The Gold Report: Federal Reserve of Dallas President Richard Fisher gave a speech in Australia declaring that quantitative easing (QE) must end or it would "fuel the kind of reckless market behavior that started the global financial crisis." If the Fed isn't going to end QE until employment improves, how will this end?

Eric Coffin: Fisher gets to voice his opinion at Federal Open Market Committee (FOMC) meetings, but he won't be a voting member until January. He hasn't been comfortable with QE from the start and has said so repeatedly. There isn't any news in that quote.

I don't think you'll see much change when the FOMC gets four different members next year. Janet Yellen, who will become chairman, is more dovish than Ben Bernanke. I think she was the right choice, not because she loves creating money from nothing but because she's probably been the most accurate forecaster of the bunch.

TGR: What about the bubble that Fisher fears?

EC: If you want to be cynical, you can make the argument that a bubble is exactly what the Fed has been trying to create. It wanted to get equity markets to go up because that increases wealth and raises consumer confidence. About half of the Fed's QE program is buying mortgage bonds. It is trying to keep mortgage rates down and resuscitate the housing sector.

At the end of this interview is a special offer from Eric Coffin for a free research report.

Fisher is right in a sense, but I don't think we're at the point where I'd be terribly concerned about things running out of control. I have to admit, though, that based on the growth of the economy, the U.S. equity markets are probably getting a little bit ahead of themselves. Most consumer inflation measures have been trending down, not up. Personally, I'm more worried about deflation, which is far harder for a central bank to fight than inflation.

TGR: The Q3/13 gross domestic product (GDP) report shows 2.8% growth.

EC: Right now, I'm kind of neutral on the economy. The data quality is going to be crappy for a month or two because of the government shutdown. The economy grew 2.8% because there was big growth in inventories, which is not the reason you want. Without that it came in at 2%, which was the expected number. You're probably going to see production cut a little bit this quarter because more stuff was made than could be sold.

TGR: Karl Denninger pointed out that the gross change in GDP from Q2/13 to Q3/13 was $196.6 billion ($196.6B), but the Fed's QE program injected $255B. So the economy actually shrank during Q3/13.

EC: I think he's oversimplifying a little bit. QE is really swapping paper, creating money out of thin air and using that to buy bonds that inject money into the economy. But the velocity of money has been very low since the crash. It's not as if the banks are taking that $85B/month and lending it all. That's where the real multiplier effect is. Right now a lot of the money created through QE has ended up in bank's excess reserves, not in the wider economy. Karl is a bit of a permabear, but I would agree with him that it wasn't that great a report.

TGR: Let's assume that QE continues at its present rate until June 2014. How will that affect gold and silver?

EC: When the Fed starts tapering, we have to assume gold and silver prices will get hit. Of course, if it doesn't actually start tapering until well into next year, we could see gold and silver go up for two or three months before that. That doesn't preclude later increases in the gold price based on physical demand, but the short term traders are completely fixated on QE (or lack thereof) and will be sellers once the taper starts, and the market will have to get past that before recovering.

TGR: What if it becomes clear we are going to get QE forever?

EC: Then I think gold goes to $2,000/ounce ($2,000/oz).

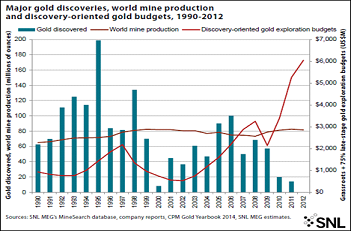

TGR: At the Subscriber Investment Summit in Vancouver last month, you compared the 10-year chart for gold to the 10-year chart for junior resources. The first chart looks good, but the second looks terrible. Why?

EC: For all the money thrown at exploration—and, of course, that number has been tumbling dramatically for the past two years—not many good discoveries resulted, especially in the last couple years. That's one reason. The chart below shows the amount of gold discovered each year since 1990, counting only new gold discoveries above 2 million ounces (2 Moz). You can see how few discoveries there have been in the past couple years. Compared to the 1990s the numbers are tiny.

The other reason is that when the gold price was rising continuously many companies were looking for what I referred to in Vancouver as "crappy ounces." Their intentions were good. They weren't trying to hoodwink anybody. They made the reasonable assumption that with gold going up and up, economic cutoff grades would keep dropping. But you can't produce gold at ever-lower grades with difficult metallurgy and infrastructure and make more money.

As it turned out, costs rose almost in lockstep with the gold price. A lot of the ounces that were marginal at $500 or $700 or $900/oz haven't been salvaged by the gold price going to $1,300/oz. Many of those resources are still uneconomic and would require more capital expenditures with longer payback periods than larger producers are willing to accept.

