One of the toughest parts about being a published newsletter writer is that once an idea or comment goes into print, it is locked and loaded into perpetuity. You cannot retract it or redact it or even subtract it; you own it.

CNBC's Jim Cramer is a great example of a financial services industry "showman" that every morning that the markets are open occupies a seat giving him full vantage point to the minds (and wallets) of millions upon million of investors, many of whom are sadly lacking in both experience and common sense. I do not think that Mr. Cramer appreciates it when his now-infamous call on investment bank Bear Stearns in the fall in June of 2007 with the share price at around $62 gets trotted out time and time again. His message to viewers went like this:

"No! No! No! Bear Stearns is fine. Do not take your money out. Bear Stearns is not in trouble. If anything, they're more likely to be taken over. Don't move your money from Bear. That's just being silly. Don't be silly."

By March of 2008, Bear Stearns was taken over at $2 per share after the regulators put a gun to the heads of the major money-centre banks and forced the deal in order to keep the sub-prime contagion from spreading any further (which it did anyway).

It has been eighteen years since Bear Stearns went belly-up yet Cramer still has his job and his reputation intact. There are social media vigilantes out there that have created a mock ETF called the "Inverse Cramer" with its main directive being to take the other side of every Cramer trade pumps to a investment world starved for "the next big trade" and from what I read, it is one of the best-performing paper trades on the planet.

Back in January, I wrote an article for my subscribers that called for the shorting of silver at around $50 an ounce which was quickly covered at a small loss. About two weeks later, in the $75-80 range, I tested Albert Einstein's "Theory of Insanity" by repeating the trade only to wind up "with the same negative outcome". By this time, my better half and my beloved dog Fido had retreated to the safety of the root cellar where an inside lock was recently installed by a local on one of the days when I was distracted by a screaming silver price.

Reaching desperately for solace from complete humiliation and embarrassment, I elected to remain silent on the matter of a 90 RSI for March silver while the army of silver newsletter bulls and armchair quarterbacks as well as dozens of podcasters all scrambling to interview Michael Oliver or Rick Rule or Tavi Costa on the slim chance that viewers could for the fiftieth time in January hear the phrase "$500 silver by summer!!!!" I was in the business back in 1980 and in 2011 the last time that silver went "parabolic" and while a few of the early investors made fortunes gliding slowly and silently off into the distance with little fanfare and ample grace. I also heard the stories – YEARS LATER – from elderly men and women that had plunged their life saving into silver during the run to $50. They would all confess to being "too embarrassed" to admit such folly until the fullness of time had passed and old wounds healed and were forgotten.

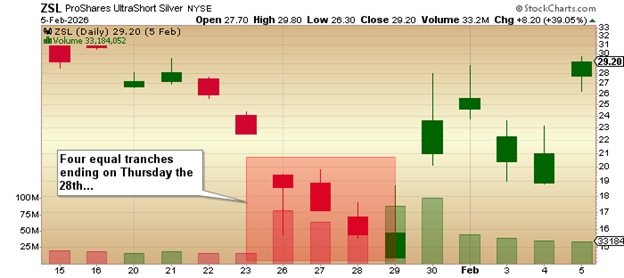

By the third week of January, I was flat all my physical silver and stinging from the reputational wounds of the mistimed silver shorts, attempted not once but twice leaving me terrified of the narcotic lure of the phrase "three times a charm". It was keeping my eyes glued to the quote screen as silver lunged through $80, 90, and then finally, the magical $100 per ounce. Now insane with temptation, I took a sledgehammer to the locked medicine chest and a crowbar to the lock on the liquor cabinet (the keys were now in the root cellar) and underwent the necessary preparations that would allow me to take the final plunge into the Dark World of "bearish silver".

I told subscribers on the weekend of January 24-25th that starting Monday morning, I was allocating 25% of my risk capital to the ZSL:US (the "short silver" 2X's ETF) and that I would buy four tranches by Thursday's close to arrive at a blended average price for a vehicle that had

dropped 93% in the past year.

Taking my queue from the words of Admiral David Glasgow Farragut, I screamed "Damn the torpedoes! Full speed ahead!" and launched into "The Battle for Investment Redemption" buying four equal tranches from Monday until Thursday while gnawing my fingernails to the cuticles and applying shock treatment to my liver.

By Friday morning, with the die summarily cast, I awoke to the sounds of robins singing wistfully by the shores of the lovely Scugog Swamp. Groggily from a fitful rendition of what might be called "a series of naps" as opposed to a "sleep", I glanced at my phone and clicked on the investing.com page that has all my futures quotes only to find the rampaging silver market in full retreat. My last tranche of the ZSL:US was made as March silver was scaling the $115 per ounce level and by the time I retired that prior evening, it was through $120 and showing nothing in the manner of

fatigue. As they say in the world of Toronto Maple Leaf's captain Auston Matthew's season, "the rest is history" as silver has failed to see the light of day above $100 since that fateful week in late January. With the crash in silver, I was able to recoup all the small losses on my earlier silver shorts and bank a good profit. However, at what price comes victory when one must fight the demons of alcohol and painkillers, welcomed escorts through the minefield of reputational capital recovery?

