The typical investor right now has no clue just how perilous the investment landscape has gotten. What's transpired over the last eleven weeks in the Middle East puts our entire future at risk. With each passing day that the Strait of Hormuz stays shut, the predicament grows more menacing.

As I'm putting this together, President Trump is over in China. What comes out of that brief visit, along with the calls he makes in the coming week, will decide whether we even have a future at all. (He's back stateside now. The China trip amounted to absolutely nothing.)

For four decades Israel has peddled the fiction of an Iranian nuclear weapons program. There isn't one. Our pricey eighteen intelligence agencies are all on the same page about this for an obvious reason that even Secretary of State Rubio and Robert Kagan grasp. Iran doesn't require nuclear weapons because controlling the Strait accomplishes more.

That said, Israel has been scheming about the Greater Israel project for ages. The blueprint demands wiping out Iran, just like what was done to Libya, Somalia, Sudan, Lebanon, Iraq, Gaza, Syria and the West Bank. Israel was never the wronged party. They have always been a criminal regime carrying out genocide all over the Middle East. Israel has lost this war] but won't own up to it or let DJT walk away.

Trump's sit-down with China is a pivotal moment. As I write this, the outcome is anyone's guess. My hunch is Trump gets sent packing with his tail tucked. Washington has no leverage. Beijing is holding every card in this hand. Iran controls a Strait. Trump has dismantled the American empire by waging an unnecessary war on Israel's behalf.

Epstein worked for Mossad. Two separate sources inside Mossad have verified this. Bibi is sitting on the Epstein files with over 10,000 hours of recordings tucked away in his office. DJT shows up roughly 38,000 times in those files. Naturally, since DJT and Epstein were thick as thieves and shared everything. Including, in all likelihood, underage girls.

Nowhere in recorded history can you find an instance of some inconsequential little brain-dead nation like Israel ordering the world's most powerful country to bankroll and prosecute a war on its behalf. Not until today.

My view, and I think the historical record will bear this out, is that on February 11, 2026, Bibi showed up at the White House and put the squeeze on DJT by threatening to release certain Epstein tapes. Bibi insisted the United States join a war of aggression on Israel's behalf against Iran. This isn't America's fight. It's Israel's, plotted out long ago.

If China declines to provide any real help to Washington in the Iran war, and they have no reason to, both China and Russia come out ahead simply by letting the United States flail in the swamp it dug for itself. If China sits on its hands and DJT alongside Israel goes after Iranian infrastructure, Iran has vowed to hit the rest of the GCC states backing the US the same way. Should that play out, we won't be staring at a 20% energy shortfall, we'll be looking at 50% and a billion lives lost.

This war on Iran has shown the Middle Eastern states that the United States is a paper tiger. The defense umbrella they were promised turned out to be a mirage. Honestly, the overpriced gear cranked out by the MIC is junk. Why would the GCC keep shelling out for pricey defense kit that doesn't deliver? The US has lost dozens of planes, exhausted our whole inventory of useless surface-to-air missiles, and hundreds of young Americans have died waging a war for Israel against a country that isn't even our adversary. Incidentally, the US still claims only thirteen American servicemembers have been killed in this conflict. That's a flat-out lie. The actual count runs into the hundreds. Those coffins are stacked up in Germany because DJT doesn't want the relatives or the taxpayers footing the bill for his deranged war to discover the genuine price tag.

The Petrodollar has expired. The GCC won't be parking surplus cash in Treasuries or insisting on USD-denominated payments any longer. Consequently, the bedrock of the American economy aside from paper shuffling, namely the MIC, is headed for extinction. Why purchase gear you already know doesn't perform as billed? Both Saudi Arabia and Qatar have started hinting that abandoning the US and partnering with Iran might be the smarter play. The six GCC countries house substantial Shia Muslim populations that side with Iran in this war.

The recent jump in gold, silver, platinum and copper prices points to hyperinflation right around the bend. The USD will linger on much the way the British Pound still turns up in some transactions, but its worth will plummet. President Trump's pointless war on Iran has wrecked his administration.

Even though the broader stock market remains riding a massive sugar rush fueled by the AI mania, it's hunting for a pin to puncture the bubble. The bond market, America's lunatic debt pile, the metals, are all flashing warnings that ugly times lie ahead. My personal conviction is that the minuscule 1% slice of total investment dollars allocated to resources is the only refuge. Our financial system has reached a major tipping point. A massive shift is coming.

