You've probably heard: gold has just had the worst month in its history.

Given that gold is older than the Earth itself, that's quite a long history.

What headline writers actually mean, even if they don't know it, is that: in US dollar terms, gold just had its worst month since 1971, at a stretch 1789.

But the US dollar is a bogus, fiat measure, and the sooner we start using constant money as our unit of account, the more truthful the world will become.

Gold hasn't changed. It doesn't. What has swung, violently as ever, is the price of fiat.

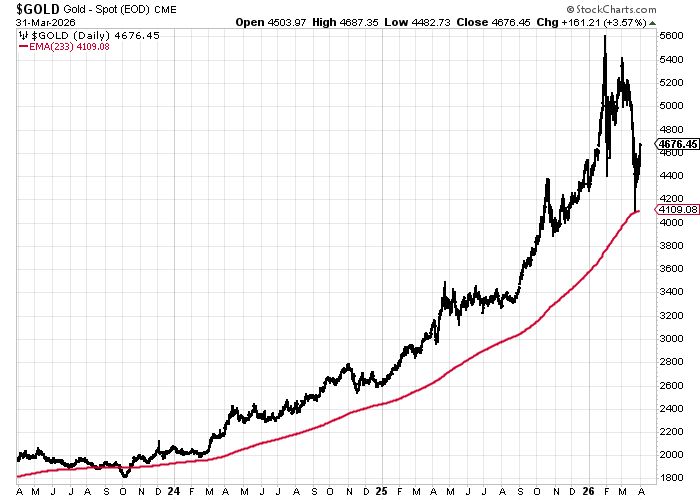

The move looks more extreme than it is because of where the month started. Gold began March near a high, around $5,400, and then sold off hard. A thousand-dollar swing sounds a lot, but after the run we've just had, it's not especially surprising. Indeed, I would go as far as to say it's normal.

Here is a 3-year chart of gold to put the March move in some perspective. I've also added a very useful indicator — the 233-day exponential moving average — in red.

233 is a Fibonacci number, and with roughly 250 trading days in a year, the 233 EMA works out as roughly the one-year average, but with the added magical quality that Fibonacci numbers often seem to have. In this case, it caught the exact bottom, as you can see.

What effectively has happened is that after a long run-up, gold has pulled back to the one-year average and bounced off it.

What we're seeing is normal behavior in a secular bull market.

Corrections feel violent at the time. They always do. But this is what bull markets do.

My view remains unchanged. We are somewhere in the middle of a multi-year move that ultimately takes gold into the $7,000 to $10,000 range.

The bigger point is not the chart, it's the backdrop. I keep saying it, but you absolutely must own some gold in your portfolio, particularly if you are in the UK, indeed anywhere in Western Europe. We have big, big problems coming down the tracks, and they are going to result in the further debasement of the national currency.

Debt levels are rising, not falling. Governments are spending more, not less. The cost of servicing that debt is going up. The political incentives all point one way: more issuance, more intervention, more currency debasement.

The UK is a particularly clear example. You can already see the strain in the gilt market, the pressure on public finances, and the complete lack of both political will and ability to address it in any meaningful way. No party is going to fix this. The system itself is broken.

There is only one way fiat money is going, and it's the same way it's always gone.

Treat pullbacks like this for what they are: opportunities.

If you don't own gold, you are relying entirely on a monetary system that is under visible strain. That in itself is a bet, whether you realize it or not.

Onto More Positive News — Or Is It? Squeaky Bum Time in Nicaragua

My largest position, and a core holding for many readers, is Metals Exploration Plc (MTL:LON).

Broker Hannam has just put a 37p price target on this 13p stock, implying roughly 3x upside. The current market cap is about £400 million.

The share price has pulled back sharply after its recent run to 19p to around 12–13p, largely tracking the ups and downs of gold.

The company has just issued a construction update, following a recent site visit to the main project in Nicaragua, La India, attended by major shareholders including Nick Candy.

Execution is everything now, and it's squeaky bum time.

The existing Runruno mine in the Philippines should produce around 50,000 oz in 2026. At $4,500 gold, that's about $225m of revenue. Using current cost guidance, that likely translates to $140m–$160m operating cash before overheads, and something like $80m–$90m after tax, G&A, and other costs.

That is strong cash generation, but it is not permanent. Runruno is a depleting asset. The ore body runs out late this year or early next, with closure likely in Q1 2027. Drilling at nearby Dupax has not delivered enough material to extend its life, so the mine shuts down.

The company will be left with a processing plant that can potentially be redeployed, but that raises the obvious: what project, where, and how much?

La India capex has now risen to $171m from $165m (it was forecast at $120m at acquisition, that's inflation, among other things, for you). The latest increase is mainly down to electrical infrastructure costs.

With $41m in the bank at the end of 2025 in addition to the Runruno revenue, funding is super tight. There is a $30m gold prepay facility (currently undrawn) and a $20m equipment loan in progress. It is marginal - hence the squeaky bum - but it does look fully funded, assuming Runruno delivers as expected.

The key positive is that the mine build is real and progressing. The project is about 42% complete against a planned 35%. The first gold pour is still targeted for December 2026. The crusher is installed, mill foundations are largely done, CIL (leaching) tanks are progressing, site infrastructure is about 77% complete, and the tailings facility is underway. Around 95,000 tonnes of ore are already stockpiled against a target of 500,000 tonnes, and pre-stripping is about 38% complete. That all reduces ramp-up risk.

There are two obvious vulnerabilities.

The first is the elution plant (the heat recovery circuit, which strips the gold off the carbon after it has been captured in processing). It arrives in Q3 and takes about two months to install. Any delays and the gold pour is delayed. Simples.

The second is power. The plant needs a stable grid connection and a substation in place before commissioning. A favorable deal with the Nicaraguan grid operator reduces cost and helps de-risk things, but it is still not entirely within the company's control.

Production guidance is now more conservative at 100,000 oz in 2027 rather than the previously touted 140,000 oz. That is probably realistic. Mines rarely hit peak output straight out of the gate.

But what we have here is a transition from a single, depleting asset to a new core asset, with exploration upside on top if things go well.

To get the re-rating, MTL needs to deliver La India on time, broadly on budget, and without too many operational mishaps. That sounds obvious, but many mining projects fail on at least one of those. There is also the jurisdictional risk. Nicaragua.

But if MTL delivers, a company producing 100,000 oz a year at costs around $1,500/oz is not a £400 million company. It's bigger.

It gets even more valuable if exploration success takes this to a district scale. Which is what we are hoping for.

It's squeaky bum time, but I think we're going to be ok.

If you'd like to read more from Dominic, you can sign up for The Flying Frisby here.

| Want to be the first to know about interesting Gold investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- Dominic Frisby: I, or members of my immediate household or family, own securities of: Metals Exploration Plc. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Dominic Frisby Disclosures: This letter is not regulated by the FCA or any other body as a financial advisor, so anything you read above does not constitute regulated financial advice. It is an expression of opinion only. Please do your own due diligence and if in any doubt consult with a financial advisor. Markets go down as well as up, especially junior resource stocks. We do not know your personal financial circumstances, only you do. Never speculate with money you can’t afford to lose.