In the past week, I have observed a legion of perma-bears all pointing to various technical and fundamental reasons for the bull market that began in 2009 to have ended.

The main culprit, of course, is the price of oil, gas, diesel, heating oil, jet fuel, and any other hydrocarbon necessary for the smooth operation of every economy on the planet. No amount of solar or wind is going to replace the loss of Qatar's LNG terminal thanks to an Iranian drone,

delivered with great precision and lethal force by the Iranian Air Command, an outfit claimed to have been eradicated by U.S. President Trump seven times in the past three weeks. As much as the Western media (owned and operated by those sympathetic to Israel) continues to "report" on the Middle Eastern news front, the bias will not be a lot different than the news reports from Iraq during the first Gulf War when the Iraqi spokesman, known affectionally in the West as "Baghdad Bob" went on the air every few hours to assure his citizens and the world that Iraq was indeed "winning the battle" as building were exploding behind him.

The events of the past four weeks were supposed to have been quick, lethal, and surgical in order to bring the Iranian military to its knees but with the Strait of Hormuz impassable except for a few favoured China/India/Pakistan-bound vessels, the war with Iran appears to have been a case of underestimation of the preparedness of the Iranian forces and leadership.

The American/Israeli assault group claims to have taken out the main leadership group through surgical air strikes, and yet the Iranian theocracy lives on, defending the nation as best it can and lashing out at any Middle Eastern neighbour hosting American bases. The latest news has three more warships headed to the region with approximately 4,400 to 5,000 U.S. Marines ordered to the Middle East. While the Trump administration has not officially confirmed a mission to seize Kharg Island, multiple reports indicate it is a "high-risk, high-reward" option being considered to gain leverage over Iran and reopen the Strait of Hormuz.

These are not moves indicative of a quick resolution of the conflict any time soon, and certainly no reason for the U.S. President to show up in a bomber jacket on the deck of one of the carriers declaring "Kuwait is liberated. Iraq's army is defeated. Our military objectives are met" while a banner reading "Mission Accomplished" hung in the background.

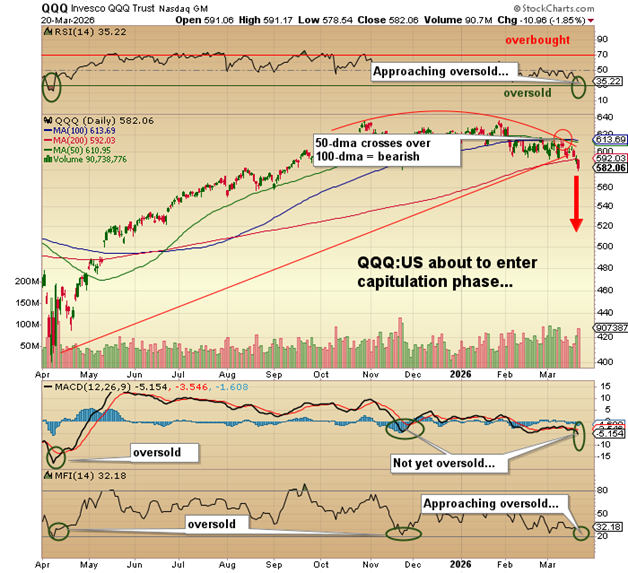

What the markets were telling us last week was that they do not believe any of the claims being made by the White House and that the "mission" to affect regime change in Iran is not going to happen overnight. Most certainly, with "boots on the ground" about to enter the fray, markets are starting to take actions that reduces leverage and hedge portfolios. That is not the fabric with which bull markets exist, and with valuation levels 2-3 standard deviations above the norm, there is a great deal of room for profits to be taken. On that note, one look at the chart of the S&P 500 since March 2009, and you can picture just how enormous the profits are remaining in portfolios. Even a minor correction to test the Covid Crash lows would be catastrophic.

Support for the S&P 500 is at 5,500 and 4,000, respectively, which are merely bounce points allowing portfolio managers to rebalance risk. Alas, the majority of PM's these days have never been through a prolonged, drawn-out bear market like 2001-2002 or (God forbid) 1973-1974. They have seen the practice of "buying the dip" rescue them every single time stocks began to leak oil, thanks largely to the habit of the Fed and/or the U.S. Treasury injecting liquidity into the system just as the breakdowns were starting to unfold. Bullets were dodged in 2008 and 2020 by trillions of dollars of magical, make-believe "money" floating down from the skies and winding up on the balance sheets of the money centre banks whose batteries of traders applied their newfound liquidity to the task of rescuing the PM's P&L statements from surefire ridicule and bonus evaporation.

So, the main question I must answer is this: "Do investors have enough time to wait for the inevitable bounce from deeply oversold conditions in order to reduce risk and establish hedges?"