Porter Stansberry just released an important video every investor should see. My suspicion is the peak hits this week with the Philly Semiconductor Index notching a fresh high for eighteen sessions running. The Nasdaq racked up nineteen consecutive up days back in March 2000 and that was the exact top.

Two longtime acquaintances of mine in the resource sector recently teamed up to build what I think will be the destination investment for American and Canadian resource investors. One huge blunder that 99% of management teams at resource companies commit is repeatedly diluting their share price and float through round after round of private placements.

The biggest retail market on the planet is funded by American investors. Resource firms covet and require access to that pool of capital but overlook the fact that brokers can't pitch shares priced beneath US$5. So brokers simply never bring up the penny juniors. The people at the helm of junior resource outfits have effectively shut themselves out of the U.S. investment market by keeping their share price under US$5.

Two serious Canadian juniors saw the problem and turned it to their advantage by combining. The bigger of the two was Contango Silver and Gold Inc. (CTGO:TSX; CTGO:NYSE), which had a sizable Alaska footprint, and it recently joined forces with the well-known Dolly Varden. The combined entity, in my view, is on track to become the go-to North American gold and silver name.

Contango Ore was run by an old friend, Rick Van Nieuwenhuyse, founder and chief of Novagold. Novagold was Canada's top-performing stock in 2001. Rick and his crew recognized early that we were heading into a major bull market in gold and silver back in the late 1990s. Novagold was among the first juniors I covered back in 2001.

The other side of Contango Gold and Silver, Dolly Varden, was also led by another old friend, Shawn Khunkhun. The combined Contango Gold and Silver (CTGO on both the TSX and the NYSE Amex) has Rick Van Nieuwenhuyse serving as CEO. Shawn Khunkhun has stepped into the President role at the merged firm.

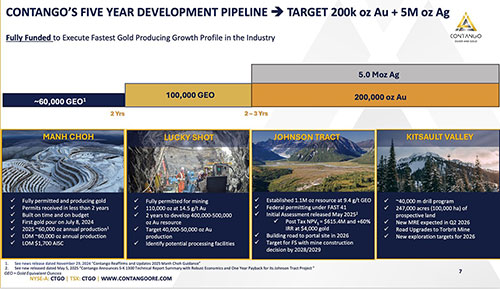

Rick contributed a producing gold mine to the deal along with two additional Alaska development assets. For 2025, Contango's 30% piece of the Manh Choh gold mine generated roughly $102 million in free cash flow for Contango. Kinross holds the other 70% and operates Manh Choh. Contango's leadership intends to channel cash flow from Manh Choh into advancing the company's three other gold and silver projects, meaning they can skip the endless private placements.