TGR: You said that juniors have a major credibility issue, specifically, that preliminary economic assessments (PEAs) and feasibility studies do not match production realities.

EC: There are a couple reasons for that. I've already mentioned costs. And when the sector recovered after 2000, there was a real capacity issue. There weren't enough geologists or engineers. There weren't even enough people who make truck tires.

"For all the money thrown at exploration, not many good discoveries resulted, especially in the last couple years."

Many NI 43-101s, PEAs and feasibility studies have been written by people who lacked experience. To be fair to the engineering companies, miners can have cost overruns of 20% and still be within the stated margin of error, but people never read the fine print. They just look at the production cost, so when it comes in $100–200/oz higher, everybody freaks out.

TGR: Juniors chased lousy projects because gold was soaring, and money flooded into the market. Now that gold has fallen 30%, will this engender the return of old-fashioned values?

EC: I think it already has. The large mining companies, having spent huge amounts of money on capital expenses (capexes) that didn't add to their bottom line, are now saying, "Show me margin." Large and medium companies will now pick up deposits smaller than what they would have touched 10 years ago because they have the grades, the geometry and the metallurgy to enable low-cost production.

TGR: So is margin now more important than grade?

EC: Grade is king, but margin is the key. Majors are focused on margin per ounce produced. You can get high margins with a lower-grade deposit if everything goes right but, by and large, the higher grade the better the margin should be. It comes down to net present value (NPV) and internal rate of return (IRR). Companies now want gold projects that can be built for $100–150 million ($100–150M) with NPVs of $300M or $400M and all-in cash costs of $600-800/oz—assuming they're big enough. They don't want to go too small because they can spread themselves only so thin. I don't see majors like Barrick Gold Corp. (ABX:TSX; ABX:NYSE) picking up 50,000-ounce-per-year (50 Koz/year) deposits, but we might see them picking up 100–150 Koz/year projects, when a few years ago few majors would look at a deposit unless it was capable of generating 250 Koz/year or more.

In Sonora, Mexico, half a dozen mines that began production in the last five years don't have grade. They're 0.8, 0.7 or 0.6 grams per ton (0.6 g/t), but they have fantastic combinations of logistics, costs, workforces, metallurgy and geometry, and they produce at $500–700/oz cash costs.

TGR: Why are new discoveries so important to the junior sector?

EC: That's what the juniors exist for. The market wants something new, with blue-sky potential. The companies with really big runs in the last year or two are, almost without exception, companies that made discoveries. They don't always work out, but that's the risk you take.

"Grade is king, but margin is the key."

If you go back to the pretty spectacular bull market in the mid-1990s, it was driven by companies going international for the first time in a long time, juniors going to South America and Africa and finding 3, 5 and 10 Moz deposits. Gold prices rose in the mid-1990s, but discoveries drove the bull market.

TGR: You called Reservoir Minerals Inc. (RMC:TSX.V) a "classic discovery story." Why?

EC: Most of its exciting concessions surround the Bor mine in Serbia. It's a big camp. Reservoir has a joint venture with Freeport-McMoRan Copper & Gold Inc. (FCX:NYSE), with Freeport holding 55% of the Timok project and Reservoir 45%. It's a high-sulfidation epithermal system. One of the first holes was 5.13% copper and 3.4 g/t gold over 291 meters (291m).

A real back-of-the-envelope calculation (because the holes are still pretty widely spaced) is that Timok has 30–40 million tons (30–40 Mt) of quite strong-grade gold-copper material. Freeport is a great partner. It has lots of money, and it has direct experience operating bulk tonnage and also block-cave underground mines, which Timok would probably end up being.

TGR: Reservoir's Sept. 9 Timok press release announced 260m of 3.93% copper equivalent. Is the early promise being fulfilled?

EC: It's a fantastic discovery, definitely one of the best of the last few years. Assuming Freeport goes all the way to feasibility—and I'd be pretty shocked if it didn't now—Reservoir essentially gets carried until then at 25%, which would still be significant value, considering the deposit.

TGR: What about other companies near Timok?

EC: The one that got my attention is Mundoro Capital Inc. (MUN:TSX.V). The company had originally gone into China and picked up a gold project that it expanded to 8 or 9 Moz with pretty good grades. Unfortunately, one of the state gold miners liked it even more, so Mundoro was shown the door and given $20M on the way out. It has lots of cash.

Teo Dechev is the president; her family comes from Eastern Europe and the VP of Exploration is based there. Mundoro picked up concessions there. Mundoro wasn't chasing Reservoir; it just liked the geology. The initial drill program at its Borsko Jezero property didn't come up with a Reservoir-style discovery, but its Savinac property has had some pretty interesting trench assays.

TGR: As high as 30 g/t gold and 171 g/t silver over 12m.