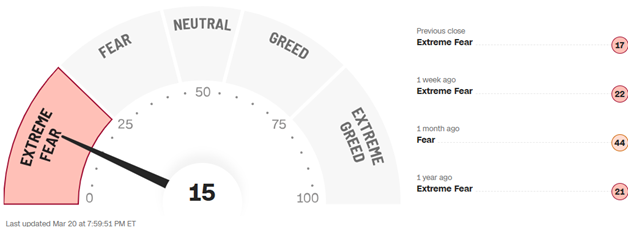

Based upon the sentiment indicators that I follow, most of the major averages are approaching or have arrived at "oversold" status with the CNBC Fear-Greed Index now solidly in <EXTREME FEAR> at 15. I have seen it lower at the bottoms in April of last year at 4 and at the Covid lows of 2020 at 2, so while investor angst is rising sharply, it is not yet at the "Back-up-the-truck" stage.

I believe that we are in the throes of a leadership change in the global markets that may take another few months to play out, with the ultimate conclusion being a rise of commodities as the new leadership group, replacing all of the former leaders like "AI", Bitcoin, and Mag Seven names with new leaders from the hard assets camp.

That is not to suggest that Agnico Eagle Mines Ltd. (AEM:TSX; AEM:NYSE) or Newmont Corp. (NEM:NYSE; NGT:TSX; NEM:ASX) will assume the role of Newmont Corp. (NEM:NYSE; NGT:TSX; NEM:ASX) or Meta Platforms Inc. (META:NASDAQ) immediately but major global miners like BHP Billiton Ltd. (BHP:NYSE; BHPLF:OTCPK) or Freeport-McMoRan Inc. (FCX:NYSE) could easily grab hold of and run with the mantel of market dominance in the same manner that NVidia suddenly leapt out of a moribund pack of video game chipmakers and seized the moment in a "Carpe Diem" feat of monumental history.

Moves like the one shown above are not commonplace, but they do occur. Bitcoin made the same advance off the lows in 2008 with "story stocks" like Tesla Inc. (TSLA:NASDAQ) and GameStop Corp. (GME:NYSE), and Strategy Inc. (MSTR:NASDAQ), all making millionaires out of paupers in their heydays, followed by making millionaires out of billionaires once the bloom came off the proverbial rose.

However, since corrections take everything down with them before a new leadership group can emerge from the mire, it is logical to assume that this current period of weakness will not be friendly to even the hard asset crowd, which is why my portfolio is never without some form of hedge to offset market drawdowns. It does not prevent my portfolio from giving back gains, but it does "soften" the drawdowns. In prior times, I would look at the myriad of technical breakdowns all happening with alarming and simultaneous frequency this past week and add to my hedges aggressively but since this sell-off in stocks and spike in oil has been event driven, history has taught me to look out to the end of hostilities rather than listening to all of the podcasting grave-dancers calling for a crash.

There is no doubt that a prolonged period of rising energy prices will crush the global growth narrative, and that will undoubtedly explain the large rise in copper inventories that I have been noting in recent email alerts. However, infrastructure, including missiles and drones, will need to be replaced and rebuilt, and that will force a drawdown in copper inventories as the munitions factories go to work.

If there is one positive side-effect to the events of the last four weeks, it is that the protesters who want to defund oil and gas and move to carbon-neutral energy sources are about to learn what a world without hydrocarbons actually feels like. All that electricity required for those fancy Teslas is going to cost a great deal more if the current is being generated by the burning of natural gas. If anything, it is going to accelerate the move to electrification as these younger generations of tree-huggers suddenly find their heating bills rising faster than their Starbucks bills, which will certainly be a terminally corrosive event for most of them but a huge boost for the copper producers.

Actionable Ideas for Next Week

This is an add-on to the Weekly Missive released last evening because of the epiphany I had while watching the Carolina Hurricanes thump the Leafs in what has become a throwback to the 2015-2016 season when the team was "tanking" late in the year in order to secure the first overall pick (which became current Leafs captain Auston Matthews).

I expect markets to rally feebly to work off the current oversold condition. We might see further weakness in the miners over the next three sessions, so I am scaling into the junior gold ETF (GDXJ:US) and one senior copper producer, Freeport-McMoRan Inc. (FCX:NYSE), while placing bids for a number of the junior developers under the market. I did not trim any of the juniors during the big run-up in January, so I need not make many moves there, but since the seniors always are the first to rebound, I am better off focusing on the quality names first if I think there is going to be a reflex rally.

As for the gold and silver miners, I did not chase any of them during their rebound off the crash lows of early February. Instead, I cautioned you all to await the inevitable re-test of those lows around $4,400 gold and $62 silver. With the Friday low of $4,480 gold and $67.75 silver, there might be a further follow-through on Sunday night through Monday morning but by the time they open for trading at 9:30 on Monday, I will have a pretty good idea if the buyers are circling or whether there is more selling left.

I am hoping that there is more leverage to be unwound next week, and judging from the huge advance in the gold and silver miners in January-February, there could certainly be more profit-taking. With instructions laid out in the Special Situations Bulletin of last week, I have completed the following:

For more aggressive speculators:

- BOUGHT 50% (25 calls) position GDX June $75 calls @ $10.00

Add an additional 50% at $8.00 by Wednesday.

