Undoubtedly, every newsletter writer, podcaster, blogger, and armchair stock wizard is now bent over his/her keyboard trying desperately to find the words to adequately describe the most bizarre case in stock market history, marking the confluence of literally forty-four years of stock market evolution. I was a rookie stock salesman back when this bull market started, and I remember it like it was yesterday. No, wait. I remember it like it was August 12, 1982, and August 1982 was nothing even vaguely similar to June of 2026.

Today, the public has been trained to worship stocks and idolize stock market trillionaires like Elon Musk. Back in the summer of '82, people hated stocks, refusing to answer telephone calls (from rotary phones) from stock salesmen, even if they were a blood relative. In fact, it was so bad that on the rare occasion that somebody with enough money (and intestinal fortitude) to invest actually answered your call, you had to spend at least twenty minutes listening to what that person thought of "you people" as if stockbrokers were from a different planet.

On one occasion, I was going through my daily list of prospects, painfully engaged in the art of "cold calling" where I would call someone I had never met before who had no idea who I was, with the expressed intent of selling them the "Stock of the Day" that came to our branch office via teletype every morning. I dialed a number in Sarnia, Ontario, and was unlucky enough to have the owner of this construction business actually answer his own company telephone.

Shocked that I could even get an answer, I quickly introduced myself, stated the name of my firm, and explained the reason for my call. The man on the end of the phone paused and then said. "Let me get this straight. You are calling to pitch me on a "hot stock" that your "firm" says will make me a lot of money, right?"

I confirmed it to him, after which he said, "The last time I took the advice of a lying, thieving stock salesman was last year, and it cost me $10,000, and you actually expect me to listen to your pitch?" Well, for the next ten minutes it went downhill from there as I was called every name in the book that included sexual preferences, psychological trauma, integrity, honesty, and whether or not I was still wetting the bed.

Now, I had arrived at work that day in ill humor as I had not had much sleep the night before due to a howling alley cat that was just below the second-floor apartment window, which had to remain open due to a distinct lack of a functioning air conditioner. So, I listened carefully and begrudgingly to the insults of this venomous human being for the full ten minutes, and then, for some ungodly reason, I snapped. As he was finishing off one particularly nasty piece of instruction as to where I should insert the research report I had offered to send him "Free of charge!", I interrupted him and said, "Mr. Curran, it would seem that I may have chosen a poor day to have a conversation with you. Tell me, sir, do you remember the name of my firm?" He grunted back, "No, and I don't particularly care either." I then asked, "And do you happen to remember my name?" Again, he snarled and said no. I then said, "OK, let me summarize. You are not able to remember either my name or the name of my firm. Is that correct?" He then said in the most condescending tone of voice imaginable, "That would be correct, Einstein."

Then, in what could have only been an out-of-body experience, I shouted an <expletive deleted> into the mouthpiece and slammed the phone down.

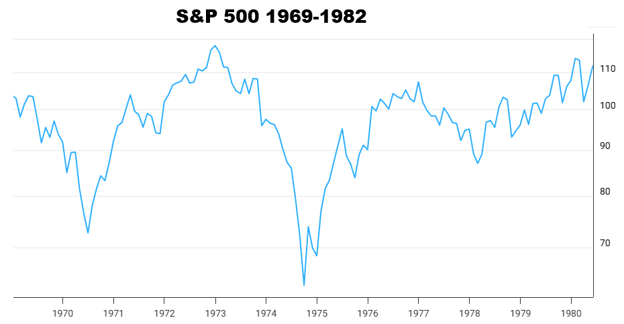

Investors in 1982 had just gone through one of the most exasperating decades in stock market history as the S&P 500 peaked in 1973 above 120 and then spent nine years trading below it, reaching a bottom at around 62 in 1974. In fact, it was inflation and Watergate that crippled stock prices brought on by the "Great Society" spending blitz under LBJ in the mid-Sixties and the cost of the war in Vietnam that caused the U.S. national debt to explode higher. In fact, many of the ill-fated programs of the 1960's and 1970s are rhyming with this current decade, which is the Millennial version of the "Roaring Twenties", that period of economic boom times that preceded the Crash of '29 and The Great Depression.

It might be said that the "AI bubble" of 2026 is a mirror image of the "British Railroad bubble" of 1847-1850, where miles upon miles of track were laid only to lie fallow for years until demand caught up with supply many years later. Analogies to the dotcom craze of 1997-2001 are everywhere, but as far as extremes go, the current mania surpasses any prior boom period by a substantial margin in terms of market cap to gross domestic product, margin debt, and price-to-sales ratios.

Many of the old-timers would suggest that the 1973-1974 bear market was the worst in recent memory with its 48.2% drop from peak-to-trough but statistically, it was the "Great Financial Crisis" (which I love to call the "Great Financial Bailout") of 2007-2009 where the S&P 500 crashed 56.78% from a peak in 2007 at 1,565 to its March 2009 low at 676 that was the Papa Bear Market of the past fifty years. Because it was over and done in a relatively short period of time thanks to the government bailouts and rescue packages, investors were not forced to face the music on their own and were in fact given a playbook in 2009 that encouraged them to take inordinate risks with their retirement accounts and college funds and rainy day nest eggs because as we have witnessed since 2009, no decline in stocks is ever allowed to last more than a few single-digit percentage points before the stimulus cavalry rides in to the rescue.