EC: I'm not assuming every trench is going to look like that, but it's a good start. The other two trenches were pretty decent, too. Mundoro may actually have something there, probably an epithermal system. The company has another project in Bulgaria I'm expecting to see results from it soon and a lot of other ground near Bor that has targets at earlier stages. The story is by no means over.

It's trading at only $0.24/share but has about $0.30/share in cash, enough for three years. So there's lots of leverage, if it makes a discovery.

TGR: You mentioned in Vancouver other companies with discoveries that are not as "classic" as Reservoir's but still have potential.

EC: I gave two examples. The first is GoldQuest Mining Corp. (GQC:TSX.V) in the Dominican Republic. It's trading at $0.29/share. It had a high of $2/share, and I'd be much happier if it traded closer to that, but it was $0.07/share before it discovered Romero. GoldQuest just released an initial resource estimate: 2.38 Moz gold equivalent Indicated and 790 Koz Inferred.

Keep in mind that Bill Fisher, the chairman, and Julio Espaillat, the president—Julio is Dominican—have done this before. They put Cerro de Maimón into production. This is a small but very profitable mine that was taken out for $3.20/share in 2011. Having management with direct mine building experience in country is a huge advantage.

TGR: How does GoldQuest stand for cash?

EC: About $12M right now, enough to take it most of the way to feasibility. Romero needs some infill drilling and more metallurgical testing. Most of the maiden resource is Indicated already so it shouldn't need to do a huge amount of additional drilling for the feasibility study. Metallurgical work should improve the economics. The old tests indicated 75% recovery, but those were simple bottle roll tests. Romero will be a sulfide plant and recoveries in the 90% range for both copper and gold are more common for that sort of operation.

TGR: What was the other company?

EC: Colorado Resources Ltd. (CXO:TSX.V), which has the North ROK porphyry discovery in northern British Columbia. This is one of those situations where the best hole is the first hole: 0.63% copper and 0.85 g/t gold over 242m. Colorado has since drilled decent intercepts, but none like the first, and the market has punished it.

We won't know for certain until the company puts out the remainder of its pending drill holes, but hole 9 looks as if it has hit a structure. If the zone doesn't continue SE of Hole 9 North ROK could still contain 100–300 Mt, and 300 Mt happens to be the size of Imperial Metals Corp.'s (III:TSX) Red Chris mine, which is going into production down the road. Colorado's president, Adam Travis, told me in Vancouver that the company is still figuring out the controls on the mineralization. But its logistics are really good, the best in the area, so this is a legitimate discovery, which may well be economic.

TGR: How much cash does Colorado have?

EC: It should have $5–7M after drilling. The company will probably get the rest of the holes and an initial resource estimate out before worrying about raising more money. Porphyries take a lot of drilling. If North ROK turns out to be a moderate-size, moderate-grade resource, Colorado may look for a partner.

TGR: Which discovery stories do you like in Africa?

EC: I like a couple. Actually, the first, True Gold Mining Inc. (TGM:TSX.V) in Burkina Faso, is now long past being a discovery story. It also has quite good logistics. The deposit is probably about 3 or 4 Moz, but right now the company is focusing on the oxides. The idea is to get a heap-leach operation into production, because that's a much lower capex, and leverage that to build a sulfide plant later. I expect to see a feasibility study early next year.

True Gold has very strong management. Mark O'Dea ran Fronteer Gold before it was taken out by Newmont Mining Corp. (NEM:NYSE). He's done something I hope we see more of—he brought in a completely unrelated company, an insurance company, which put a large placement into True Gold. O'Dea has done a good job of funding, admittedly with more dilution than I would have liked, but that's just the market we're in. The company certainly has enough to get through feasibility. We're probably looking at a $100–120M capex for a mine that should be able to do, say, 100+ Koz/year for 10 years. A feasibility study should be out within a couple months.

TGR: And the second African discovery?

EC: Roxgold Inc. (ROG:TSX.V), also in Burkina Faso. The 55 Zone of its Yaramoko project is a high-grade, steep-vein setting. It put out a PEA and mineral resource in September: 850 Koz gold at 13.88 g/t. This will be a small but very high-margin operation.

TGR: What other companies with new discoveries do you think have potential?

EC: Mirasol Resources Ltd. (MRZ:TSX.V) is a very successful explorer and project developer. It sold a high-grade silver discovery in Argentina to Coeur Mining Inc. (CDM:TSX; CDE:NYSE). Thanks to that, Mirasol has about $40M in cash and Coeur shares, which, coincidentally, is the same as its market cap. For political reasons, no one is a fan of Argentina these days, but the company also has large projects in northern Chile that look pretty interesting—early stage but big.

