Some of the greatest investment passes of the past century were made by individuals who thrived upon ignoring conventional wisdom and storming headlong into thoroughly contrarian trades, content to fly in the face of the current popular narrative. Not only were these trades 100% "contrarian," but they also usually inhabited the vast majority of the portfolio, a condition that could render careers defunct should the trade go offside for as much as a 15-minute coffee break.

Sir John Templeton ran Global Investments back in 1939, and at the onset of World War II, as fear gripped markets and most investors expected the U.S. economy to suffer further, Templeton bought 100 shares of every U.S. company listed on the New York Stock Exchange that was trading for less than $1 per share. Many of these were on the brink of bankruptcy, but the diversified bet paid off handsomely, launching his career and validating his "buy at the point of maximum pessimism" philosophy. He also invested heavily in Japanese stocks in the 1960s when they were largely ignored by Western investors, generating massive profits.

A second example would be George Soros, who, while running the Quantum Fund back in 1980, made over a billion dollars in a single day by shorting the British pound. He correctly anticipated that the Bank of England could not defend its currency's fixed exchange rate within the European Exchange Rate Mechanism (ERM) due to weak economic fundamentals. When the UK was forced to exit the ERM and let the pound devalue on "Black Wednesday," Soros's fund profited immensely.

However, the most recent example and one that many current market players recall was the daring move by the noteworthy heroes of the 2007-2008 Great Financial Crisis — Michael Burry and Steve Eisman — who decided to bet against the American housing market at a time when the vast majority of investors all believed unanimously that "house prices never go down."

As depicted in the excellent film "The Big Short," these brave souls went through literal hell having to sit patiently as mortgage default rates began to soar while the brokers holding the contracts on their short positions refused to adjust their "marks" (bid prices for short positions) until they had unloaded all of their in-house their liability. Nevertheless, after purchasing credit default swaps (CDS) to bet against mortgage-backed securities, the move required significant patience and conviction as their positions lost money initially, making investors nervous. These daring bets ultimately resulted in hundreds of millions in personal profits and billions for investors when the market crashed in 2007-2008.

There have been many other instances of unbridled bravery that can be referenced, but there is one fundamental difference between the famous Rothschild quote, "Buy them when there is blood in the streets" or my favourite from the old Chicago Board of Trade, "when they're yellin', you should be sellin'" and when they're cryin' you should be buyin'."

These expressions were all valuable guidelines prior to the popularization of Fed interventions, interferences, and bailouts, all designed to neutralize the impact of market corrections. When Hank Paulson got on one knee and begged Congress for an $875 billion bailout for the N.Y. money-center banks (while his sizeable position in Goldman Sacks stock was being held in escrow in a blind trust AND on the verge of vapourization), he was setting the tone for the institutionalization of "moral hazard" into the minds and actions of every basement-dwelling, fuzzy-cheeked day-trader on the planet. Since the 2009 rescue of the criminalized U.S. banking fraternity, the concept of "contrarian investing" has been rendered ineffectual because there is never any "blood in the streets" or "cryin'" because the Fed has taught an entire generation of investors that no matter what the news is, stocks will be rescued. It was the genesis of the "Buy the dip" generation.

In the past six years, U.S. investors endured a global pandemic after which the entire global economy was shuttered, and thanks to both fiscal and monetary stimulus, bailouts, and profligate behaviors, every downturn was repelled. The natural capitalist process, where bad businesses fail and good businesses thrive, has been derailed, and now the penalty for poor corporate decisions is interventions and bailouts, which actually weaken the lot of the well-run businesses as they are constantly embroiled in pricing wars with companies under the care-and-maintenance of the federal government.

In the same time period, they have seen a couple of big regional banks fail due solely to high-level mismanagement triggering the prospect of contagion (which the Fed absolutely detests) resulting in the passage of the "Bank Term Funding Program" which allowed the regional banks that were forced to buy all the low-yielding bonds floated by the treasury not be required to meet margin calls for leveraged U.S. government bonds that were trading suddenly and without notice at fifty cents on the dollar.

