I used the phrase "Shades of '99" as the title for this, the May 8 weekly edition of the GGM Advisory newsletter, because, although it was 25 years ago, the famous phrase about history never repeating but often rhyming holds fast and true.

Back in the day, long before computerized trading or the current version of high-frequency trading, I used to be what the old-timers called a "tape reader".

Back in the day, long before computerized trading or the current version of high-frequency trading, I used to be what the old-timers called a "tape reader".

At the front of the bullpen, just above the equity trading desk, was an old-style ticker tape, but in its time, this electronic ticker was like looking at the Business News Network (BNN) television screen, where stock symbols rolled across the screen from right to left, creating a kaleidoscope of colors and letters that only a trained eye could successfully decipher.

My mentor at the time was a former floor trader on the old Toronto Stock Exchange, and he taught me how to spot idiosyncrasies in the flow of symbols.

For example, if Sundance Oil & Gas (Symbol SDN) started to dominate the screen, it meant volume was picking up, which usually was a precursor to drill results. As the years rolled by, I rarely paid less attention to the ticker, but as they say, "old habits die hard," and when

I did find the occasion to watch the tape, and some of those 50-year-old triggers would spring back to life.

That was the story of the past week as I found myself bedazzled by the tape action, where eight out of every ten symbols rolling across the tape were semiconductor stocks.

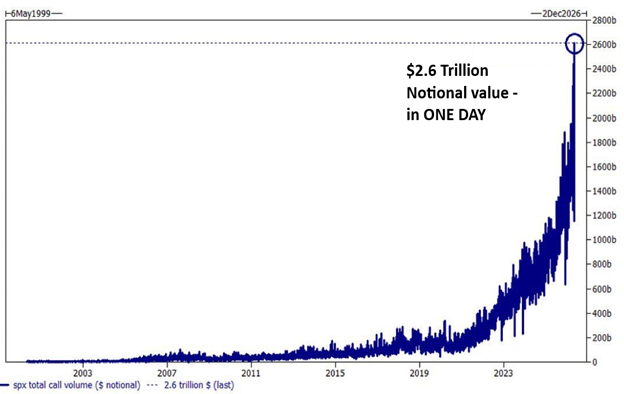

You see, the Philadelphia Semiconductor Index has been on fire — and I mean a serious "el fuego". Despite a war in the Middle East, $100 oil, and a long bond yielding over 5%, investors are partying like it's 1999 with record call option buying, mostly in the semiconductors.

The cheerleaders over at the Bubble Network (CNBC) are giddy with "irrational exuberance" (a term made famous in the months leading up to the 2007-2008 Great Financial Crisis) as the terror they felt back in March and one year ago during the Tariff Tantrums has been totally extinguished.

The tape action I was watching all week long reminded me of the period of the late 1990's when anything vaguely associated with the "Internet Revolution" sent anyone with a pulse and a few dollars in the bank to their nearest broker with clear instructions to "Buy me ANYTHING that ends in .com" . The "dotcom bubble", also known as the "internet bubble", epitomized a period of speculative mania that drove U.S. technology stock valuations sky-high during the late 1990s. Fueled by a fervor for internet-based companies, equity markets experienced exponential growth, highlighted by the Nasdaq index skyrocketing from under 1,000 in 1995 to more than 5,000 by 2000. This speculation relied heavily on the promise of profitability rather than actual earnings, leading to a frenzy where investors overlooked traditional financial fundamentals.

However, as 2000 ushered in a sobering reality of widespread overvaluation, the market suffered a dramatic correction. The Nasdaq plummeted dramatically from a peak of 5,048 on March 10, 2000, to 1,139.90 by Oct. 4, 2002 — a staggering decline of 76.81%. Many dotcom stocks went bankrupt, and even established companies like Cisco Systems Inc. (CSCO:NASDAQ), Intel Corp. (INTC:NASDAQ), and Oracle Corp. (ORCL:NYSE) saw their stock prices erode by over 80%. This crash culminated in a prolonged financial recovery, with the Nasdaq taking 15 years to reclaim its previous high on April 24, 2015.