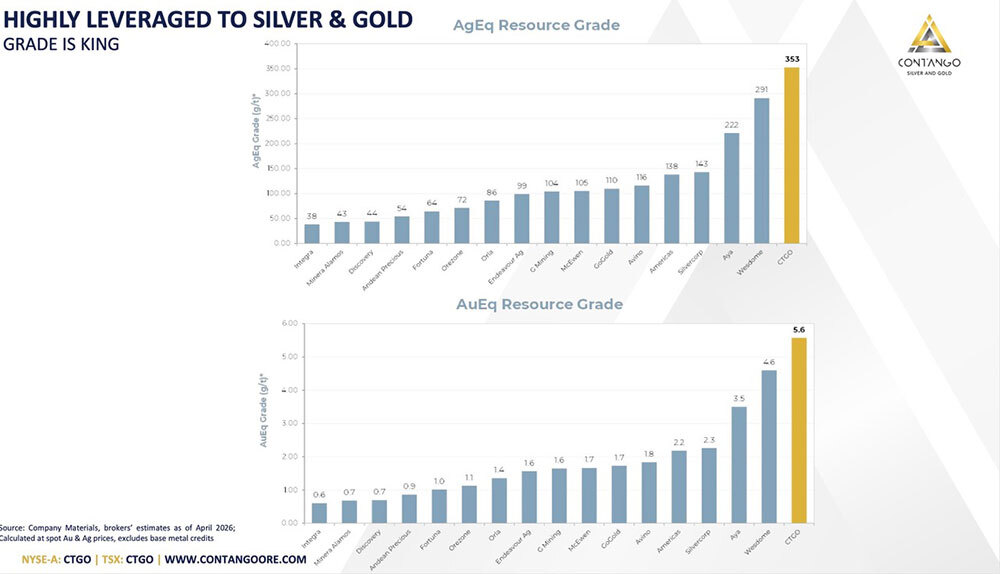

Manh Choh employs an uncommon mining approach known as Direct Shipping Ore, or DSO. The ore is mined, loaded onto trucks, and hauled 240 miles to the Fort Knox mill that Kinross runs. DSO trims upfront capital, shortens permitting timelines, and accelerates cash flow. They can pull this off because the Kinross/Contango JV zeroed in on high grade. When you've got grade, DSO is a quick and inexpensive route. CTGO holds the top grade among its peer group across all its projects.

That kind of free cash flow gives Contango the runway to push its three other projects forward at pace without constantly diluting current shareholders.

Contango's second Alaska gold property is the Lucky Shot Mine. Lucky Shot is a 100%-owned, fully permitted underground operation with both rail and road access. Historical district production averaged 40 g/t Au. Contango has kicked off a 20,000 meter infill and expansion drill campaign targeting 400,000 to 500,000 ounces by an H1 2027 Feasibility study. Management is aiming for production of 40,000 to 50,000 ounces of gold in 2028 from Lucky Shot using the DSO approach.

The third Alaska gold asset on the roster is the 100%-owned Johnson Tract, situated roughly 125 miles southwest of Anchorage. I'll lift this directly from the Johnson Tract write-up on Contango's site. "The JT Deposit is interpreted as an intermediate sulfidation epithermal deposit with volcanogenic massive sulfide (VMS) characteristics." Mineralization includes gold, silver, copper, zinc and lead. Johnson Tract has a 1.15 million ounce resource at 9.39 g/t AuEq. Just like Lucky Shot, the grade clears the bar for the low-cost DSO route.

Federal permitting is advancing under the FAST-41 protocol. The access road running from camp to portal is under construction along with the necessary environmental permitting work. A feasibility study is slated to support a mine construction decision penciled in for 2028/2029.

Dolly Varden's piece of the merger is the 100%-owned Kitsault Valley silver/gold project just over the border in BC's Golden Triangle. The Kitsault Valley project carries a 43-101 resource of around 65 million ounces of silver and one million ounces of gold. An updated resource is on deck for Q2 2026. The Kitsault Valley resource likewise qualifies for DSO shipping. Contango is planning a 40,000-meter drill program at Kitsault this year.

Contango's five-year roadmap targets 200,000 ounces AuEq in production plus another five million ounces of silver each year.

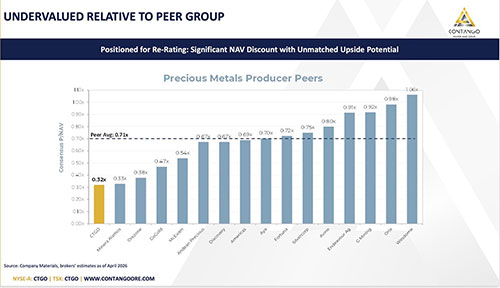

With a modest 30.75 million shares outstanding and $102 million in free cash flow for 2025, every share represented roughly $3.18 in free cash flow for 2025. Do I really have to spell out how cheap that is? On top of that, Contango trades at a hefty discount to its peer group with a slim 0.32 price-to-NAV ratio against a peer average of 0.71.

This merger has pulled off something I haven't seen from any junior I've tracked over the past 25 years.

- Every North American investor can now buy a dual-listed NYSE Amex and TSX name that brokers are free to recommend.

- CTGO holders get exposure to gold, silver and critical metals across Tier 1 jurisdictions.

- The 30% stake in Manh Choh kicks off enough free cash flow to develop the rest of the 100%-owned gold and silver projects without leaning on perpetual private placements.

- It's ridiculously cheap relative to its peer group.

- Institutional ownership of the stock is very high.

- They're sitting on around $100 million in cash to push projects ahead in 2026.

Contango is an advertiser. I have been a longstanding shareholder of Dolly Varden so I have exposure to the new Contango. Do your own homework.

Important Disclosures:

- Bob Moriarty: I, or members of my immediate household or family, own securities of: Contango Silver and Gold. My company has a financial relationship with: Contango Silver and Gold. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.