About a month ago Paul van Eeden (www.paulvaneeden.com) published his updated gold model. At the time, gold was trading at approximately $970 and most of the “experts” and pundits were claiming gold was beginning the next up-phase of its big bull run. Paul’s exhaustive analysis of the data, however, suggested the 2008 price should be closer to $776 per ounce. Well in case you haven’t noticed, gold closed at $786: man, is that guy charmed or what! I remain dubious and still hiding in my bunker.

Mentally, however, I am preparing to timidly step back into the gold market if it stabilizes around the current price. Assuming it does, this gold price (or silver and base metals for that matter) provides no impetus for the junior exploration stocks to move higher. There has been serious technical damage to the stock charts which is another way of saying there are a lot of people underwater and anxious to get out on any uptick. I therefore continue to believe sellers will swamp buyers in all but a few select names through the end of the year at least. If so, there will be some very compelling bargains to be had. I am keeping my powder dry.

I recently received a rather detailed and insightful query from a subscriber regarding the relative valuations of several “prospect generators”. This week’s letter addresses some of his questions with a brief discussion of mining and exploration business models. This is followed by a table with some of the more pertinent data for 10 prospect generators. Be forewarned-despite the apparent value in this group I am not adding any new names to the EI portfolio. I urge you however to arrive at your own investment decision regarding names within this group.

The Contrary Investors Café interviewed me a few weeks ago. This is an interesting investment site, have a look around. You can listen to our discussion here.

The Rant

Exploration is primarily a game of odds with luck at the end of a drill bit being the great unknown. I have discussed the very poor odds of discovering an economic mineral deposit numerous times in this esteemed publication. The fact that gold used to sell for over $900 an ounce and people can make money on rock containing 0.03 of an ounce per ton should tell you this stuff is hard to come by.

Nonetheless, there are literally thousands of junior exploration companies listed on the Canadian and Australian stock exchanges that are combing the world looking for gold, copper, silver, uranium, etc. Last year alone over $11 billion was spent searching for metals (Metals Economic Group data) yet you would be hard pressed to point to a dozen legitimate significant discoveries in the past five years. For the rare company that is successful, however, the rewards can be fantastic. That is why this letter takes an interest in the junior exploration sector.

How these junior companies go about their business directly affects how extraordinary our rewards or losses can be. There are three basic business models the junior explorers employ in their efforts to succeed.

1. Acquire a known deposit and work to improve its economics.

2. Continually raise money and hope like hell the next drill hole is the big discovery you have been looking for.

3. Bring in a partner to fund the heavy expenditures required to make the big discovery.

Model # 1 above works for a very select group of people who have the skill and financial connections to successfully pull it off. Hunter Dickinson and The Lundin Group are good examples of companies successfully employing this model. There are, however, many other companies that try to bootstrap themselves into a positive, free cash flow position by developing small mines. From my experience this rarely works.

Mining is a very tough and complex business in which misjudgments, delays, cost increases and metal price changes are inevitable. A large, well funded mine can normally endure these problems. A small marginal operation will go bankrupt. Although there are many notable exceptions to this rule (First Quantum, FNX Mining and Novagold) there are hundreds more small, broken mines and worthless stock certificates scattered around the lonely deserts and urban jungles of the world.

On the rare occasion that we here at EI invest in these situations the production costs have to fall within the lower third of the industry costs, and/or the net present value must be significantly higher than the current company market capitalization. We don’t do small marginal deposits!!

Model # 2 above is the preferred model for the majority of junior explorers and speculators. It gives you 100% of the upside associated with any discovery and produces huge capital gains for anyone fortunate enough to have been a shareholder. Recent examples include Aurelian Resources and Canplats Minerals. They ran from $0.65 to $30 (pre-split) and $0.20 to $5.00, respectively. On the other hand, the downside unfortunately is nearly 100%.

This “go for broke” junior exploration model requires continual financing and can work when the market is all whipped up, money is cheap and even turkeys can raise capital. However, the resulting shareholder dilution to fund the next big play means your share of any future discovery is diminished with each property drilled and gone bust.

Let’s play with the numbers and assume you are able to do a bit of research and avoid the outright frauds. This generously puts the chance of a discovery at, say, 1 in 100. That being the case, statistically you would need to fund 100 drill programs for that single legitimate discovery. Put another way, assuming that you “invest” $10,000 in 100 drill-hole plays or companies you would need a 100-bagger to get your money back. A single 10-bagger means you only lost 90% of your one million dollars. There are of course other ways to make money in these companies. Often just the perception of a discovery and market sentiment can work for you but the actual odds of making money betting on the drill bit over the long run are really not good at all.

