I was reading an interesting statistic the other day that said that "the ongoing US air war over Iran has been far more dangerous for US pilots than the bombing campaign against Saddam Hussein's Iraq in 2003, or Afghanistan in 2001." In fact, as I read on, this story revealed that up until the war in Iran, the last time the US lost a fixed-wing aircraft was on April 10, 2003, when a surface-to-air missile fired from a location in Baghdad took down an A-10 Thunderbolt II fighter jet.

While President Trump was telling the American people that "Iran is unable to carry on the fight" and Secretary of defense Pete Hegseth saying that "Iran's air defense capabilities have been destroyed", the Iranians proved conclusively that both statements were falsified due to the loss of as many as twelve fixed-wing aircraft lost to hypersonic missiles designed by the Russians and the Chinese with software modified by the Iranians.

The world has always operated on a dollar-based system of international trade, with the payoff being the "umbrella of defense" guaranteed by the U.S. military. This contract allowed Americans to build bases in places like Bahrain, Kuwait, and Qatar in order to project the aura of invincibility in the region. So, when Wall Street Journal articles are printed that detail mass evacuations of staff at embassies in Bahrain last month, one has to question the efficacy of the term "umbrella" if their air defenses were incapable of stopping the Iranian hypersonic missiles from targeting and actually hitting these bases. In fact, there are reports that claim that all of the American bases in the Middle East suffered "catastrophic damage" meaning that they are no longer usable landing zones for aircraft purported to be "invincible".

Downed US Aircraft in Iran

Herbert Hoover was once quoted as saying that "Wars are ordered by old men but fought by young men," and with the current president's approval ratings in freefall, it cannot be helpful that soaring diesel prices and rising mortgage rates are derailing his efforts to secure a Republican victory next November.

If there was one thing that contributed to the agony of the 1973-1974 bear market and recession, it was the sagging popularity of then-President Richard Nixon. The mainstream media led by a couple of cub reporters for the Washington Post (Carl Berstein and Bob Woodward) ran story after story about the Watergate break-in until impeachment became inevitable. In fact, it was eight weeks after Nixon's resignation that stocks bottomed, marking the end of the worst bear market since the Great Depression.

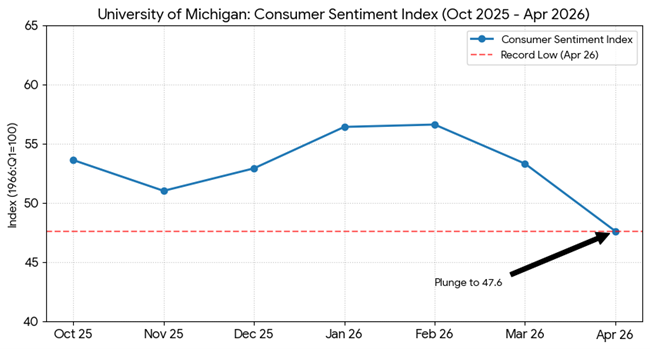

Investor sentiment rises and falls with presidential approval ratings, and one of the ways to gauge overall confidence is through the University of Michigan Consumer Sentiment survey, which here in April just hit a record low at 47.6. What this tells me is that while stocks are currently enjoying a relief rally, overall sentiment is not conducive to a prolonged recovery in prices.

This weekend, Vice-President Vance meets with the Iranian leadership to discuss ways to end the conflict, and if he is successful, then all eyes revert back to the economy, and with the inflationary ramifications of $100 oil, the big question will be on oil supplies and whether or not the war permanently hampered those supplies.

Judging from the late-week trading in oil, I would venture a guess as to the market's confidence in these so-called "peace talks" and with oil hovering just below $100/bbl., the odds of a lasting peace and normalized flow of oil through the Strait of Hormuz are long.

Also interesting is the action in the former market leaders where record highs were registered in the "AI' stocks all through 2025 and into January 2026.

With the double-leverage inverse ETF for the Magnificent Seven group of stocks (MAGX:US) down 37.1% from its November top, this ETF is still down 23.1% even after the best week for stocks in 2026.