And yet, the S&P has been setting record highs every few days with rarely as much as a 10% correction, and even when it approaches one, the Fed sends out gangs of governors and regional presidents to cheerlead the NASDAQ. Total chaos at every turn. . .

In the end of the book "Never Cry Wolf" by Farley Mowat, there is a captivating scene where a herd of reindeer are running to elude the wolf pack and after the melee ends with several kills that feed the wolves and their pups, the next day Mowat visits the carcasses of the dead reindeer and breaks apart a leg bone of one of them only to find it riddled with disease. His conclusion was that the wolves were a necessary part of nature in their ability to "cull the herd," thus strengthening the bloodline by allowing only the fittest of the species to procreate.

We have heard similar stories about the degradation of Yellowstone National Park, where bounties on wolves caused severe degradation of the ecosystem due to overgrazing by the elk herds. With the defoliation came the loss of marshlands and many species of insects, waterfowl, fish, and reptiles. It took over seventy years for government officials to reintroduce wolves to the park, causing a sharp reduction in the elk and a rejuvenation of the ecosystem, which happened within a few seasons. This is exactly what is needed for the global capitalist economic system. Governments need to get out of the habit of trying to "manage" the economy and let the economy "manage" itself.

The practice of "contrarian investing" is not exactly dead because it still works effectively in all segments of the marketplace that are deemed immaterial to the government and/or central bank interventionalists. If one looks at the chart depicting the Goldman Sachs Commodity Index versus the S&P 500 dating back to December 2000, one can see clearly how stocks have been coddled and coaxed higher at every turn while commodities, representing "hard" versus "paper" assets, have lagged miserably primarily since the Great Financial Bailout.

If the world has indeed entered into a "Fourth Turning" — a recurring period of crisis in the Strauss-Howe generational theory, where society faces major challenges like wars, economic collapse, or political upheaval — then it should also be classified as a "Kondratieff winter," a deep depression phase in a long-term (around 50-60 year) economic cycle, theorized by Nikolai Kondratieff, marked by massive debt write-offs, deflation, collapse of asset bubbles (like stocks/real estate), high unemployment, and social strain, following an "Autumn" speculative boom and preceding a "Spring" recovery, acting as a painful but necessary reset for new innovation, much like the Great Depression.

The financial media seem hell-bent-for-leather on driving home the "American Exceptionalism" mantra, which applies to every member of Western Civilization and especially those that pride themselves as "capitalist communities," but the reality is that the term "capitalism" cannot be applied to every country in the western hemisphere. In fact, the country that prides itself as the flag bearer for capitalist values — the United States of America — has almost as many socialist programs in place as does Sweden or Canada, including food stamps and Medicaid, which would certainly please Karl Marc were he still alive.

As I first wrote of in the GGMA 2000 Forecast Issue, the U.S. government has only one asset that it carries that can be repriced, and that is its gold horde. The only method of avoiding default on treasury debt is to "meet the margin call," which is to say that they must put up more equity in order to secure the loan — the US$38 trillion loan — that threatens to derail "American Exceptionalism" at the next curve in the track. Re-pricing gold is what the citizens want to see, but the reason it will not happen in the near-term is that the vault holders are terrified of the inevitable audit that will be required before the foreign buyers of collateralized treasuries agree to the terms. If that gold alleged to be in Fort Knox has gone AWOL, the U.S. dollar goes to zero in a heartbeat.

Tightropes

The man with the balancing rod walking across the Niagara gorge in 1960 was Nik Wallenda, and I was only seven years old, but since I was in a hockey school run by Stan Makita in St. Catharines that year, I was able to see the man taking an incredible "career risk" inching his way across the river. The Niagara River is a BIG river as it is the only way Lake Erie (the tiniest of the Great Lakes) can empty itself into Lake Ontario, it thunders over the ancient sedimentary rocks to the river below sending cloud after cloud of moisture skyward that could not be pleasing to a man walking in a white leotard and matching ballet slippers with only a fifteen foot balancing rod as security.

