There is a type of securities fraud that falls under the banner of "manipulation," known as "wash trading". Wash trading is a form of market manipulation where an investor simultaneously buys and sells the same financial asset to create artificial market activity. It works in a number of ways, either where one trader buys and sells from themselves using different accounts, or two cooperating parties buy and sell from each other back and forth.

The goal is to have the asset change hands, but where the actual owner remains the same, while the transaction costs are the only real money lost by the manipulator. Why the perpetrators get involved in "wash trading" is to create the illusion of high liquidity and market interest, artificially driving an asset's price up or down, where such high activity tricks real investors into buying into a dead asset. In crypto, it is often used to farm "platform transaction rewards" (whatever that is). The markets most affected by it are the unregulated exchanges, which frequently suffer from automated wash trading bots and NFT's where the creators buy their own digital art to make it look highly valuable. It was outlawed as "strictly illegal" under regular stock exchanges, but still attempted historically.

The Securities Exchange Act of 1934 established the SEC and created Section 9(a) to outlaw the creation of a "false or misleading appearance of active trading" via wash sales, which is legally classified as "fraud" because it was misleading the public market.

This past week, the new Chairman of the Federal Reserve Board, Kevin Warsh, was sworn in during a White House ceremony that included Fed-basher President Donald Trump. The new Chairman is considered to be a monetary policy "hawk" who has repeatedly pledged to act independently, even as he criticized the central bank for what he called "mission creep" and its response to the pandemic inflation surge. However, commentaries throughout the twitterverse and all over the blogosphere would have us believe that somehow this new Chairman of the American central bank is going to usher in a new regime that is more clearly committed to Main Street, otherwise known to mean "Joe Sixpack", a somewhat derogatory descriptive of the "average American voter" often referred to by Hilary Clinton all-inclusively as "the deplorables". Mr. Warsh has already confessed to a desire for some changes at the Fed, including a focus on reshaping inflation metrics, streamlining communication, and shrinking the Fed's footprint in financial markets.

The list of specific items includes:

- Reducing the Fed Balance Sheet: Warsh has expressed a desire to aggressively reduce the Fed's massive balance sheet, aiming to shrink it down from over $6.7 trillion toward a baseline closer to $3 trillion.

- Limiting interventions: He believes the balance sheet should only be used during periods of severe economic crisis or market dysfunction, rather than as a routine tool to manipulate general financial conditions. He prefers to rely almost exclusively on the federal funds rate as the primary economic lever

- Using "AI" as a deflationary "supply-side" force: To balance President Trump's demands for rate cuts with the reality of stubborn inflation, Warsh has introduced a supply-side economic theory centered on technology. He views artificial intelligence as a massive, structural disinflationary force that will rapidly expand productivity and economic output. Under this view, he believes the Fed may eventually have room to cut interest rates aggressively because AI-driven efficiency gains will keep inflation naturally contained.

- Fed Culture: Warsh plans to narrow the central bank's focus back to its core dual mandate: "price stability" and "maximum full employment". He has publicly criticized the Fed's previous drift into social and political issues, asserting that the institution should not be involved in climate change initiatives or diversity, equity, and inclusion (DEI) policy tracking. Furthermore, he has firmly ruled out the creation or pursuit of a central bank digital currency (CBDC) as he most certainly should.

When I ran through the checklist of Warsh's new policy initiatives, it became obvious that there is actually nothing new to anything he has proposed. You see, to really understand the Federal Reserve, you have to go way back and understand how and why it was created.

The whole concept of a "national bank" was fiercely opposed by the Founding Fathers of the United States, who considered banks "more dangerous than standing armies," as was written by Thomas Jefferson in his memoirs. Only the Panic of 1907 could finally persuade the lawmakers to spit in the eyes of the Founding Fathers. In mid-October 1907, speculators F. Augustus Heinze and Charles W. Morse attempted to corner the stock of the United Copper Company. ("Cornering" a stock means buying up enough shares of a company to gain control of its available supply, allowing the buyer to artificially dictate the market price.)