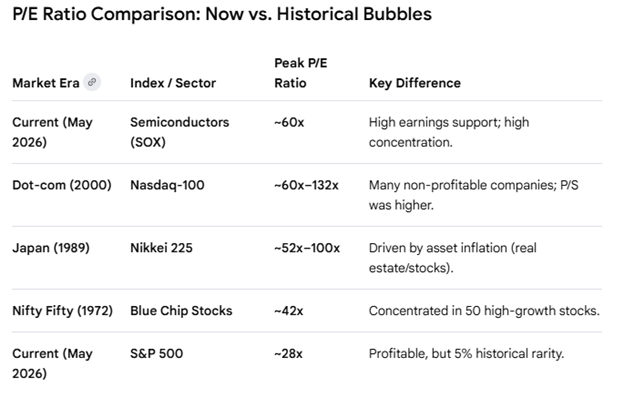

The "Cartoon Network" (CNBC) must have trotted out over two dozen "guest commentators" in the past two days to explain to the viewing audience why exactly "this time is different" with everyone 100% unanimous in their convictions that capital expenditures related to the buildout of the artificial intelligence infrastructure are the mother's milk of this bull market. There is some validity to the notion of potential future for companies like Microsoft Corp. (MSFT:NASDAQ), but much of it is generating nothing in the shape of current or even near-term profits. The question must therefore be raised as to the timeline of profitability for these huge megacap technology companies that are making gargantuan "wagers" on the future profitability of "generative AI".

Subscribers know all too well the phrase that I have used since the GGMA's inception: "any market trend that moves from "gradual" to "vertical" (as in incline or decline) is a trend that entered its terminus". The semis had a nice advance off the lows of October 2023, which then got fairly serious after the April 2025 "Liberation Day" as it graduated from "gradual" to "near-vertical" into early-2026. However, after a minor correction in February-March, it has, in the past 37 days, moved to a "vertical" ascent, not sometimes but always symptomatic of the terminus of the move. The problem remains not whether the trend is about to change but when, as the shape of the X-axis (time) is screaming "soon," but the Y-axis (price) is indeterminable.

The tape action in the late-'90's was eerily similar to the tape action I witnessed this week; not only are retail investors "piling on", but professional investors are also in the hunt for performance-altering names, resulting in the inevitable "chase" that always marks the top. Much of this mania gas arrived in the form of a "gamma squeeze," which is a self-reinforcing feedback loop where massive buying of call options forces market makers to buy the underlying stock, which in turn drives the stock price higher. This phenomenon is driven by the mechanics of the options market rather than company fundamentals. The degree to which this type of squeeze has been affecting the semiconductor stocks cannot be underestimated, but what is critical to understand is that this action inevitably gets unwound, and when it does, the downside velocity will be nasty.

Could it really be "different" this time? Could the "AI build-out" result in mindboggling profits that will ultimately justify these nosebleed valuation levels for the semiconductor stocks? The answer is, as always, "Of course." However, a similar question was asked in 1999, whether the internet was going to change the information landscape over the next decade, and while it most certainly did, many of the early entrants to the internet space disappeared long before the event occurred.

As I witnessed in 2000-2002, yesterday's darlings of the "internet bubble" are no different than today's darlings of the "AI bubble". Some will flourish while many will cease to exist. As in all market cycles, the "pretenders to the throne" will be vanquished while the "true heirs" will succeed. What is a veritable certainty in my mind is that no matter what the outcome, all members of the space, whether they be "pretenders" or "heirs," are super-prone to a bloodcurdling correction that will take the $SOX:US down to the 100-dma at best, which resides approximately 30% beneath where it closed on Friday.

On the discussion of gold, let me first post this chart:

Now, I again ask the question: "Is there ANYTHING wrong with this chart?"

The answer, in addition to being totally self-evident, is a categoric "NO!" followed by not one but 50 exclamation marks. So I turned to the other metals in which I am "fully-invested" (meaning "I own WAY TOO MUCH") and up popped the "Good Doctor" as in "Dr. Copper".