PDAC Curse

All through February, I had to stifle myself for even whispering the term "PDAC Curse" because investors in every nook and cranny of world of speculation would glare at me with animated vitriol if I even hinted at the junior miners being somewhat ahead of themselves.

Every time I clicked on a website or downloaded a podcast from the start of January to the end of February, there was some raving lunatic "influencer" like Michael Gentile or Tavi Costa talking up his book with shameless fervor and unlimited certainty beseeching viewers to throw all semblance of caution to the wind and buy every junior gold or silver deal regardless of their AISC limitations because rises in underlying metal prices would eventually skate every project completely onside and into the black. Even silver projects located next to the North Pole with $100/ounce costs of production were a "surefire bet" because "silver at $500 by summer renders them insanely profitable!!!".

Now, make no mistake. I, too, have been a shameless bull on more than a few of the names in my book, but my assumptions have always included more rational numbers as guidelines for economic viability. I own a few copper names but if any junior I own has a decently-sized resource, I am using $6.00 Cu as my benchmark, not $10 or $15 as I have read in recent posts by new arrivals to the party.

There is nothing wrong being excited and showing the world that excitement, especially when we bulls in the metals arena have been subjected to cheerleading and victory lapping by crypto and "AI" and software and the S&P 500 all topped off by the ever-annoying QQQ:US dip-buying techaholics that just know for sure that technology will not only grow to the Heavens but also cure cancer and put a man on Venus by the time it takes Elon Musk to turn Telsa profitable.

Every March-June since I can remember, the TSX Venture Exchange undergoes a correction of all of those hideous excesses that accompany overwhelming bullishness of the pre-PDAC warm-up. From on-site reports from PDAC 2026, the halls of the Toronto Metro Convention Centre were chocked full of fuzzy-cheeked generalist portfolio managers, all well rehearsed in geo-babble and memorized "rock talk" trying desperately (but in vain) to sound like the actually knew the difference between a porphyry and a porpoise which they most certainly did not.

For the legions of Vancouver and Toronto paper-hangers that arrived at PDAC with overflowing core boxes matched only by their overflowing sell orders of their junior mining issues, PDAC 2026 was a never-ending lottery win. Junior miners that a mere one year ago were trading at a nickel had miraculously metamorphosed into "value propositions" at $1.00 per share. Most of these silver-tongued devils came into 2026 driving their 2016 Toyotas but left PDAC driving brand new Porsches as once again, the wonderment of the U.S. dollar "debasement trade" corals the herds of unsuspecting newbies into wallet-removal stations also labelled "exhibitor booths" by the PDAC marketing wizards.

Arguably, the one stellar copper deal of 2025-2026 has been Marimaca Copper Corp. (MARI:TSX; MC2:ASX) whose share price bottomed last April 10th at USD $3.07 per share. Topping at USD $9.87 on January 29th, the stock is now down over 33% in two short months but not before closing a USD $57m funding late last year.

Is MARI/MARIF worth any less than the price it hit in late January than the level upon which it closed last Friday?

Of course not.

GGMA favourite Fitzroy Minerals Inc. (FTZ:TSX.V; FTZFF:OTCQB) reported the first tranche closing of an $18.8m funding on Friday at CAD$.50 with the stock going out at CAD $.38 for the week, 24% off the financing price and 48% off its 52-week high. With two major projects being developed/explored in mining-friendly Chile, was it a "sell" at $.73 back in January? I think not given the high prospectivity of their two major copper projects.

Alas, the final arbiter of value is the bid-offer on the stock price and since we all know too well that the trading pit can be a cruel master to all that dream of untold riches through the drill bit, the juniors that trade on the TSX Venture or the CSE are once again the reality that shouts "It's never really different this time or any other time" that rampant speculation takes over the helm of the valuation vessel. You can kick yourself as a newsletter guy for failing to issue a "Sell" on those specific juniors that are now in the tank but perhaps using an inverse silver leveraged ETF was enough to protect value. (Or not.)

Oil and Gas

Coming into 2026, I added two oil and two natural gas producers to my GGMA 2026 Trading Account as anchors to portfolio volatility. Between the shorts, the long volatility, and the energy names, the portfolio is down a little over 8% YTD largely caused by the pullback in FTZ/FTZFF which is still ahead but not nearly as much as when New Year's Day rolled in. Since I rolled the dice on the Buen Retiro Copper Project morphing into "Candelaria II" in 2026, I am now seriously overweight the name which means swings in its price has a debilitating effect on portfolio performance.

The selling wave that started during PDAC will need to run its course and it is my measured opinion that it will coincide with a cease in hostilities in the Middle East. Since trying to read the mind of the most powerful man on the planet is nothing short of impossible verging upon implausible, I can only hope that the juniors can look beyond the geopolitical noise and focus instead on the individual assets that moved them onto the radar screen to begin with.

While $200 oil certainly helps my energy and volatility allocations, it does not do anything positive for the metals or the juniors exploring for and developing them.

| Want to be the first to know about interesting Oil & Gas - Exploration & Production, Copper and Gold investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers, contractors, shareholders, and/or employees of Streetwise Reports LLC (including members of their household) own securities of Fitzroy Minerals Inc.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: ZSL and Fitzroy Minerals Inc. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.