That was the feeling I had on October 17 when I determined that the gold market was gripped by a mania not seen since 2011, resulting in my "sell" signal that was immediately scoffed at by the legions of armchair "newbie" experts who only learned how to spell "debasement" last month with the help of ChatGPT.

I answer almost all emails either sooner or later, after which I keep the ones that are particularly relevant while binning the ones with little or no use. After reviewing them all, I skulk my way back to my desk and muster up all semblance of courage and I try with great angst to assess all aspects of all markets affecting my "highest conviction trades" and while sometimes I am right and sometimes I am wrong, the win-loss ratio is has been on the plus side for every year since I launched the letter in 2020.

This is why I am joining Mr. Wallenda on the high-wire of career risk and making a rather aggressive call. I am calling an intermediate-term top in silver.

"Whenever the trend of any financial asset or commodity moves from gradual (rate of incline or decline) to vertical, that trend is entering the terminus stage." Such is a pattern that I have observed over the past few decades, so let us take a gander at a couple of tops that were preceded by trendlines that went from "gradual" to "vertical."

First, there is gold.

Gold

Gold prices began the year around the $2,600 mark and embarked on a gradual advance that took it to $3,500 before stepping back under $3,000 during the early April "Liberation Day" shenanigans that nearly decapitated the global bond and stock markets before the White House pivoted from austerity to growth as soon as they got their month-end statements from their local financial advisor. It resumed that gradual uptrend all through the spring and summer until late August when Chairman Powell auspiciously hinted at pending rate cuts after several quarters of temperance in light of the inflationary impacts of the tariffs.

Then, in early October, gold went into a near-vertical to vertical ascent that resulted in daily, weekly, and monthly RSI readings moving to decisively overbought conditions and stayed there for 56 days before the October 17 "key outside reversal day" marked the top. It has been 50 days since prices peaked, and until the HUI:US joins gold in a solid close above the record high of 693.10 with February gold higher than $4,433, I will continue to fade rallies.

Next, I look at the non-precious-metals arena where another example of this gradual-near-vertical-vertical topping pattern was Nvidia Corp. (NVDA:NASDAQ), whose chart followed a similar pattern of gradual ascent from June until mid-October and then suddenly, it bolted out of the starting blocks and screamed from $180 to a record high at $212 in a matter of days as animal spirits became enlivened after markets survived the normally weak August-October period with nary a scratch. However, once it finally moved from near-vertical to vertical, down it went and has yet to recover.

These periods of vertical incline can be compared to the old Comex saw mentions "when they're yellin'" — i.e., periods when panic buying grips markets, forcing the FOMO-afflicted traders to buy at any price. In contrast, declining trendlines that are gradual in nature are consistent with bear market periods, but Meier Rothschild identified that the panic selling period of the decline is when the decline moves into the vertical phase, characterized by "blood in the streets" and few sellers left.

Silver

I am a Twitter follower, and as much as I detest the garbage that is strewn by way of political nonsense from the U.S. President or Twitter's current owner, I use it as a barometer of sentiment for all things financial. In addition to reading more than a few publications every day and dozens every week, I love it when a common thread dominates the Twitterverse.

Back in early October, I bit my lip as the Bitcoin Brotherhood was getting increasingly out of sorts with the outsized move in gold. Just as Bitcoin was gathering momentum to hit its record high of $126,110, they were extolling gold holders to "Switch to Bitcoin" in a manner that reeked of desperation, orchestration, and collusion. What followed was purely textbook action. Bitcoin topped shortly thereafter and is now in full bear market territory.

During the past two weeks, the world has seen a rocket ship advance in silver, and while I am a precious metal bull over a long-term perspective, I get somewhat animated when the same armchair technicians and or book-talkers like everyone on the You-Tube interview circuit are all singing in harmony of "200 silver!" or "LME shortage!"

The best is Eric Sprott, now taking well-earned victory laps around the arena because his "call" for new highs in silver finally paid off. That only applies, of course, if you did not take his advice the last time silver hit $50 when he told the audience at PDAC in 2011 that he was "All IN." However, since Eric is a billionaire and I am not, his opinion should be viewed seriously and mine, well, not so much. . .

