The Gold Report: You are based in Australia where iron ore and coal are the dominant mined commodities. A recent Morgans research report said, "We need to see demand-linked data improve, or at least stop getting worse, for the Chinese steel industry for us to gain any confidence" in iron ore market fundamentals. Has there been any improvement?

James Wilson: Companies with resilient supply, coupled with the remarkable cost-out performance of Vale S.A. (VALE:NYSE), BHP Billiton Ltd. (BHP:NYSE; BHPLF:OTCPK), Rio Tinto (RIO:NYSE; RIO:ASX), Fortescue Metals Group Ltd. (FMG:ASX), Roy Hill (private) and subsidized Chinese domestic iron ore production, will lower the long-term sustainable price level needed to encourage new investment in iron ore supply. We estimate this has reduced the long-term sustainable iron ore price from US$85/ton (62% Fe) to US$65/ton, capping the upside potential of any eventual recovery. As a result, we expect those miners burdened with high levels of debt like Fortescue or large leverage to iron ore like Rio Tinto will remain under pressure. Our preference remains with BHP, which maintains competitive exposure to iron ore but is significantly boosting free cash flow across its business, coupled with attractive leverage to oil and gas, one of our preferred commodity exposures.

TGR: The World Gold Council says Australia is second only to China in global gold production. How is a weak Australian dollar compared to the U.S. dollar changing the fortunes of the country's gold miners?

"A weak Australian dollar means strong leverage for domestic gold producers."

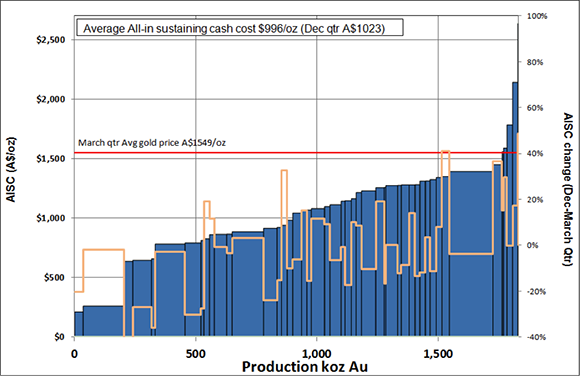

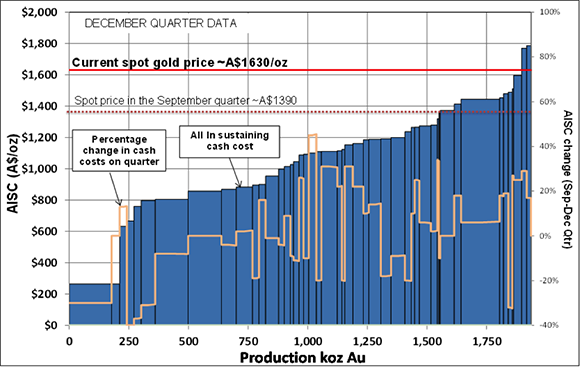

JW: A weak Australian dollar means strong leverage for domestic gold producers. At the start of the June quarter, the gold price in Australian dollars hovered around AU$1,500 an ounce ($1,500/oz), which is great considering the average "all-in sustaining cash cost" was around AU$960/oz in the March quarter compared to AU$1,023/oz in the December quarter. The bottom line is that cash margins are looking quite healthy for our Aussie miners. We are certainly seeing investment dollars directed toward predominantly Aussie domestic producers and explorers, too. One good example is Gold Road Resources Ltd. (GOR:ASX), which recently raised $39 million for its Gruyere development project in the Yamarna Belt in Western Australia.

TGR: Which metrics (i.e., cash flow per share, all-in sustaining cash costs) are the most telling as you pore over the numbers of the gold producers?

JW: All-in sustaining cash costs is our favorite metric, but it is not totally transparent, so the figures are always a bit rubbery. That being said, it has been a great way to track the sector costs on a more level playing field than previously.

Source: Morgans

Source: Morgans

Source: Morgans

Source: Morgans

TGR: What Australia-listed companies are developing gold projects with strong stories?

JW: I mentioned Gold Road earlier. It is probably the most interesting story. The company is a big takeover target thanks to its large resource base of 5.5 million ounces and growing. The company plans to use the funds it just raised to complete a prefeasibility study by March 2016 with a definitive feasibility study calendared for the end of that year.

"Cash margins are looking quite healthy for our Aussie gold miners."

Evolution Mining Ltd. (EVN:ASX) is doing great. We currently have an Add rating. The company recently made its third deal in two months by announcing that it would acquire the Cowal gold mine in New South Wales from Barrick Gold Corp. (ABX:NYSE; ABX:TSX). This is a transformational deal. Combined with the recent acquisition of the La Mancha assets in Kalgoorlie, it will make Evolution the second largest gold producer on the Australian Securities Exchange. I think the company's focus on costs will yield further upside value in the not too distant future. We are looking for future exploration upside at Cowal, La Mancha and Cracow, which along with possible increases in the gold price and further weakness in the Australian dollar could result in further upgrades to our price target of $1.40.

Crusader Resources Ltd. (CAS:ASX) is also doing well. We recently visited the Juruena site in Brazil and believe it has significant potential for a near-term, small-scale operation. Drilling has continued to intercept high-grade zones at Querosene and an initial resource estimate is in the works. We are looking forward to Crusader connecting with a bigger funding partner to capitalize on the opportunity in the historic mining area. The company continues to operate a cash flow positive iron ore operation where operating costs have continued to fall due to cost improvements. A new deal with Vale could expand the operating footprint at Posse. The company is also moving forward with development at the Borborema project where plans for a more affordable 1.5–2 million tons per annum operation could be released by the end of the year.

"We are seeing investment dollars directed toward predominantly Aussie domestic producers and explorers."

TGR: What are some Australian graphite companies you have been following?

JW: There are not many to choose from on the Australian Securities Exchange, but we have been following Metals of Africa Ltd. (MTA:ASX) thanks to its location along strike from the Montepuez Central project in the massive Balama deposit of Syrah Resources Ltd. (SYR:ASX) in Mozambique. Metals of Africa recently announced a high-grade, near-surface assay with large average flake size.

We have also been taking a look at Magnis Resources Ltd. (MNS:ASX) recently. This is a near-term graphite producer working in southeast Tanzania.

TGR: Please complete this sentence: In the mining sector, 2015 will be remembered as the year of the. . .

JW: . . .patient investor!!!

TGR: Thank you for your insights.

James Wilson is a senior analyst at Morgans. He is a qualified geologist who spent his early career in regional exploration in Western Australia with CRA & Great Central Mines before moving on to exploration and mining feasibility roles in West Africa, North Africa and China. He has since specialized as a mining analyst, joining Morgans in 2010.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) The following companies mentioned in the interview are sponsors of Streetwise Reports: Syrah Resources Ltd. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

2) Morgans may from time to time hold an interest in any security referred to in this interview and may, as principal or agent, sell such interests. Morgans may previously have acted as manager or co-manager of a public offering of any such securities. Morgans' affiliates may provide or have provided banking services or corporate finance to the companies referred to in the report. The knowledge of affiliates concerning such services may not be reflected in this interview. Morgans advises that it may earn brokerage, commissions, fees or other benefits and advantages, direct or indirect, in connection with the making of a recommendation or a dealing by a client in these securities. Some or all of Morgans' Authorised Representatives may be remunerated wholly or partly by way of commission.

3) James Wilson: Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.