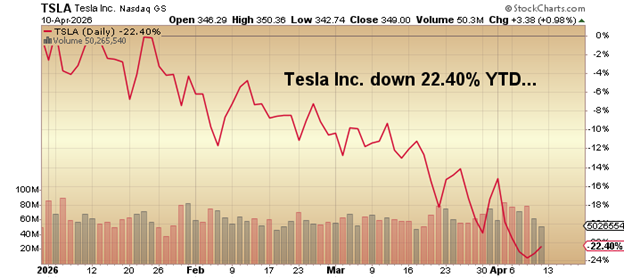

Then there was the mighty Tesla Inc. (TSLA:NASDAQ), the former favorite pastime for multi-billionaire soon-to-be-trillionaire Elon Musk, whose overpriced EV manufacturer will soon be relegated to "also-ran" status as his newest beach toy — SpaceX Inc. — is about to become the biggest IPO in Wall Street history.

Well, if you are a bear on Tesla Inc. as I am and a fervent opponent to the regulatory Hijinx of its founder, CEO, "product architect", and resident promoter/pitchman Elon Musk, then you have to wonder whether he can juggle two mega-deals at the same time. This is particularly relevant when Wall Street's familiar parade of carnival barkers over at CNBC have pivoted from "Elon Tesla" to "Elon SpaceX" as the next big story to talk about now that Bitcoin has fallen into disrepair and ignobility.

Whether it is the Mag Seven, Bitcoin, or Tesla, the leaders of the post-COVID liquidity binge, aided and abetted by the Fed and the Treasury department, are no longer leading, and as of April 10th, 2026, no real leaders have raised their hands or thrown their hats into the leadership ring. One might say that the gold miners have been taking on the leadership role despite the crash we had in March because it has been the miners that have roared back into gear.

Despite getting cut in half in March, the HUI:US actually went negative YTD at month-end but has since recovered to a highly-respectable 20.56% gain on the year. Compare that to the S&P 500, which is still negative despite this week being the best week of the year, largely as a result of the cease-fire.

Now, it will be curious to see what happens if Monday morning comes along and there is either no deal or a weak deal emanating from Islamabad.

Silver has been lagging gold badly since the lows of March 23 were seen. Whereas gold has been powering ahead in full recovery mode, silver has been limping along, albeit in an uptrend, but a far cry from the ascent we all witnessed in January. That moonshot in February was one for the record books and while it was fun for those that sold into the late-January madness (as I did, taking huge heat in the process), it was anything but fun for those that not only drank the Kool-Aid but actually gulped it as they are in now a World of Hurt with losses the likes of which cannot be redeemed simply by "holding on".

It is my sincere belief that silver will underperform gold and copper for the rest of the year but will test the territory above $100 by year-end. Whether we see record highs for silver will depend totally on the degree to which $100 oil pushes the U.S. economy into "stagflation" mode. If we get elevated inflation readings in the spring-summer period, accompanied by monetary and fiscal stimulus designed to win votes in November, then commodities, led by the metals, will all advance.

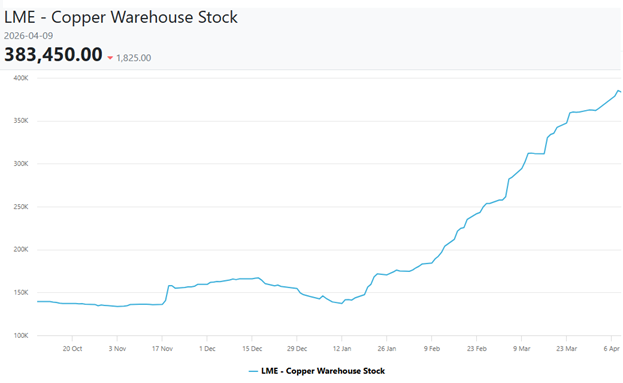

As for my favorite metal — copper — I love the manner in which it is retracing the crash to $5.20/lb. and is now cruising along at $5.85/lb. with $6.00 copper in its crosshairs and that against the backdrop of a cooling global economy and macroeconomic uncertainty flooding the landscape of every continent, irrespective of country.

