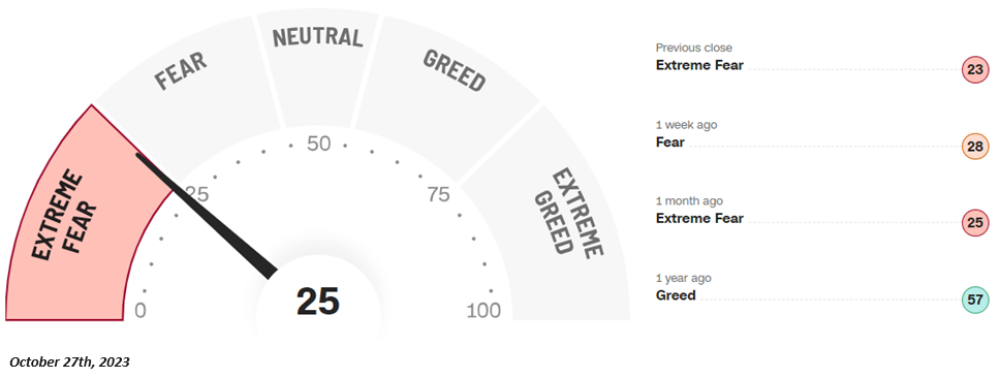

Last October, I began posting a number of charts that would suggest that the average investor was rapidly approaching that point in the cycle where they usually throw in the towel and jettison that last remaining remnant of a hemorrhaging portfolio in what the behavioral psychologists have referred to as a "capitulation bottom."

While anything that comes from the CNBC "research department" cannot usually be trusted, their "Greed-Fear Indicator" is usually a halfway decent

tool for discerning investor sentiment. I first found it in the Market Laboratory section of Barron's magazine and was granted the right to display it by the late Citigroup Strategist and founder Tobias Levkovitch. I have been using the indicator since the turn of the 1990s, and up until the Great Financial Bailout in 2008, it was a fairly useful market timing and risk management tool.

After working quite well at the late-October lows, it was sitting at <Extreme Greed> for most of the latter part of February and most of March as the AI-driven tech stocks finally flattened out and gravity took hold. Here is a repeat of a rare Sunday email alert sent to subscribers on April 7:

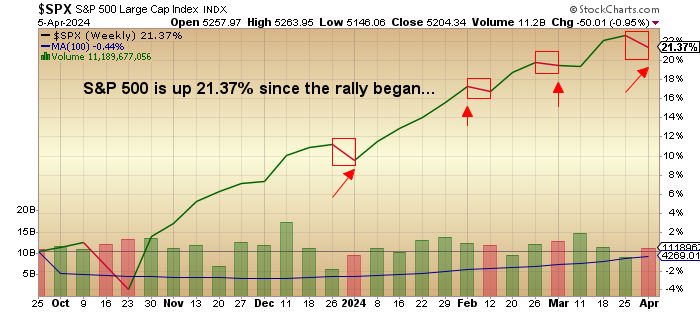

"Last week was one of the few down weeks since the rally in stocks began in late October of last year. It marked the fourth week of the past twenty-four that was down in a period that has been one of the strongest performances for stocks in history."

The S&P 500 is up 21.37% for the period October 27, 2023 until April 5, 2024 while the NASDAQ is ahead by 22.91% for the same period.

Advances in these amplitudes are not only rare; they reek of extreme intervention and manipulation.

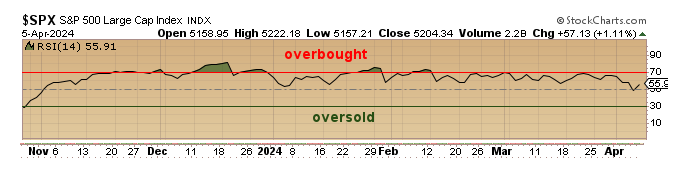

The Relative Strength Index sitting at 55 is no longer overbought bought looking back to December, one can see that it is now in full decline which indicates a serious loss of momentum.

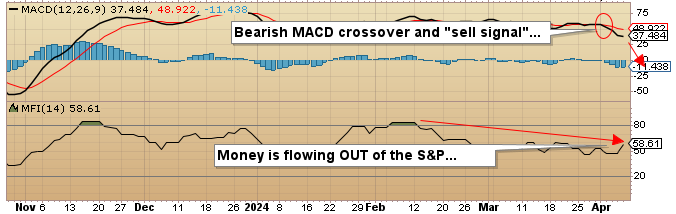

Just before the March month-end, there was a bearish MACD crossover that constitutes a "sell signal," and while this has been unreliable unto itself since the rally began when coupled with declining RSI and the declining Money Flow Indicator ("MFI"), you get the sense that some serious erosion has suddenly taken place in the rally's resilience.