I feel that we here at EI are able to improve the odds of drill-hole success through careful research, years of experience, site visits and global contacts in the industry. That is why the portfolio is populated by a small number of high-risk exploration plays and developing discoveries. I do not believe in the shotgun approach and do not stay married to any company if the facts change. When the grounds for owning a stock shifts from conviction to hope, it’s time to exit that stock. There are no guarantees attached to the EI portfolio and I stress anyone playing in this market should be doing so with risk capital only.

Model #3 refers to companies that joint venture their projects to partners who will then spend the big dollars needed to test the exploration targets. In doing so, shareholders' eventual ownership of a bona fide discovery is diluted but their ownership in the generating company is not. This dilution at the property level versus the corporate share structure level is not popular among most junior resource market investors. The majority of gamblers in the junior sector tend to believe that the company is giving away their shot at a 10-bagger.

The prospect generator companies, and most of the people who invest in them, tend to view their company as a long-term business venture. The management behind these companies has probably learned the hard way that despite their eternal optimism, the earth rarely deposits economic quantities of metal in one place. They recognize that actually discovering an economic mineral deposit requires considerable time (years) and money ($10’s to $100’s of millions). Hence, it takes a lot of looking and drilling to find the unique set of circumstances responsible for an economic mineral deposit.

Let’s look at some numbers again. The typical joint venture requires the incoming partner to spend X dollars over a period of time to earn a piece of the property. Ideally the partner upgrades the property to or through the feasibility stage for a 60% to 80% interest if a resource is defined. The prospect generator is thereafter required to fund their portion (call it 30%) of the development costs or dilute their interest. This roughly 30% of a defined resource and possible 10-bagger discovery has cost investors relatively little in terms of share dilution. The same holds true if nothing of value is defined.

More importantly, the investor in a generator is ultimately exposed to more chances of a success for the same investment dollar. This is because the prospect generator continually brings in new partners to drill-test targets. Often the same old targets get worked over and over again but with a new twist. Almaden Minerals’ Caballo Blanco project has seen at least four companies drill it and walk away yet each time the property became more valuable. Discoveries are usually made through a series of trials and errors where the knowledge base improves with each drill program.

Another advantage, often pointed out by Paul van Eeden and Rick Rule, is that you get the added value of a third party geologist critically doing due diligence on your generator’s properties for you. This comes at no extra cost and provides some assurance that the company is not wasting your money.

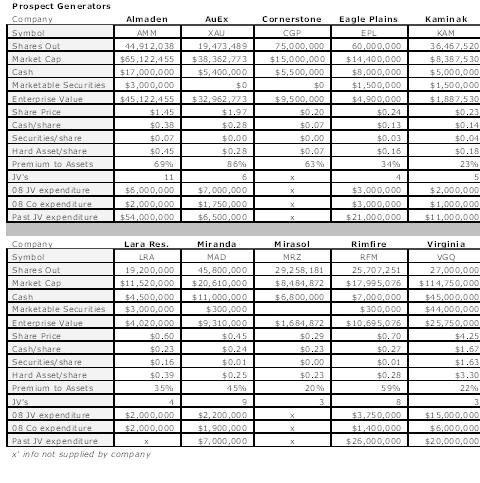

The following table illustrates the advantage of having partners spend the money. Companies like Eagle Plains, Kaminak and Rimfire have had their current market capitalization, or more, spent by partners on their projects without a discovery. That’s money raised and lost by someone else with absolutely no dilution to the generator’s shareholders. The generator’s business and corporate structure remain intact despite the lack of obvious success.

This is a rather messy table but I think all the information is germane. It is provided to help you evaluate these companies and make an investment decision. The data was compiled by my daughter from information supplied by and/or checked by the respective companies (she graduates university next year and will most definitely be looking for work!)

Some of the more useful value metrics include cash, enterprise value, premium to assets, and past and current joint venture expenditures. Mineral property assessments are obviously missing from this database. Simply put, there is not enough time to cover and discuss each of the company’s projects. I am watching them and will do my best to bring any potentially significant discovery to your attention when it happens.

Cash is obviously very important, particularly in a market where cash is going to be very hard to come by. Although we were unable to get annual company burn rates, the 2008 expenditure estimates will provide some indication of how long the company can survive without raising more money. In this category AMM, XAU, EPL, MAD, RFM and VGQ are set to remain in business for years.