The plan failed spectacularly, causing the stock to collapse and bankrupting the brokerage firms involved. Because Heinze and Morse held prominent positions at several New York banks, panicking depositors rushed to withdraw their money, fearing those banks were now insolvent. The panic quickly spread from traditional commercial banks to trust companies, which were highly vulnerable financial intermediaries that competed with banks but were less regulated, keeping cash reserves of only about 5% compared to the 25% required for national banks. When the Knickerbocker Trust Company—New York's third-largest trust—collapsed and closed its doors on October 22, it triggered a massive, systemic crisis of faith across the entire U.S. banking sector.

Enter the venerable and legendary financier, J. Pierpont Morgan. With no central bank to step in, the powerful J. P. Morgan locked New York's top bankers in his private library, where he forced them to pool their money to bail out failing institutions and keep the New York Stock Exchange open. Only the brazen actions of Morgan and friends prevented a complete breakdown of the financial system, but the memories of the event were not lost upon either the bankers or the lawmakers because the specter of private citizens being forced to bail out the banking system was an admission of vulnerability of capitalism and the American Way.

It was in 1910 that a group of bankers and lawmakers met at the Jekyll Island Club on Jekyll Island, Georgia, under the guise of a "duck hunting trip" that the structural framework for the Federal Reserve Bank was established. Directly triggered by the Panic of 1907, the group met to draft a comprehensive overhaul of the chaotic American banking framework. Over those ten days, they formulated the "Aldrich Plan." (Henry Aldrich was a U.S. Senator.) While Congress initially rejected the plan because it gave too much power to private banks, its core structural features served as the direct blueprint for the Federal Reserve Act of 1913, which created the modern U.S. central bank (the "Fed"). So, it was a panic orchestrated by financiers trying to corner a stock that led to the creation of what is today the Federal Reserve Board. The decision to meet on Jekyll Island had nothing to do with "the average American voter" ever. It was deemed necessary for the guaranteed survival of the U.S. banking system.

Kevin Warsh is the new Chairman of an institution created for the expressed purpose of protecting the banks. It was not until the Federal Reserve Reform Act of 1977 did the Congress add the triple mandate" of "maximum full employment", "price stability", and "moderate long-term interest rates", with the latter two lumped together leaving only "price stability" and "maximum full employment" as the dual mandate. The notion of his appointment being anything vaguely resembling "regime change" verges on the absurd because history would prove that with a balance sheet at over US$6 trillion, up from US$800 billion in 2005, the outrageous money creation in reaction to the 2007-2008 GFC and the 2020 Covid pandemic is proof-positive that "price stability" was and is not a concern of the Fed. Ensuring that the bankers still received their bonuses in 2008 and 2021 were two occasions where the Fed looked after the banks well in advance of looking after Joe Sixpack.

I will be on the lookout for anything that resembles the 2026 version of "Warsh Trading", where the Chairman of the Federal Reserve Board manipulates the minds of investors by creating the illusion of Fed activity in the areas of "price stability" and "maximum full employment" under the guise of looking after the "average American voter" when in fact the only concern being raised is for the continued profitability of the member banks, you know, the registered owners of the Federal Reserve.