Note the above chart that has the S&P500 essentially "hugging" the 20-dma all the way up from the October 27th lows, with the only break being the fake-out during the first week of the year when tax-related issues triggered larger-than-normal outflows. Since then, only very brief skirmishes have occurred, with last week being the most serious.

Nvidia

Lastly, the market leader, Nvidia (NVDA:NASDAQ) — the company that launched artificial intelligence into the limelight for the new meme in technology stocks — has rolled over with a trendline break, a 20-dma failure, a bearish MACD crossover, and an MFI reversal. There might be rotation into other sectors but when the leaders begin to roll over, there is usually a sharp correction before new leadership leads stocks higher.

Hence, I see a correction on the near-term horizon.

Now, that said, despite all of these indicators that have worked admirably in prior times, they have not been working since October, with what appears to be an "invisible hand" rescuing stocks every time they look ready to cave in. I have a small put option position in the DIA June $375 puts at $3.50 in an attempt to recapture the drawdowns from January and April, where my attempts to top-pick the Dow were soundly thrashed. I do not trust any of the data being spewed out by any of the government departments in either the U.S. or Canada, but what I do trust is the bond market.

Note how the 10-year yield has not only reversed the downdraft that triggered the stock market advance last October but has also taken out the February and March highs around 4.30%. In fact, the 10-year yield penetrated the 4.40% level Friday before backing away, which tells me that while the stock junkies are convinced that Jerome Powell is going to launch a series of rate cuts before the November elections, the bond market is believing none of it.

In fact, bonds are looking for a rate increase in response to economic data that continues to reveal stronger than expected growth, stronger than expected employment gains, and hotter than expected prices, three conditions that do not lead to Fed easing.

So, take away the arrival of easier credit conditions and hotter CPI numbers, and you will have the perfect recipe for a serious Wile E. Coyote moment where the over-leveraged traders suddenly find themselves without a net.

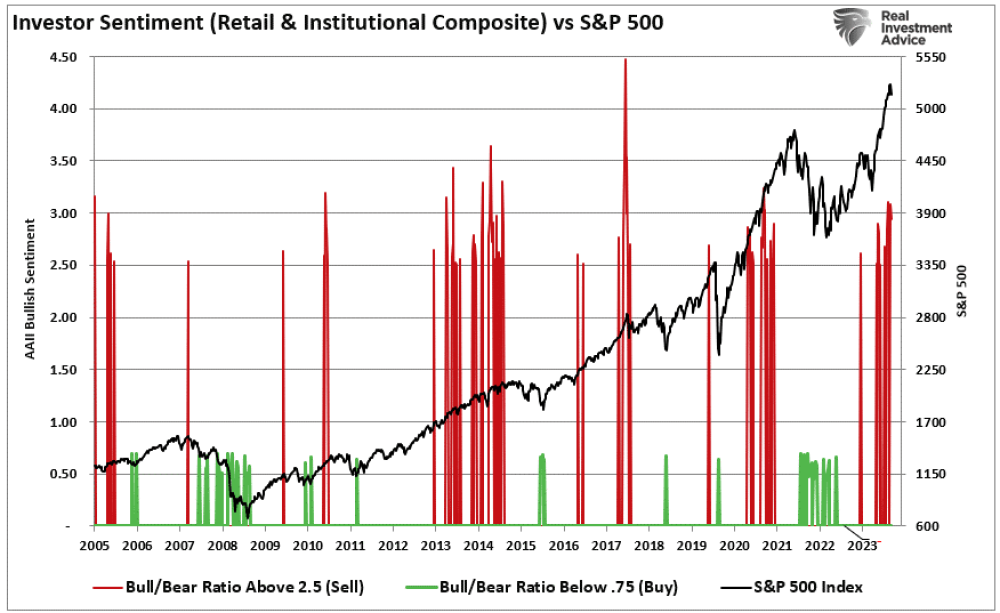

Sentiment is also uber-bullish (which is actually uber-bearish), as you can see from institutional positioning. The American Association of Individual Investors (known as the "AAII") shows the bull-bear ratio approaching historic highs, which is in itself an indication that investors and traders are now "all-in."

Margin debt is also now higher than it was prior to the 2008 Great Financial Bailout Crisis, which only means that the more leverage out there underpinning stocks, the greater the volatility once that leverage is forced to be unwound, as we saw in 2008 and 2020 as well as 2022.