There will be hundreds of commentaries by the end of next week both praising and condemning the Spacex IPO as it is entered into the hallowed Wall Street Hall of Fame as the richest IPO in history but at the same time embodying the "Future of America" with artificial intelligence marrying up with outer space exploration which certainly justifies a company that had a net "burn" of nearly $5 billion in 2025. While Starlink is highly profitable as a satellite internet provider, the space exploration and AI divisions are "cash incinerators" of the highest order. The IPO was successfully completed on Friday at $135 per share with its opening trade at $150 and high print at $175. The market value at the high of the day exceeded $2 trillion (with a "T"), and if CNBC were to show Elon Musk's smiling face one more time by the closing bell, I was going to launch my five-pound paperweight through the TV screen.

2026 is definitely not like August '82.

Precious Metals

The precious metals have been in a dour funk since last January 29, when gold scaled the $5,626 level, and silver crashed through $123 with calls for "$500 silver by summer!" and "silver shortages everywhere!" ringing throughout the blogosphere and reverberating around the Twitterverse with astounding certainty and remarkable hubris. Up until earlier this week, the gold and silver gurus of 2025 had been trying in earnest to find a way to make amends for all the money they had been losing their subscribers by preaching the "ten rules of dollar debasement" to their unsuspecting followers.

Notwithstanding the fact that I have been hearing, reading, and watching the hard money gang preach from the same prayer book since 1980, what the newcomers to the "Dying Dollar" narrative forgot to tell their flock of eager Kool-Aid drinkers was that gold and silver are not "deities" to be honored by the offering of sacrificial lambs otherwise known as "subscribers". Gold and silver have a "bid" and an "offer" and are influenced by the same rules of demand and supply as any other stock, commodity, or fixed income vehicle.

As I pointed out in January, three times to be accurate, with small losses taken twice, the precious metals markets had been rising in an orderly "gradual" manner from late-August 2023 after Fed Chairman Jerome Powell shifted from "hawkish" to "neutral" during his Jackson Hole speech. It was late last year, beginning in August, two full years after that "Powell pivot", that the PMs decided to depart from the "gradual" ascent and embark upon a steepening of the ascent, moving from a comfortable 45° incline to 75° in December and then the final 90° "vertical" incline in January.

The top came like a thief in the night; it arrived without fanfare and with no advanced warning (except from party-poopers like yours truly), but when the events of January 29 were in the history books, they marked one of the truly classic textbook reversals in market history. Silver went from $123 to $64 in five sessions before bottoming on March 23 at $60.94.

Each rally saw lower highs, and each decline saw lower lows, making the last four months vintage bear market behavior. This past week, I was forced to put away my bearish inclinations toward the PM's because the relative strength index for gold touched levels last seen in the summer of 2023 at the tail end of the Fed-tightening cycle, when it plunged to the mid-20 level.

While the Hamas attacks on Israeli citizens on October 7of that year undoubtedly caused a watershed shift in sentiment, I think that the market this week finally decided to ignore the posts on Truth Social and, in fact, see the Middle East conflict for what it truly is: a mess. It now appears as though there is not going to be an easy way for Trump to back down after suffering not only heavy losses in the campaign to remove the Iranian hardliners but also the embarrassment of failing to secure the Strait of Hormuz or the enriched uranium.

For the very first time in 2026, I told subscribers that I was making the move to "bullish" for both gold and silver, and I put my money where my mouth was on Wednesday with the purchase of the GLD:US as well as some at-the-money call options on it and the SLV:US for August expiries. I also cautioned that these purchases are "trades" and not long-term investments to be kept in a hallowed room in the basement along with lit candles and burning incense. The downtrend line drawn of tops in January and May comes in around $4,425 for spot gold or around $410 for the GLD:US, so I will be on high alert if and when I see those levels being tested and will have zero remorse about flinging all positions summarily overboard in order to lock in profits.

As for silver, it is a somewhat dissimilar beast than gold in that it can gain trajectory and momentum in the blink of an eye, largely because it is persistently in the crosshairs of the legions of podcasters and bloggers that love to pride themselves as "silver specialists". For me and for these trades I put on last Wednesday, I am watching the downtrend line, which coincides perfectly with the 100-dma at around $79.50 as my near-term target. I will not be donning my "Silver Squeeze Hoodie" anytime soon, and I will refrain from saying any silver-oriented prayers in order to augment my chances for success. When silver approaches that downtrend line, I will be offering my leveraged positions happily and with nary a shred of remorse. After all is said and done, it is merely a "trade".