Silver is, as represented by the ETF SLV:US, hitting new highs and is now overbought by a small margin, but what I see is fading momentum as seen with the money flow indicator hitting lower highs, as RSI registers lower highs, and the MACD indicator remains overbought.

Every tweet and email, every phone call and text message, everything I read and hear is now 100% SILVER, so I can only conclude that the same Game-stoppers and crypto-whackos that think they can run markets to perpetuity are now in full regalia in the silver market, just like NVidia in late October at $212 (now $182) and just like Bitcoin in early October at $126,000 (now $89,319).

I see SLV:US back at the 100-dma at $40.94 in due course, so I decided to buy the ProShares UltraShort Silver 2X's (ARCA) ETF (ZSL:US) with a view to profiting from the inevitable exit from the mania currently gripping silver. I fully recognize the 271 reasons that silver is going to $500 per ounce, but I choose quite selectively to absolutely ignore them.

Those reasons are already known to all and are fully discounted by the record silver price. Lastly, I get bombarded with investment "stories" on a daily basis and have developed an instinctive "divining rod" of sorts that allows me to detect subtle shifts in speculator sentiment based upon the number of similar "deals" that cross my desk. As an example, in September, I must have had two dozen junior gold stories hit the screen, with most of them being low-grade garbage that only now is getting skated onside by the rising gold price.

The same thing happened in late 2022 with lithium deals and in late 2024 with uranium. During those periods, my desk was bombarded with juniors claiming to be "the next Albemarle!" or "the next NexGen," if only my subscribers would write a cheque to allow it all to happen. Of course, there were some that caught my interest, but the vast majority did not, and that is exactly the case here in late 2025 with silver deals.

At or near tops, usually after an extended run in the already-established producer-developers, the junior silver deals have started to dominate my inbox. Silver in Nunavut, silver in Finland, silver in Nevada, silver in your cornflakes — silver deals are the talk of the town everywhere, as the favored narrative for those kiddies new to the world of silver is "shortage."

I take great exception to that word for a number of reasons. Firstly, the primary silver supply is largely determined by demand for other metals, not by silver prices alone. Mine production is expected to reach a 7-year high in 2025, rising by 2% to 844 million ounces, with increased output anticipated from both existing and new operations in several markets. Rising global production does not adequately describe "shortage" conditions. However, when a global mania driven by FOMO and YOLO increases demand exponentially in the same manner that the kiddies created outsized demand for bankrupt video game renters like GameStop, price action suddenly dictates the terms of the narrative so necessary in explaining the advance. Millions of Chinese and Indian investors piling into the silver trade is not due to the shortage of silver but rather the illusion of a shortage in silver. Narrative controls price.

I contend that the silver market is being controlled by not a supply problem (because the facts refute the allegation that there is a shortage of supply) but as in any product or service, prices always respond to sudden and sharp increases in demand, We saw similar increases in 1979-1980 and in 2011 when the rate of increase in the supply of silver remained constant but where unprecedented speculative interest overpowered existing supply resulting in $50 silver on both occasions.

Now, I own a couple of junior silver deals because they are exploration plays run by established winners, but I am not buying them because there is a pending "SilverSqueeze" just around the corner that will take granny's cutlery to over $400 per ounce. I sense that the silver narrative is beginning to fade, and am willing to speculate that it and gold will experience an extended period of correction in 2026 as the hot money cashes out and gravitates to the real shortage-driven metal of the century — copper — which does have a serious supply shortfall heading rapidly in the direction of escalating electrical demand and copper usage. When boring old copper starts to get squeezed, it affects every facet of life on our planet, not just the neck, finger, or wrist of a lucky lady or that ugly solar panel despoiling the view of the landscape.

Could I be wrong? Of course, I could be wrong. Evidence of imbecilic deduction will be acknowledged in this publication on a 2-day close in February gold above $4,433 and the HUI:US above 693.10 with silver moving to continued new highs. A close below $48 in the SLV:US, accompanied by a close below 617.72 in the HUI:US, and a close below $4,110 in February gold, and I will have a confirmed top on an intermediate-term basis only.