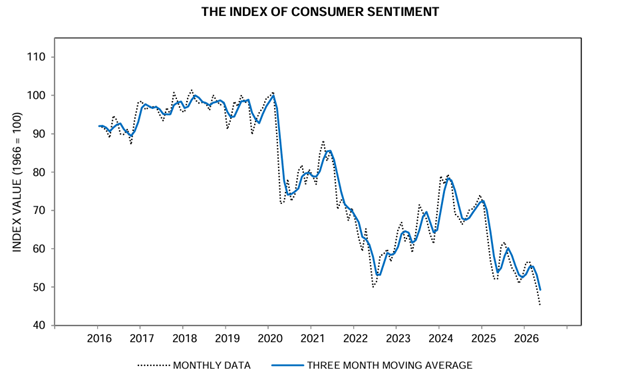

That Mr. Warch entered his new position the very day that the University of Michigan Index of Consumer Sentiment was released, showing a record drop in all categories, is ironic. Here is poor Mr. Walsh trying to get the Fed to tone down "interventions" and reduce the size of its balance sheet, as many of the member banks he has sworn to protect that are actually choking on debt created by the Fed itself. When the Fed funds rate hit zero six years ago, a large number of financial institutions backed up the truck and loaded up on debt, selling carloads of bonds with artificially depressed coupons thanks largely to the Fed.

Six years later, and that mountain–continent of debt has to be rolled over with the coupon now four full percentage points higher. I will be curious to see what happens when all those wonky commercial real estate loans start going south. Will Mr. Warsh be the champion of Joe Sixpack and start dumping the $1.98 trillion of mortgage-backed securities that they have been taking off the member banks since 2008? Will he let the big banks like JP Morgan and Goldman Sachs flounder under the weight of margin calls from their hedge fund clients? You all know where I stand on that.

Kevin Warsh is "the new boss," and yes, he is exactly like "the old boss," and to coin a very misused and abused phrase, the more things change, the more they remain the same.

Gold

In a BBC broadcast in 1939, the great British stateman, Sir Winston Churchill, was asked if he could make a forecast concerning Russia, and his reply was:

"I cannot forecast to you the action of Russia. It is a riddle, wrapped in a mystery, inside an enigma."

In 2026, a subscriber asked me to give her my best forecast for gold, and my only reply was, "I cannot forecast to you the action in gold. It is a riddle, wrapped in a mystery, inside an enigma."

Truly, the gold market has me befuddled. One look at the longer-term chart of gold and you breathe a long and satisfied sigh of relief. The five-year chart for gold looks absolutely superb. It is undergoing a "healthy correction" (term used by bulls when they wish thy had sold at or near prior peak) with the trend line drawn of the October 2023 low still very much intact.

However, as much as we all stand up and pound our fists on the table avowing ‘til the death that "we all invest for the long-term", we all secretly dread corrections because they are stressful, irritating, and no fun.

Along that line of reasoning, long-term investments are short-term investments made at the wrong price and at the wrong time. They metamorphose into long-term investments because we hate taking losses on deals that should be going up and refuse to listen to our screams in the bathroom at four in the morning. It is not the long-term chart that gives me grief; it is the short-term chart.

They say that technical analysis is "reactive" rather than "predictive," and I find that criticism only partially correct because if I had a dollar for every "technical breakout" that proved to be a false signal, I would not be forced to write newsletters at my advancing stage of life. The chart shown on the next page is the six-month chart, and it is, to say the least, troublesome.

You will note on the chart posted above the red ellipse that marks the crossing of the 50-dma under the 100-dma, which is not considered a major technical event, but it does carry implications.

When a 50-day moving average (50-DMA) crosses below the 100-day moving average (100-DMA), it signals a major shift toward an intermediate-to-long-term "bearish trend reversal".

In technical analysis, moving averages track momentum over specific windows. When a shorter-term average falls below a longer-term one, it proves that recent downward price momentum is accelerating faster than the historical baseline.

While there are certainly no guarantees of anything in the capital markets these days, the implications of this cross are as follows:

- Loss of Intermediate Momentum: It confirms that the short-term buying pressure has officially exhausted, shifting control from the bulls to the bears.

- Resistance Level Flips: The price points where these averages intersect often transform from former psychological support floors into heavy overhead resistance.

- Precursor to a Death Cross: While not as severe as the classic Death Cross (50-DMA crossing below the 200-DMA), this event acts as an early warning system that a deeper, structural bear market may be forming.

In that last bullet point, the operative word is "may".

Want to be the first to know about interesting Gold investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter.

Subscribe

Important Disclosures:

-

Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.