBF:OTXQX) received U.S. patents for its proprietary red mud processing. The Orbite process uses red mud waste generated from aluminum refining as a feedstock from which it extracts and separates REEs, rare metals, alumina, magnesium oxide, titanium dioxide and other economically significant metals and oxides. Orbite proposed using a very similar process in its 2012 PEA of its Grande-Vallée project in Québec. The process it proposed at that time included a bolt-on solvent extraction circuit for extracting and separating rare earths and rare metals.

Québec junior GéoMégA Resources Inc. (GMA:TSX.V), in cooperation with FFE Service of Germany, conducted lab-scale tests using free flow electrophoresis technology. The tests suggested, at least at lab-scale, that REEs can be separated simultaneously from one another—rather than sequentially—in a single step and can be done to a high-purity level without costly solvents and significant amounts of energy. The company did a lot of additional optimization work in 2014, including testing with a commercially sourced REE concentrate. In early 2015 it announced that it would begin bench-scale production of REE concentrates from its Montviel project in Québec in order to prove out the recovery rates on its own material. In March 2015 the company spun out its separation rights and lab equipment into a company called Innord Inc., which I think is a smart move as it allows strategic partners to invest in specific activities under the GéoMégA umbrella.

In late 2014, Rare Element Resources Ltd. (RES:TSX; REE:NYSE.MKT) produced a thorium-free mixed REE oxide at 99.999% purity from its Bear Lodge project in Wyoming. The company employed a patent-pending selective separation and solvent extraction process that enables full extraction of thorium and around 85% of cerium in a single step. That significantly reduces the amount of material that needs to be treated in subsequent steps, while boosting the relative value of the remaining REE oxides contained in the Bear Lodge basket.

In February, Texas Rare Earth Resources Corp. (TRER:OTCQX), owner of the Round Top REE and uranium project in Texas, signed a letter of intent with K-TECHnologies Inc. to form a joint venture that will develop and market K-TECH's Continuous Ion Exchange (CIX) and Continuous Ion Chromatography (CIC) technologies for the extraction separation of rare earth elements. CIX and CIC have been used in other metal industries for decades and appear to hold promise for the REE industry, too.

Finally, DNI Metals Inc. (DNI:TSX.V; DG7:FSE) is looking to heap leach REE oxides, as well as a suite of other metals and products, from its Buckton project in Alberta. In a 2014 PEA on Buckton, DNI proposed a large-scale bioleaching setup with subsequent separation and refinement to produce rare earth oxides, uranium oxides, zinc, copper, nickel, cobalt and 280 tonnes of scandium oxide per annum—a staggering amount. The Buckton PEA came with relatively high capital and operating costs but I think there's great potential to scale down the project and pursue a more investor-attractive staged growth plan like that proposed by Texas Rare Element Resources for its Round Top project.

TMR: You recently visited Innovation Metals Corp.'s lab-scale REE processing/separation plant near Toronto. Tell us about what is happening there.

RC: It was impressive. Innovation Metals is participating in a REE supply chain development program, which is being led by Technology Metals Research and funded by the U.S. Army Research Laboratory, a division of the U.S. Department of Defense. Technology Metals Research is operating a 120-stage, lab-scale rare earth pilot plant that's using solvent extraction to liberate and separate rare earth elements with a major focus on separation of individual heavy rare earth oxides. The 24/7 facility processes REE mineral concentrate feedstock sourced from the commercial market. The goal is to bolster North American expertise and knowledge of REE processing, specifically the separation of heavy rare earth elements of which China has a near 100% monopoly. We don't hear much about the results of the ongoing work in the press because it's not a commercial venture, but it's genuinely impressive in scale and scope. The amount of tacit knowledge the team has amassed through hands-on experimentation is amazing.

TMR: What happens next?

RC: I can't comment on behalf of those involved in the project, but I see two likely outcomes. First, the results from this initial stage will determine and inform what the next steps will be toward the project's goal of bolstering North American expertise and knowledge around REE processing and extraction. That part of the equation is funded by the U.S. Army Research Laboratory. Another outcome of this research will be the advancement of Innovation Metals' development plans for a toll-separation facility in Bécancour, Québec. This facility would serve the array of emerging producers in North America or abroad that don't want the risk and added capital expense of developing and operating their own separation facility.

TMR: Would Innovation Metals' plant be the only REE toll-separation facility in North America?

RC: It would, although some industry followers have suggested that if Molycorp doesn't opt for its phase 2 expansion to 40,000 tonnes per annum via production from its Mountain Pass ores, it could still build-out its processing capacity to toll-separate for emerging producers in North America, whether for Avalon Rare Metals Inc.'s (AVL:TSX; AVL:NYSE; AVARF:OTCQX) Nechalacho or for another company. That's a plausible scenario, but not one that will unfold immediately.

TMR: Does Molycorp have the facilities to separate HREEs?

RC: Perhaps not at Mountain Pass but through some of its subsidiaries, such as at Silmet in Estonia and Jiangyin in China, it has capacity to separate HREE oxides.

TMR: Many of these companies have seen their share prices drop to pennies. Are companies closing the doors and waiting it out? Are they selling assets? What is happening in this space behind the scenes?

RC: It's fair to say that a large number of REE juniors have placed projects on hold until conditions improve. In many cases they've turned their attention to other projects in their portfolios or are simply hiding under their desks until markets turn. About 60% of the 55 REE projects that we cover have been shelved, in some cases leaving cashless and projectless zombie owners with little left but a ticker symbol. There are also a number of REE projects that are quietly up for sale. As I mentioned, a good 15 to 20 projects continue to forge ahead.

TMR: Parting thoughts?

RC: What we've seen in late 2014 and so far in early 2015 are indications that markets for certain REEs—neodymium, praseodymium, terbium, dysprosium, the ones generally used heavily in permanent magnets—are becoming increasingly tight. The supply–demand fundamentals are falling into imbalance and are only surviving based on preexisting stockpiles. That's what has buoyed prices and that's what's sending end users into partnerships with the likes of Molycorp and others. Rare earths prices have again soured in the last month, but as soon as the uncertainty surrounding Chinese export tariffs goes away, we'll start to see more positive momentum behind REE prices and more positive market sentiment toward REE companies.

TMR: Thank you for your insights, Ryan.

Ryan Castilloux is the founder of Adamas Intelligence, an independent research and advisory firm that provides strategic advice and ongoing intelligence on critical metals and minerals sectors. He helps investors, financiers, end users and other stakeholders track emerging trends and identify new business opportunities in the critical metals and minerals sectors. Castilloux is a geologist with a background in mining and exploration and has a Master of Business Administration in finance from the Rotterdam School of Management, Erasmus University. Subscribe for free updates from Adamas Intelligence at www.adamasintel.com.

Ryan Castilloux is the founder of Adamas Intelligence, an independent research and advisory firm that provides strategic advice and ongoing intelligence on critical metals and minerals sectors. He helps investors, financiers, end users and other stakeholders track emerging trends and identify new business opportunities in the critical metals and minerals sectors. Castilloux is a geologist with a background in mining and exploration and has a Master of Business Administration in finance from the Rotterdam School of Management, Erasmus University. Subscribe for free updates from Adamas Intelligence at www.adamasintel.com.

Read what other experts are saying about:

Want to read more Mining Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit our Mining Report home page.

DISCLOSURE:

1) Brian Sylvester conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, The Life Sciences Report and The Mining Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Namibia Rare Earths Inc. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Ryan Castilloux: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.