Enterprise value is essentially the value being placed on the company by the market for the company’s management, properties and future prospects. It is the market capitalization less cash and marketable securities. [Note that VGQ’s $44 million in marketable securities is actually a straight net asset valuation of their 2.2% royalty on the Elenore deposit they sold to Goldcorp. The valuation is based on 2.5 million ounces and an $800 gold price.]

The spread in enterprise values is quite large, ranging from about $45 million for AMM to a minuscule $1.8 million for KAM. Almaden’s relatively high valuation is partly due to the shareholder loyalty they have built through their persistence since 1986. They have never had a share rollback and have proven themselves a very reliable company that continually generates new mineral targets. They currently have a partner drilling the high profile Caballo Blanco gold system in Mexico and another 10 projects being worked by partners.

XAU’s relatively high enterprise valuation is mostly due to a gold discovery in Nevada being drilled out by Fronteer Resources. MAD’s $7 million enterprise value reflects the size of the prize they are after. They are targeting Cortez Hills-style gold deposit in Nevada (8.5 million ounces).

KAM, EPL, LRA, MAD and MRZ look very cheap based on the enterprise value metric. The premium to assets line shows as a percentage how much the company is trading above its enterprise value.

The current and past joint venture lines provide a good measure of how successful the companies actually are at their generator business. From my experience all of these companies are good at the business. The variability in past expenditure reflects how long they have been in business or heavy expenditure on one project that looked particularly promising.

I personally own most of these companies and nearly every week I am tempted to add the “prospect generators” to the EI portfolio. These are some of the best and most honest explorers in the business. I think they offer very good value here depending on what factor you consider most important. However, I am focused on keeping the portfolio holdings to a minimum for now as I believe there will be even better deals as this market continues its downward spiral.

That’s the way I see it,

Brent Cook

Exploration Insights offers the sophisticated speculator independent and unbiased information analysis on the junior mining and exploration market. It is written and produced on a weekly basis by Brent Cook, a veteran geologist and mining stock analyst. To learn more about subscribing to Exploration Insights visit our web site here https://www.explorationinsights.com/

Testimonials

Rick Rule Global Resource Investments, Founder

http://www.gril.net/default.htm

“Serious mineral exploration speculators should “employ” Brent Cook. I’m supposed to be smart, and I paid him hundreds of thousands of dollars when he worked for me; you can get him for $140 per month! I got good value- imagine your potential returns. Brent is a no nonsense “boots on the ground” geo, not one of the “desk explorers” who cost the investment community so many millions. He can make you serious money with his buy recommendations, and save you much more, by counseling you on what to avoid. Most newsletters are written by journalists, if they researched publishing investments, maybe they would be credible. Brent is an exploration geologist, writing about exploration geology, what a wonderful, novel idea. Do your portfolio a favor, subscribe!”

Robert Bishop Editor, Gold Mining, Stock Report (1983-2007)

“Minerals exploration is a game of long odds and Brent Cook never lets his readers forget that. After years of visiting mining projects with Brent, and liberally picking his brain when not in the field, I have gained the utmost respect for Brent’s views on rocks. Market psychology, promotion, capital structure, people, and many other factors dictate whether a stock will rise or fall, but in the final analysis, the rocks always prevail. Brent Cook knows rocks.”

Disclaimer:

This letter/article is not intended to meet your specific individual investment needs and it is not tailored to your personal financial situation. Nothing contained herein constitutes, is intended, or deemed to be -- either implied or otherwise -- investment advice. This letter/article reflects the personal views and opinions of Brent Cook and that is all it purports to be. While the information herein is believed to be accurate and reliable it is not guaranteed or implied to be so. The information herein may not be complete or correct; it is provided in good faith but without any legal responsibility or obligation to provide future updates. Research that was commissioned and paid for by private, institutional clients is deemed to be outside the scope of the newsletter and certain companies that may be discussed in the newsletter could have been the subject of such private research projects done on behalf of private institutional clients. Neither Brent Cook, nor anyone else, accepts any responsibility, or assumes any liability, whatsoever, for any direct, indirect or consequential loss arising from the use of the information in this letter/article. The information contained herein is subject to change without notice, may become outdated and may not be updated. The opinions are both time and market sensitive. Brent Cook, entities that he controls, family, friends, employees, associates, and others may have positions in securities mentioned, or discussed, in this letter/article. While every attempt is made to avoid conflicts of interest, such conflicts do arise from time to time. Whenever a conflict of interest arises, every attempt is made to resolve such conflict in the best possible interest of all parties, but you should not assume that your interest would be placed ahead of anyone else's interest in the event of a conflict of interest. No part of this letter/article may be reproduced, copied, emailed, faxed, or distributed (in any form) without the express written permission of Brent Cook. Everything contained herein is subject to international copyright protection.

