Back in December of 1996, I was enjoying the greatest nine-year stretch I had yet experienced as a member of the Canadian Securities Industry. Starting with the post-'87-Crash discovery of gold and silver in B.C.'s "Golden Triangle", the Eskay Creek discovery was the first of a number of market-rattling resource discoveries made in the Americas that propelled the junior resource sector to dizzying heights through most of the next decade. In 1991, the discovery of diamond-bearing kimberlites in Canada's Northwest Territories triggered the largest staking rush in history as over $200 million was spent acquiring land positions.

After early sampling in September 1993 confirmed a drillable target, the Voisey's Bay (Labrador) nickel-copper-cobalt discovery became one of the most significant mineral finds of the late 20th century because the ore was both incredibly high-grade and located close to the surface, making it remarkably easy to extract. The discovery triggered a fierce multi-billion-dollar corporate bidding war. In 1996, Canadian mining giant Inco successfully purchased the site for a staggering CA$4.3 billion.

Right after that came the Pierina gold-silver discovery in northern Peru by Canadian explorer Arequipa Resources Ltd., whose share price skyrocketed from roughly $2 per share to a buyout price of $30 per share (by Barrick Mining Corp. (ABX:TSX; B:NYSE)) in under a year. Those four discoveries were followed by the third major diamond discovery in Canada's NWT by Mountain Province Mining Inc. (today called Mountain Province Diamonds Inc. (MPVD:TSX)), whose early funding requirements were handled to no small degree by yours truly. Its move from the pennies to nearly $10 in 1996 will remain forever etched in my septuagenarian memory banks.

The wealth created by these five major discoveries was truly mindboggling for the resource investor community that resided primarily in Canada, but with a major component being the U.S. investor class. Everything was humming along swimmingly until U.S. Federal Reserve Chairman Alan Greenspan threw the first chink into the armor-plated shield of the Canadian resource sector when he made those fateful remarks about "irrational exuberance" representing a "clear and present danger" to the health of the mainstream American (and global) economy.

However, the major crippling blow came in April of 1997 after Strathcona Inc. reported the results of a forensic audit of assay results from the multi-billion dollar Bre-X gold debacle. I was presenting Mountain Province to a group of Fidelity fund managers the morning of the announcement when, after arriving in the reception room, I saw the morning section of the Globe & Mail's Report on Business with the headline "Strathcona confirms Bre-X Gold Discovery a Fraud".

The meetings were originally planned in the largest of the Fidelity meeting rooms, but by the time 9:00 am arrived, the number of managers attending had dwindled from fifty to around ten. The body language of the attendees as I stepped up to the podium to introduce our corporate client was unmistakable — folded arms, eyes diverted, staring at watches, and more than the occasional yawn — all confirmed that these gentlemen did not want to be there.

I decided that the only way to diffuse the tension was with humor, so with a large disingenuous smile on my face, I said boldly: "Good morning, everyone, and thank you for attending. I am here today representing a junior Canadian exploration company — HOW DO YOU LIKE ME SO FAR???"

After the nervous laughter subsided and the presentation ended, the senior Fidelity boss came over and said, "Great presentation under difficult conditions." After which he shook my hand and said, "Have a good flight back. See you again in ten years."

Well, it wasn't ten years but a little under five years that the junior exploration sector went completely dormant, with only the gold breakout in 2001 resurrecting the buyers. What had been a nine-year run of "irrational exuberance" in the junior mining space had turned into a four-and-a-half-year period of corporate finance agony. It was in late 2001 that the phone rang, and my Fidelity contact started our conversation as if it were only yesterday. "I told you ten years, and here it is almost five. Send me your list of junior gold miners, and maybe we can do some business again."

I should add that between the horrific revelation of the Bre-X fraud and that phone call, the world had to deal with the Asian debt crisis of 1997, the Russian debt default of 1998, and the popping of the dotcom bubble in 2001, all of which threw bucket after bucket of cold water on the Canadian junior miners.

Here in 2026, the markets are still absorbing the impact of government response to the COVID-19 pandemic of 2020, where total global economic stimulus deployed to fight the COVID-19 pandemic shutdown reached approximately $17.2 trillion in direct government fiscal spending, with some banking and monetary estimates placing the broader combined global injection closer to $32 trillion. That liquidity continues to slosh around the financial system, finding a home for the most part in common stocks, as the S&P 500 has moved from a low of 2,191.86 on March 23, 2020.

With the S&P 500 at 7,580, it has increased 3.46 times the lows of 2020, while U.S. gross domestic product has grown from $21.54 trillion to $32.38 for a gain of 1.5 times. The S&P 500 has increased 2.31 times the rate of growth for the U.S. economy, which tells me that the culprit can only be one thing — the liquidity created during the pandemic.