Needless to say, that was a timely email alert because if one fast-forwards to today (Friday), note the weekly S&P 500 chart that has clearly broken down.

Now take a quick look at the chart of market darling and narrative provider NVidia Corp., whose price fell a full 10% today in what has to be the curtain call for the tech stocks, punctuating one of the most obscenely politicized ramp-jobs in market history, all designed to lure the American electorate into thinking that all is well with their debt-engorged economy and deeply split social fabric.

When the market leader and general-in-charge of "all-things-equity" — NVidia — literally crashes down through 20-dma and 50-dma inside of nineteen days and is now heading into month-end reeling from multiple body blows and about to get downgraded by the legions of portfolio managers that have made billions off its epic run, you just know markets are in trouble.

This is not going to be a pretty month-end, especially when everyone wakes up and realizes that they are going into that oh-so-famous "Worst Six Months" period that forces these portfolio managers to "Sell in May or go directly to jail" lest they miss their critical monthly bonus figures out of loyalty to the mighty NVDA beast?

Not bloody likely.

Copper

In contrast to the moribund bearishness expounded in the first section of this week's missive, I must rejoice in the recognition that the "beast-of-all-things-metal" — the mighty copper — closed at a two-year high today and is taking aim at the all-time high just over $5.00/lb. last seen in March 2022. My colleagues are taking ample potshots at me because I am constantly retweeting bullish copper commentary by the legendary Robert Friedland.

Now, be it known that I have known Bob since the 1990s, and while I cannot boast that he is on my Christmas Card list, nor do I expect a call on my birthday, I have immense admiration for him for none other than his olfactory sensibility to money and lots and lots of it.

When the jabs come rolling in reminding me of what can only be described as "the obvious", I ask that they acknowledge that I am fully aware that Bob Friedland rarely, if ever, parts his lips to promote anything unless Bob Friedland has a large position in it. I have followed the Friedland mystique for years and years and have been watching the progress of his family company, Ivanhoe Mines Ltd. (IVN:TSX; IVPAF:OTCQX), as they partnered up with the government of the DNC and the Chinese and created an absolute monolith of a copper company in the Kamoa-Kakula Copper mine. It is one of the only new sources of copper available on the planet as supplies dwindle and resources deplete.

When the bashers were all going through breathless conniptions over the "biased view" brought by Friedland to the copper discussion and attempted to counter with the "China slowdown" angle, Friedland responded with more knowledge about the demand for copper in China than any Wall Street analyst could ever have offered, let alone deduce.

All I have ever known about Friedland is that he is a brilliant thinker and an even better communicator. I simply followed his line of thinking and drew my own conclusions that copper was then and now is a beast that will not be tamed. With that as ammunition, I offered subscribers Freeport-McMoRan Inc. (FCX:NYSE) as my top pick in the blue-chip space for 2024, and as well as it has performed, I might have had "a taste of my own cookin'" and decided to use IVN:TSX as my alternative proxy for copper trade as it has doubled the return of the mighty FCX.

The junior copper explorers I own are all doing better but nowhere near as well as they might have if there had been basic knowledge of the investment space that retail investors have for technology and crypto present in the junior resource issues. I try to tell investors that when the Fed decided to bail out the banks and got full Congressional and Senatorial support for that horrific move, it shifted the landscape for anything resembling either "free markets" or "sound money" as priorities that should be guarded like first-born children.

It forced the impatient youngsters to ignore the wisdom of their aging mentors who tried to steer them to gold and silver, but after getting rebuked soundly by forces both foreign and foul in their attempts to profit from the precious metals arena, they bolted like cattle in a lightning storm. Hopefully, as the benefaction of the metals — all metals — continues to bestow monetary benefit to more and more of our investing brethren, it will filter down to a broader acceptance by the kiddies of the junior metals developers and explorers.

Last point on this: in 1978, very few investors knew a great deal about gold or gold stocks, but a number of the older veterans knew a thing or two and they loaded portfolios up to the absolute MAX with every imaginable penny miner that had land within thirty farmhouses of a gold occurrence and while gold at $125 per ounce in 1975 jiggled very little in the way of "animal spirits," by 1979, even the mention of staking a claim in gold country sent the shares rocketing to unimaginable heights.

The harvesting of profits in 1979-1980 by the old brokers and their much younger clientele was legendary, and that, my friends, is exactly what we can expect.

| Want to be the first to know about interesting Technology and Base Metals investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- Michael Ballanger: I, or members of my immediate household or family, own securities of: All. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

- This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.