The leaders in the metals' equity parade include my beloved Freeport-McMoRan Inc. (FCX:NYSE), which I bought back at or near the 2026 low at $52.30, along with a slew of June $55 calls options in a move I affectionately called the "Damn the torpedoes" moment. Since just after the Covid Crash took everything apart at the seams, I have been magically and mystically attracted to FCX:US and consider it the finest-run mining company in the world, with honourary respect to Canada's Agnico Eagle Mines Ltd. (AEM:TSX; AEM:NYSE) that runs neck-and-neck with FCX:US depending on the time of day and position of the moon and stars.

I declare "Advantage Freeport!" only because of its copper content because as a primary producer of gold, there are none that some even close to AEM. However, copper, like oil. Is found literally everywhere. Because of its universality, copper is where I have the major portion of my capital.

No market ever goes straight up, and one look at the LME inventories and I get the impression that copper is a great deal stronger than anyone imagines, and that is because it is rising in the face of bloated inventories. Contrarians would argue that this is exactly when you want to BUY copper, when the supplies appear to be ample and demand is weakening. However, when price action spits squarely into the face of elevated supply. I learned a great many years ago to "Always Trust Price" over any other contradicting input.

Inventories started to rise in November of last year and have since shown little signs of abatement (meaning "drawdown") but when you try to picture the amount of copper was used up (destroyed) during the five weeks of belligerence in Iran, you are forced to think "replacement" and that means that over the spring and summer of 2026, a great many drones,

missiles, and American ejection seats are going to be in full "Rosie the Riveter" production mode as weaponry stockpiles are reconstituted.

Make no mistake, if there is one vulnerability that the Chinese recognize about their country, it is that they must go "electric". The abject fear that Premier Xi must have felt watching his overdue oil shipments sitting idle, unable to get through the Strait of Hormuz, must have been palpable.

China cares not about Iran developing nuclear weapons; they care only about Iranian oil. Until their plan to rid themselves of dependence upon oil has been completed, they will toil feverishly to establish a nation-wide infrastructure of nuclear power, all totally reliant on electricity. With that reliance comes a circular reliance upon metals that conduct electricity, the most notable of which is copper.

I continue to hold and add to my junior developers and explorers with trading profits generated from other areas, and while it is maddening to sit and watch the junior names do absolutely nothing for weeks on end, experience has taught me to be patient. Take the example of G2 Goldfields Inc. (GTWO:TSXV) that traded from 2020-2024 in the sub-$1.00 range on skimpy volumes and notable disinterest. Then, in November 2024, it broke out above the $1.00 ceiling and for the past two years has been in a steady state of ascent, culminating with a daring offer from G Mining Ventures (GMIN:TSX.V) that has offered to acquire it for approximately US$2 billion in value.

Considering that it has produced a Preliminary Economic Assessment in which it estimates a gold resource of just under 4 million ounces. This means that a new benchmark for "value-per-ounce" calculations has to be in the USD $500 range. While perhaps GMIN:TSX overpaid for GTWO:TSX, but whatever the case may be, juniors like Getchell Gold Corp. (GTCH:CSE; GGLDF:OTCQB)), valued at less than USD $20 per ounce of in-ground gold, are most certainly mispriced in today's irrational market environment.

I am eagerly awaiting the results of the 2026 Masters Golf Tournament as much as I am awaiting the outcome of the weekend "peace talks," but while I am rooting heartily for Rory McElroy to repeat as champion, I am also rooting heartily for a serious resolution to the conflict.

Markets cannot function when global thermonuclear war is even the most remote of outcomes and one thing of which I am most fearful is a "WOUNDED EAGLE". The Americans have not played the ultimate battle chip, so if the Iranians continue to flaunt their prowess in the beaks of the American Eagle, they had better be prepared for the wrath of the American War Machine, which could be many, many magnitudes more calamitous than the world could ever imagine.

| Want to be the first to know about interesting Copper, Gold, Silver and Critical Metals investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers, contractors, shareholders, and/or employees of Streetwise Reports LLC (including members of their household) own securities of Tesla Inc., Agnico Eagle Mines Ltd., and Getchell Gold Corp.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: Freeport-McMoRan and Getchell Gold. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.