I am adamant on treating these new positions as trades because the events of January 29 were too similar to September 2011 and August 2020 to allow me to remain complacent. It may well be that I am trading on the long side of a bear market rally, and based on the blow-off tops in January, that is still an odds-on favorite as a call. However, markets were egregiously oversold this week, so I took the plunge. If it turns out to be "THE" bottom, I will be more than happy, as will my junior gold positions that still inhabit my portfolio on the whim and prayer that the final speculative blow-off in the junior miners lies ahead of and not behind us.

S&P/TSX Venture

The S&P/TSX Venture Composite has been behaving poorly since the January 29 blow-off top in the precious metals, but that is no surprise to followers of this service. I have been droning on and on for years about the correlation between the gold price and the TSX Venture Exchange, and no better illustration than the chart shown below.

A series of lower lows and lower highs since January has the TSXV on its heels, and in all likelihood, this malaise will last until after Labor Day, into the middle of September, after the kiddies are all back in school, tuitions paid, and room-and-board money all accounted for. It doesn't mean that prices will continue to drop right through to September, but what it does suggest is that upside momentum will be subdued until the majority of speculators return to the junior mining arena.

What will coerce the typical junior resource noodler into writing cheques again will be either a) an across-the-board upturn in metal prices or b) a major discovery. A third possible catalyst could be corporate activity in the form of an investment by a major miner into a junior explorer or developer, but absent any of those three triggers, the juniors stay fairly quiet right through to mid-September.

The companies I am buying are ones I already own; I rarely add new names to my list of holdings during the summer months because the ones I hold are ones that I trimmed in the pre-PDAC period (January-February). In my case, all of the companies I own are deeply-rooted explorers that are active in the field as this is being written, so with the possibility of a game-changing discovery present for most of my junior holdings, I stick to my knitting, as they say.

One company that I particularly like, given my newfound fondness for "all that glitters," is little Grafton Resources Inc. (GFT:CSE; PMSXF:OTC), whose management group is the same group that runs my top-ranked Fitzroy Minerals Inc. (FTZ:TSX.V; FTZFF:OTCQB) and who continue to be active in Chile, one of the best places in the world to be involved in the mining and/or exploration business.

While FTZ/FTZFF is a copper-centric explorer-developer, GFT/GFTFF is a designated precious metals explorer-developer with projects in both gold and silver located in enviable jurisdictions in Chile.

From what I have been able to glean, they are currently in the "accumulation phase", as in the hunt for projects and properties in Chile. Director and Technical Advisor Gilberto Schubert has been toiling in this region for over thirty years, and as the former country manager for Vale, he knows the Chilean landscape better than most.

From what I have been able to glean, they are currently in the "accumulation phase", as in the hunt for projects and properties in Chile. Director and Technical Advisor Gilberto Schubert has been toiling in this region for over thirty years, and as the former country manager for Vale, he knows the Chilean landscape better than most.

While management has a solid track record in all the right spaces, it is the capital structure that caught my attention.

Most junior miners involved in exploration and/or development for the past number of years tend to have bloated share structures largely because from August 2020 until October 2023, the metals were caught in a moribund malaise of disinterest that meant "Keep the Lights On" financings were necessary at depressed prices for the better part of three years resulting in a great many shares being issued just to keep active and by "active", I mean "still listed", as opposed to drilling their properties.

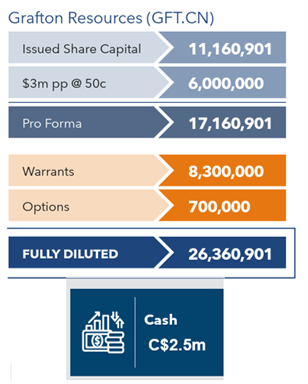

GFT/GFTFF was put together late last year as a new shell company with an extremely tight float, such that the company has working capital exceeding CAD $3 million with only 26.3 million shares issued (fully-diluted).

They avoided the "dilution trap" because they took advantage of the hot markets in late 2025 to complete two small raises at $.30 and $.50 and are now fully-funded.

One of their properties, called Alicahue, is in the same vicinity as Fitzroy's Caballos project, with a piece of ground held by a major mining company sandwiched between the two.

The company announced on May 20 a "Letter of Intent" with Denver-based Newmont Corp. (NEM:NYSE; NGT:TSX; NEM:ASX), but the details were omitted in advance of a "Definitive Agreement" which will sort out what properties and terms have been agreed upon. I eagerly await the revelation of the details of this transaction and firmly believe that this is the kind of corporate development that will act as a positive catalyst for the stock.

Just the proximity to Caballos could be reason enough for GFT/GFTFF to support a market cap double or triple the current level in the event that Caballos turns out to be another Los Bronces or Las Pelambres, two of the more noteworthy copper-molybdenum mines in that part of Chile.

In the interim, these lazy summer markets may allow some stock to shake free, which is why I was bidding literally all week long with little result.

Grafton is a "strong buy" for a big move into year-end.

| Want to be the first to know about interesting Special Situations, Silver, Copper, Gold and Technology investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers, contractors, shareholders, and/or employees of Streetwise Reports LLC (including members of their household) own securities of Grafton Resources and Fitzroy.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: Fitzroy Minerals and Grafton Resources. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.