I will then be looking to re-enter all liquidated holdings from October 13th to 20th.

(Note: All snarky emails to the contrary will be summarily ignored.)

Juniors

There were to major releases last week by my two favourite junior companies — Getchell Gold Corp. (GTCH:CSE; GGLDF:OTCQB) and Fitzroy Minerals Inc. (FTZ:TSX.V; FTZFF:OTCQB), and while the former announced a high-grade intercept that may have altered the landscape for their Fondaway Canyon project in Nevada (19.0 meters of 5.7 g/t Au), the latter was not able to report high-grade assays from either of their two flagship projects in Chile. However, while the former had a nice "up" week, closing at CA$0.40, the latter had a down week as investors focused on lower-grade results from Buen Retiro and Caballos while missing the most critical development in the history of the company.

For the past 18 months, I have patiently awaited the completion of Fitzroy Minerals' exploration of the copper-bearing oxide cap that can be moved to production by way of heap-leach technology for a minimal CAPEX downstroke, which can also be permitted and built quickly. I appreciate the tenacity with which Fitzroy management systematically grid-drilled the oxide zone to the point where they have entered the early stage of Preliminary Economic Assessment. However, as lovely as will be the free cash flow spewing out of Buen Retiro, it will not force a major mining company to write a big fat cheque to ingest the 330 million shares issued which is what will be required to make any kind of decent return.

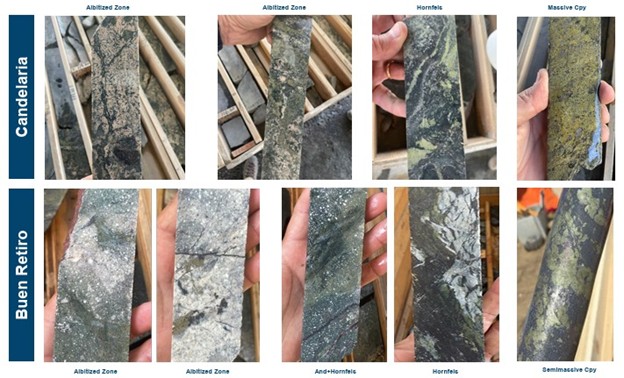

What will force them to write a big, fat cheque is a "Candelaria-style" discovery of iron-oxide-copper-gold mineralization on the scale found 45km. to the northeast at Lundin Mining's Candelaria Mine Complex, where forward guidance for 2025 has copper production pegged at 143,000-149,000 tonnes and 78,000-84,000 ounces of gold.

From the press release on Tuesday, "Hole 43, 150 metres north of hole 42, is currently underway. Crucially, the core photographs look very similar to the style of mineralization from within the resource zone at Candelaria. These holes are the first time that Fitzroy has seen consistent sulphide mineralization of this nature, which further enhances the exploration model at this project."

This was singularly the most important part of the press release, and investors sold the stock down from $0.40 to $0.32 without the slightest consideration of the implications of the statement.

The company released a video that explains in detail what they are dealing with here, in what may be a geological occurrence of immense proportions.

Needless to say, the company posted this comparison of core samples taken from recent deep drill holes at Buen Retiro compared to core found at the Candelaria Mine Complex.

Everyone in my universe who owns shares in FTZ/FTZFF is now on the edge of their seats, awaiting assays from hole # BRT-DDH-043 when it returns from analysis within the next few weeks.

Fitzroy is my premier copper proxy for 2025, while Getchell enjoys the same distinction as my gold proxy.

Those readers wishing to offer me suggestions on why my call on silver is so terribly misguided, uninformed, and just plain outright wrong can email me at [email protected], and I shall be delighted to respond in early 2026 if time permits.

| Want to be the first to know about interesting Gold, Silver and Copper investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers, contractors, shareholders, and/or employees of Streetwise Reports LLC (including members of their household) own securities of Getchell Gold Corp. and Fitzroy Minerals Inc.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: Getchell Gold Corp. and Fitzroy Minerals Inc. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.