"When the Fed starts tapering, we have to assume gold and silver prices will get hit."

San Marco Resources Inc. (SMN:TSX.V) is focused on northwest Mexico, an area I've always liked and still do. The company is not cash rich but has strong joint-venture agreements with Exeter Resource Corp. (XRC:TSX; XRA:NYSE.MKT; EXB:FSE) on its Angeles and La Buena projects. Exeter has to spend $10M on Angeles and $15M on La Buena to get 60% of each. La Buena is just north of Goldcorp Inc.'s (G:TSX; GG:NYSE) Peñasquito mine and a lot of the geochemistry and geophysics are similar. San Marco has started drilling the Julia zone, and I hope we'll see drill results sometime this month. It is a riskier play but has a $3M market cap, so if it makes a discovery, there's a lot of upside.

TGR: What other companies do you want to talk about?

EC: SilverCrest Mines Inc. (SVL:TSX.V; SVLC:NYSE.MKT) announced a silver resource of 199 Moz at La Joya. It's a low-grade, polymetallic skarn: silver, copper, gold, lead and zinc. The company followed that up with a pretty good PEA: an after-tax NPV% of $93M and a 22% IRR for a "starter pit" operation that is focused on the highest grade portion of the resource.

TGR: How do you rate its management?

EC: That's the main reason I like it. Chairman Scott Drever, President Eric Fier and CFO Barney Magnusson have been a team since day one. They are all well experienced in both exploration and putting mines into production.

That experience really showed with Santa Elena, SilverCrest's Sonora mine. It has good grades and pretty much an even mix between gold and silver in value. The team has managed to get it financed at the bottom of the market in 2009, which was no easy feat, and built it for a little more than $20M, which is pretty amazing. It's producing silver equivalent at $8.50/oz. That's quite a bit better than most.

TGR: What are the prospects for Santa Elena expansion?

EC: It's most of the way through one now. Santa Elena started out as a heap leach, but SilverCrest is building a mill, which should start production early next year. That should bring the company up from, say, 2.5 Moz silver equivalent to close to 3.5 Moz next year. As the mine gets into deeper, higher grade material, it should surpass 4 Moz silver equivalent in 2015. La Joya will be more difficult, but I definitely wouldn't bet against management building it on time and on budget and making sure it makes money.

TGR: SilverCrest is in Mexico, and the new mining regime proposed by the Mexican government has been met with threats by mining companies to close operations and cease investment. Is this premature?

EC: I think some of this is politics and not just on the part of the Mexicans. If someone raises your taxes, you jump up and down. I don't want to underestimate the seriousness of this, but it gets called a royalty when it really isn't. It actually comes off the net. I think it will reduce after-tax profits by 10%, which isn't wonderful but I don't think it will suddenly make economic mining projects uneconomic. What it will do is raise the bar a bit on projects still in development. Some operations that already looked a bit marginal might not get built now.

That said, Mexico, especially the northwest where SilverCrest operates, is one of the few areas in the world where companies can put mines into production fairly painlessly, with a well-understood permitting regime and low capexes. Miners that produce gold at $500 or $600/oz cash costs are not going to become unprofitable because of a tax increase from 30% to 37%.

TGR: Eric, thank you for your time and your insights.

EC: You're welcome. I have a new report available for your readers that is free to download—it is actually an interview with one of the companies I have discussed above, which I think is a very worthwhile read. We also have a special subscription offer included in this report.

Eric Coffin is the editor of the HRA (Hard Rock Analyst) family of publications. Coffin has a degree in corporate and investment finance and has extensive experience in merger and acquisitions and small-company financing and promotion. For many years, he tracked the financial performance and funding of all exchange-listed Canadian mining companies and has helped with the formation of several successful exploration ventures. Coffin was one of the first analysts to point out the disastrous effects of gold hedging and gold loan-capital financing in 1997. He also predicted the start of the current secular bull market in commodities based on the movement of the U.S. dollar in 2001 and the acceleration of growth in Asia and India. Coffin can be reached at [email protected] or the website www.hraadvisory.com.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Kevin Michael Grace conducted this interview for The Gold Report and provides services to The Gold Report as an independent contractor. He or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Gold Report: Colorado Resources Ltd., Mundoro Capital Inc., Roxgold Inc., SilverCrest Mines Inc. and True Gold Mining Inc. Goldcorp Inc. is not affiliated with The Gold Report. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Eric Coffin: I or my family own shares of the following companies mentioned in this interview: Colorado Resources Ltd., GoldQuest Mining Corp., Mundoro Capital Inc., Reservoir Minerals Inc., Roxgold Inc., San Marco Resources Inc., SilverCrest Mines Inc. and True Gold Mining Inc. I personally am or my family is paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.