Mentally, however, I am preparing to timidly step back into the gold market if it stabilizes around the current price. Assuming it does, this gold price (or silver and base metals for that matter) provides no impetus for the junior exploration stocks to move higher. There has been serious technical damage to the stock charts which is another way of saying there are a lot of people underwater and anxious to get out on any uptick. I therefore continue to believe sellers will swamp buyers in all but a few select names through the end of the year at least. If so, there will be some very compelling bargains to be had. I am keeping my powder dry.

I recently received a rather detailed and insightful query from a subscriber regarding the relative valuations of several “prospect generators”. This week’s letter addresses some of his questions with a brief discussion of mining and exploration business models. This is followed by a table with some of the more pertinent data for 10 prospect generators. Be forewarned-despite the apparent value in this group I am not adding any new names to the EI portfolio. I urge you however to arrive at your own investment decision regarding names within this group.

The Contrary Investors Café interviewed me a few weeks ago. This is an interesting investment site, have a look around. You can listen to our discussion here.

The Rant

Exploration is primarily a game of odds with luck at the end of a drill bit being the great unknown. I have discussed the very poor odds of discovering an economic mineral deposit numerous times in this esteemed publication. The fact that gold used to sell for over $900 an ounce and people can make money on rock containing 0.03 of an ounce per ton should tell you this stuff is hard to come by.

Nonetheless, there are literally thousands of junior exploration companies listed on the Canadian and Australian stock exchanges that are combing the world looking for gold, copper, silver, uranium, etc. Last year alone over $11 billion was spent searching for metals (Metals Economic Group data) yet you would be hard pressed to point to a dozen legitimate significant discoveries in the past five years. For the rare company that is successful, however, the rewards can be fantastic. That is why this letter takes an interest in the junior exploration sector.

How these junior companies go about their business directly affects how extraordinary our rewards or losses can be. There are three basic business models the junior explorers employ in their efforts to succeed.

1. Acquire a known deposit and work to improve its economics.

2. Continually raise money and hope like hell the next drill hole is the big discovery you have been looking for.

3. Bring in a partner to fund the heavy expenditures required to make the big discovery.

Model # 1 above works for a very select group of people who have the skill and financial connections to successfully pull it off. Hunter Dickinson and The Lundin Group are good examples of companies successfully employing this model. There are, however, many other companies that try to bootstrap themselves into a positive, free cash flow position by developing small mines. From my experience this rarely works.

Mining is a very tough and complex business in which misjudgments, delays, cost increases and metal price changes are inevitable. A large, well funded mine can normally endure these problems. A small marginal operation will go bankrupt. Although there are many notable exceptions to this rule (First Quantum, FNX Mining and Novagold) there are hundreds more small, broken mines and worthless stock certificates scattered around the lonely deserts and urban jungles of the world.

On the rare occasion that we here at EI invest in these situations the production costs have to fall within the lower third of the industry costs, and/or the net present value must be significantly higher than the current company market capitalization. We don’t do small marginal deposits!!

Model # 2 above is the preferred model for the majority of junior explorers and speculators. It gives you 100% of the upside associated with any discovery and produces huge capital gains for anyone fortunate enough to have been a shareholder. Recent examples include Aurelian Resources and Canplats Minerals. They ran from $0.65 to $30 (pre-split) and $0.20 to $5.00, respectively. On the other hand, the downside unfortunately is nearly 100%.

This “go for broke” junior exploration model requires continual financing and can work when the market is all whipped up, money is cheap and even turkeys can raise capital. However, the resulting shareholder dilution to fund the next big play means your share of any future discovery is diminished with each property drilled and gone bust.

Let’s play with the numbers and assume you are able to do a bit of research and avoid the outright frauds. This generously puts the chance of a discovery at, say, 1 in 100. That being the case, statistically you would need to fund 100 drill programs for that single legitimate discovery. Put another way, assuming that you “invest” $10,000 in 100 drill-hole plays or companies you would need a 100-bagger to get your money back. A single 10-bagger means you only lost 90% of your one million dollars. There are of course other ways to make money in these companies. Often just the perception of a discovery and market sentiment can work for you but the actual odds of making money betting on the drill bit over the long run are really not good at all.