I was not able to complete the following:

- Buy 25% position GDX:US @ $76.00

Add 25% each day that follows until Wednesday.

It traded down to $78.74 on Friday and might hit my $76 target entry level early next week, depending on what I see on Friday night.

I also issued the following:

- BUY 25% position GDXJ:US @ under $100

Add 25% each day through next Wednesday.

Nothing done. It traded down to $102.88 after opening at $109.57, so the term "crashing" is certainly appropriate, which is why I use a "scale-in" approach.

For speculators:

- BUY 50% position GDXJ June $100 calls @ $12.00.

Add 50% @ $9.00 next week.

Nothing done. It was $14.10 bid on the close on Friday. Again, I will know what my chances are of an entry at $12 by Sunday evening's electronic session.

On the copper front, there are a number of issues that should be bought:

Freeport-McMoRan Inc. (FCX:NYSE)

- BOUGHT 50% (1,000 shares) position FCX:US @ $52.30

- BOUGHT 50% position (25 contracts) FCX June $55 @ $4.50

Ivanhoe Mines Ltd. (IVN:TSX; IVPAF:OTCQX)

- BUY 50% position (2,000 shares) @ $7.50

- Add remaining 50% @ $6.00 by Wednesday

Fitzroy Minerals Inc. (FTZ:TSX.V; FTZFF:OTCQB)Fitzroy Minerals Inc.

- Buy 200,000 FTZ:TSXV/FTZFF:US @ CAD $.35 / $.26 good through Wednesday.

Energy

I have already reduced exposure to oil and increased exposure to natural gas, so I am sitting with three names that will benefit if the Middle East conflict is prolonged or spreads.

In this sense, the energy names are a hedge.

Market Hedges

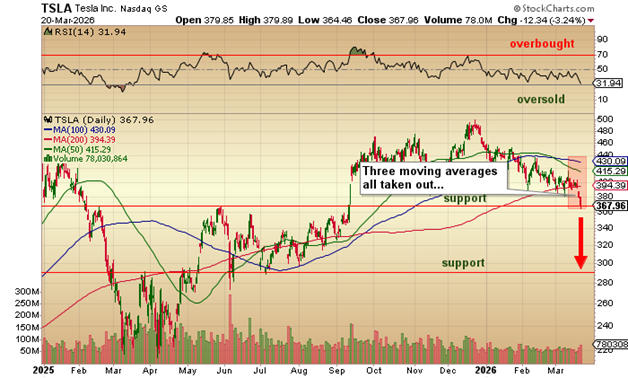

The only actual hedge that still remains, aside from the energy names, is the T-Rex 2X's Inverse Tesla Daily Target ETF (TSLZ:US), which I own from an average cost base of $17.51 on 6,000 shares. It has traded as low as $9.735 on December 22 of last year, but I refused to dump it, because as Warren Buffett famously said, "The only time you find out who is swimming nude is when the tide goes out."

So, with stocks correcting and leadership rotating, the Mag Seven now in full retreat, I have always considered Tesla Inc. to be not only in breach of GAAP (Generally Accepted Accounting Practices) but also negligent on multiple occasions of the CEO (Elon Musk) making "forward-looking" statements that verged upon outright "fabrications."

For these reasons, I have determined that before very long, investors would be become jaded over the "Musk Effect" and look at Tesla Inc. for what it is, a failed EV manufacturer losing money (net of carbon credits from Uncle Sam) that is losing market share to China's BYD, where in Europe they are the only EV on the road.

On Monday, watch TSLA closely as it has now taken out the three major moving averages, the 50-dma, the 100-dma, and the 200-dma, leaving literally no lines of support left other than the March 2025 peak and the May 2025 peak (which it just broke).

A move to under $300 takes the TSLZ to around $40. I also own (in a non-public account) another small position in the TSLZ April $15 calls that I bought last week at $1.90. They closed at $2.35 on Friday, but if TSLA crashes next week to under $300, these calls are probably worth $25. With an RSI at 31.94 for TSLA:, the odds favour a reflex rally by later in the week but if we get a waterfall capitulation-type crash starting early next week, the one stock that has nothing in the way of technical support is the failed EV manufacturer, Tesla Inc.. As a limited risk speculation on a waterfall decline, these calls could represent a low-risk shot on continued weakness in the Mag Seven and Tesla.

Buy only as much as you can afford to completely lose IF you decide to take the plunge. Risking a few thousand dollars to earn a ten-bagger is a justifiable speculation, especially if the tide is actually going out.

| Want to be the first to know about interesting Gold, Silver, Copper, Technology and Critical Metals investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers, contractors, shareholders, and/or employees of Streetwise Reports LLC (including members of their household) own securities of Agnico Eagle Mines Ltd., Tesla Inc., and Fitzroy Minerals Inc.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: Freeport-McMoRan and the Van Eck Junior Gold Miners ETF. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.