The new poster child for this love affair with stocks is the rise of "artificial intelligence" deals led by the number one chipmaker, Nvidia Corp. (NVDA:NASDAQ), whose share price is up 4,085% since the pandemic lows. By comparison, Costco Wholesale Corporation (COST:NASDAQ) is ahead only 250.1% in the same period. Even computer maker IBM:US is only up 220.2% in that time span, which tells me that the majority of the liquidity created by the global governments has been channeled into "AI," which has, in fold created not one shred of profit (yet), but where most of the revenue growth has come from bonds issued to fund the build-out.

Therefore, since there is no real evidence of an increase in productivity or earnings, this advance in the valuations for all companies directly or indirectly linked to the "AI build-out" represents a hybrid of the Greenspan euphemism "irrational exuberance," only this time, analysts should insert the term "artificial exuberance" to qualify this quantum leap in overvaluation.

And anyone buying into a market driven purely by (unbridled) greed and fear (of missing out) is bending down in front of a steamroller to ensnare the quarter lodged in the cement. The risk surely outweighs the potential reward.

More importantly, what bearing does this have on the Great Commodities Supercycle being lauded and applauded by everyone with a blog or podcast that has swallowed the "AI build-out" story hook, line, and sinking microchip? More importantly, what are the ramifications for the S&P/TSX Venture Composite, now showing a year-to-date gain of only 1.41% despite gold up 4.47%, silver up 6.73%, and copper up 10.46%, all on a year-to-date basis?

The answer lies in the current obsession amongst the younger generation of retail traders — and they are retail, short-term traders whose definition of a long-term trade is where the ink is barely dry on the confirmation slip. Mind you, everything is electronic these days, so maybe the 2026 version of a short-term trade is where they set the sell price before they receive a fill on the buy side.

Whatever the case may be, this generation of traders that has been trained — brainwashed — into believing that no matter what price they pay for anything, if it starts to leak oil, the Fed or the Treasury will send in a bugle-bearing cavalry of "dead presidents" to flood the market with sufficient liquidity such that nobody loses money. It is just like when they give out the end-of-year report cards to the kiddies these days, and everyone has a "cum laude" on their card with nary a one failing.

When I was in school, the cards were given out to the average students first, with the "cum laude" eggheads next in line and the "summa cum laude" nerds at the tail end. In fact, the kid with the highest mark in the class got a special nod from the home room teacher. The poor numbskulls that failed were not even given "summer school" as a penance until years later, after I became a parent, because the educators in the 1950s believed (and rightly so) that the floaters that resembled Cro-Magnon man failing to do their "lessons" deserved the embarrassment of starting the next year with kids a year younger than them.

I grew up in a working-class aircraft manufacturing town in northwest Toronto, and to walk into a grade eight class and see your older brother's pal with the finest pork chop sideburns in the entire school, seated in the front row, was quite a shock when every other boy in class was still two years away from puberty. It was always the kid with the sideburns who stayed after class to get extra help, and that was the whole purpose of holding him back a grade. Kids always strove to avoid embarrassment through achievement rather than entitlement, which is most certainly a departure from today's classrooms.

I wonder what happens if and when the current fiscal debt bomb with the lit fuse forces the Fed and the Treasury to refrain from rescuing the capital markets in order to avoid defaults. The Fed was able to rescue the banks back in 2008, but who, pray tell, will be rescuing the Fed when the monetary chickens come home to roost?

Total securities (purchased by the Fed) at their amortized cost are estimated to be $6.47 trillion ($4.39 trillion in U.S. Treasuries and $2.08 trillion in Mortgage-Backed Securities), with the market value of said securities at $5.63 trillion, leaving a net paper deficit of $844 billion at year-end, which has recently hovered around $857 billion. The Fed is an "independent federal agency and not a GSE ("government sponsored entity"), but the role of the Fed, it has been said, is to "manage U.S. monetary policy and financial system stability" as opposed to a GSE whose role is to "expand credit and liquidity in targeted sectors like real estate".

You cannot tell me that the Fed was not doing exactly that for the banks during either the 2008 GFC or the 2020 Covid pandemic. The Fed is the sole possession of its member banks, and as such, there will never be an occasion when there is a "cash call" as in the great film "Trading Places" where the Chairman of the commodity exchange says to Mortimer Duke, "You know the rules of the Exchange, Mr. Duke! All accounts are to be settled at the end of the day's trading, without exceptions." (at which point Randolph Duke collapses).