Followers of this publication know all too well my affection and affinity for the one metal with a PHD in Economics — copper — and one glance at the chart dating back to the COVID lows, and I walk away with one simple, two-word definitive: bull market. The copper market is the deepest, most liquid metal market in the entire world. Until two decades ago, it always reflected marginal increases or decreases in global economic activity because it could never be fooled. Supply was more or less constant, so that was a variable upon which analysts could rely, such that price swings to the downside became leading indicators of industrial demand. Fast forward to the decade of the tree-hugging ecological protestors and politicians, determining that the kiddies that control social media "know better" and have a Divine Right of Permitting, this has put a severe stunt into the construction of new mines and the discovery of new ore bodies destined to replace the aging and depleting reserves of the "Old Guard" like Antofagasta Plc (ANTO:LSE; ANFGF:OTCMKTS) and BHP Billiton Ltd. (BHP:NYSE; BHPLF:OTCPK).

For any of the doubters out there that are swallowing the current Wall Street narrative that the negative action since the outbreak of hostilities in the Middle East on February 27 is the start of a major bear trend in the metals, have a glance at the three-year chart of the Bloomberg Commodity Index. If one ever wanted to question the government-generated Consumer Price Index over the past three years, which is on the record as being approximately 3.2% per annum, how on earth can an index of all commodities (including food and energy) be up 73.4%?

I stopped listening to the pundits over two and a half decades ago concerning inflation because it became apparent that the only way the U.S. could fund its military expenditures which have

averaged $663 billion per year, with the 2026 estimate being in excess of $1 trillion. If buyers of U.S. treasuries were given an actual rate of inflation in the U.S. closer to what the Bloomberg Commodity Index implies, there would be a buyer's strike of epic proportions.

With commodity prices trending bullishly, why pray tell, are my list of junior resource developers and explorers acting so poorly? The chart posted on the next page reveals a junior resource sector that is struggling to find its footing after the late-January blow-off in metal prices. Using the S&P/TSX Venture Composite Index as a proxy for the junior resource stocks as a group, you can see how easily it doubled off the April 2025 lows of last year, but running face-first into a wall of profit-taking coinciding perfectly with the end-of-month peak in January. It tried to recover in the weeks leading up to the Prospectors and Developers Association Convention ("PDAC") in early March, but seasonal forces put an end to that literally the week of the conference. Since then, it has experienced a series of lower highs and lower lows and sits 15.28% off recent highs. I use the term "recent highs" because that index reached its all-time high of 3,371.63 points on May 2, 2007, which was nineteen years and seven days ago, for those who care about such trivial facts.

It was during the global financial crisis of 2007-2008 that the index plummeted to roughly 670 points by December 2008, a drop of approximately 80% from its peak. This index continued to struggle over the following decade, such that by late 2014, it was cited as being down roughly 80% from the 2007 record. It hit further multi-decade lows during the March 2020 /COVID Crash, briefly dipping below 400 points. As of May 8, 2026, the index closed at 997.29. Compared to its 2007 peak, the exchange is still down about 70.4% in total value.

So, owning the junior resource sector in no way vaguely resembles the mania of the past three years in technology issues. The junior resource sector has a great deal of recovery embedded in its future, especially when one considers the paucity of capital expenditures on mining projects during the last two-and-a-half decades.

I have, since the 1990's, used the month of February as a time for raising cash as I am superstitious enough to follow the "PDAC curse" that seems to usher in a near-term top in the TSXV every year. I also learned a long time ago that the month of August is usually a good time to accumulate the juniors and that old horse chestnut goes way back to the 1960's when speculators were forced to sell their penny stocks in order to pay for back-to-school expenses such as tuitions, room-and-board, and books. The sector would remain weak until after Labor Day, and all the bills were paid, at which point the selling was over, and the juniors would be allowed to levitate. It may sound nonsensical, but it has worked pretty much along that framework for more than a few decades. I see no reason why it will change in 2026.

Of course, there will be event-driven moves in the junior space related to corporate developments or drill results that tend to arrive in the mid-late summer. Most of the names in my portfolio are active explorers as well as developers, so stay tuned for news releases and/or volume spikes that are precursors to critical events. This should be a very active summer for more than a few of the juniors.

| Want to be the first to know about interesting Copper, Gold, Artificial Intelligence and Technology investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers, contractors, shareholders, and/or employees of Streetwise Reports LLC (including members of their household) own securities of Intel Corp.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: None. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.