Whereas poor Randolph came to a sudden realization that no one was going to rescue either him or his brother, there is going to be an occasion where officials at the U.S. Fed and Treasury have a "Randolph Duke moment" with the sudden realization that there is no recourse other than default, which sends the USD into a death spiral. With that, commodities will explode to higher ground, but what will the "AI" hyperscalers do with all that new debt? The major tech hyperscalers —Amazon.com Inc. (AMZN:NASDAQ), Alphabet Inc. Class A (GOOGL:NASDAQ), Meta Platforms Inc. (META:NASDAQ), Microsoft Corp. (MSFT:NASDAQ), and Oracle Corp. (ORCL:NYSE) — have taken on approximately $230 billion to $260 billion in cumulative new balance-sheet debt over the last five years.

It is still a drop in the proverbial bucket as compared to the debt being held by the Fed at $6.47 trillion. Add them all together, and you have all the right ingredients for an epic drop in the purchasing power of the U.S. currency, the inverse of which is an epic surge in the dollar-denominated price of commodities, which, I should add, includes all of those critical minerals required for the "AI build-out".

So, when subscribers are emailing me with questions about the companies I own, I try to take a philosophical approach. The juniors are, unfortunately, doomed to a life of elevated volatility because they are largely illiquid and fraught with executional risk. However, the ones I own have management teams that have put together well-defined resources, such as gold, copper, or silver. There is always execution risk, but I gravitate to companies that see themselves purely as developers with no intention of taking on the risk of either mine construction or production.

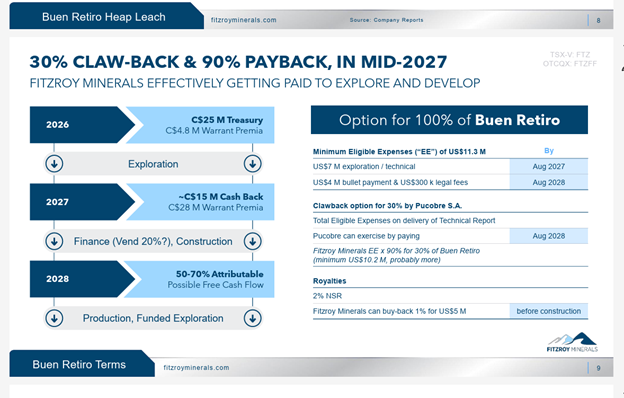

A great example is Fitzroy Minerals Inc. (FTZ:TSX.V; FTZFF:OTCQB), whose management has an economically viable oxide copper resource in Chile.

They announced on April 23 that they had signed a "Letter of Intent" with Chilean miner Pucobre S.A., whereby the latter intends to exercise their 30% "clawback provision".

CEO Merlin Marr-Johnson sums it up beautifully: "The joint Letter of Intent is a major validation of the Buen Retiro Heap Leach project and is a win for both parties. Pucobre benefits by potentially securing production from the Buen Retiro Heap Leach to fill spare capacity at Planta Biocobre for many years, and thereby significantly improve operational economics by spreading fixed costs across more production units."

The Fitzroy CEO makes no bones about the company having no delusions about managing a producing mining operation. They know that Pucobre S.A. is the expert at heap-leaching oxide copper deposits in the Chilean jurisdiction, so they welcome the LOI with open arms. For me as a shareholder, it is important that I see a clear path to an exit strategy.

Otherwise, many of these junior miners just languish in mediocrity. The company emphasizes in all of their presentations that they are "explorers first and foremost," and the establishment of a large copper-bearing sulphide deposit at either Buen Retiro or Caballos is in addition to the oxides at BR.

Therein lies my exit strategy because the free cash flow off the oxides makes any purchase of FTZ/FTZFF immediately accretive as of 2028. CEO's at the major mining companies will look at the accretive nature of the acquisition very fondly because the markets will not penalize their shareholders, which is critical.

We are going to go through the normal summer doldrums that the bulls refute every single year since the 1980's, whether we like it or not. Every year, some junior mining executive gives me five bullet points on why his company's share price will advance over the summer months, and every year it fails to happen. I have told subscribers numerous times that the TSXV will present an opportunity around the middle of August, with possible exceptions being any junior that delivers an unexpected world-class drill intercept, which is possible with every single company I hold. I urge you all to keep an eye on the drilling progress and avoid getting frustrated with the lack of movement.

Enjoy the summer and get ready for an exciting second half of 2026 just like the second half was in 2025.

| Want to be the first to know about interesting Copper, Artificial Intelligence and Technology investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers, contractors, shareholders, and/or employees of Streetwise Reports LLC (including members of their household) own securities of Fitzroy Minerals Inc. and Amazon.com Inc.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: Fitzroy Minerals Inc. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.