I feel that we here at EI are able to improve the odds of drill-hole success through careful research, years of experience, site visits and global contacts in the industry. That is why the portfolio is populated by a small number of high-risk exploration plays and developing discoveries. I do not believe in the shotgun approach and do not stay married to any company if the facts change. When the grounds for owning a stock shifts from conviction to hope, it’s time to exit that stock. There are no guarantees attached to the EI portfolio and I stress anyone playing in this market should be doing so with risk capital only.

Model #3 refers to companies that joint venture their projects to partners who will then spend the big dollars needed to test the exploration targets. In doing so, shareholders' eventual ownership of a bona fide discovery is diluted but their ownership in the generating company is not. This dilution at the property level versus the corporate share structure level is not popular among most junior resource market investors. The majority of gamblers in the junior sector tend to believe that the company is giving away their shot at a 10-bagger.

The prospect generator companies, and most of the people who invest in them, tend to view their company as a long-term business venture. The management behind these companies has probably learned the hard way that despite their eternal optimism, the earth rarely deposits economic quantities of metal in one place. They recognize that actually discovering an economic mineral deposit requires considerable time (years) and money ($10’s to $100’s of millions). Hence, it takes a lot of looking and drilling to find the unique set of circumstances responsible for an economic mineral deposit.

Let’s look at some numbers again. The typical joint venture requires the incoming partner to spend X dollars over a period of time to earn a piece of the property. Ideally the partner upgrades the property to or through the feasibility stage for a 60% to 80% interest if a resource is defined. The prospect generator is thereafter required to fund their portion (call it 30%) of the development costs or dilute their interest. This roughly 30% of a defined resource and possible 10-bagger discovery has cost investors relatively little in terms of share dilution. The same holds true if nothing of value is defined.

More importantly, the investor in a generator is ultimately exposed to more chances of a success for the same investment dollar. This is because the prospect generator continually brings in new partners to drill-test targets. Often the same old targets get worked over and over again but with a new twist. Almaden Minerals’ Caballo Blanco project has seen at least four companies drill it and walk away yet each time the property became more valuable. Discoveries are usually made through a series of trials and errors where the knowledge base improves with each drill program.

Another advantage, often pointed out by Paul van Eeden and Rick Rule, is that you get the added value of a third party geologist critically doing due diligence on your generator’s properties for you. This comes at no extra cost and provides some assurance that the company is not wasting your money.

The following table illustrates the advantage of having partners spend the money. Companies like Eagle Plains, Kaminak and Rimfire have had their current market capitalization, or more, spent by partners on their projects without a discovery. That’s money raised and lost by someone else with absolutely no dilution to the generator’s shareholders. The generator’s business and corporate structure remain intact despite the lack of obvious success.

This is a rather messy table but I think all the information is germane. It is provided to help you evaluate these companies and make an investment decision. The data was compiled by my daughter from information supplied by and/or checked by the respective companies (she graduates university next year and will most definitely be looking for work!)

Some of the more useful value metrics include cash, enterprise value, premium to assets, and past and current joint venture expenditures. Mineral property assessments are obviously missing from this database. Simply put, there is not enough time to cover and discuss each of the company’s projects. I am watching them and will do my best to bring any potentially significant discovery to your attention when it happens.

Cash is obviously very important, particularly in a market where cash is going to be very hard to come by. Although we were unable to get annual company burn rates, the 2008 expenditure estimates will provide some indication of how long the company can survive without raising more money. In this category AMM, XAU, EPL, MAD, RFM and VGQ are set to remain in business for years.

Enterprise value is essentially the value being placed on the company by the market for the company’s management, properties and future prospects. It is the market capitalization less cash and marketable securities. [Note that VGQ’s $44 million in marketable securities is actually a straight net asset valuation of their 2.2% royalty on the Elenore deposit they sold to Goldcorp. The valuation is based on 2.5 million ounces and an $800 gold price.]

The spread in enterprise values is quite large, ranging from about $45 million for AMM to a minuscule $1.8 million for KAM. Almaden’s relatively high valuation is partly due to the shareholder loyalty they have built through their persistence since 1986. They have never had a share rollback and have proven themselves a very reliable company that continually generates new mineral targets. They currently have a partner drilling the high profile Caballo Blanco gold system in Mexico and another 10 projects being worked by partners.

XAU’s relatively high enterprise valuation is mostly due to a gold discovery in Nevada being drilled out by Fronteer Resources. MAD’s $7 million enterprise value reflects the size of the prize they are after. They are targeting Cortez Hills-style gold deposit in Nevada (8.5 million ounces).

KAM, EPL, LRA, MAD and MRZ look very cheap based on the enterprise value metric. The premium to assets line shows as a percentage how much the company is trading above its enterprise value.

The current and past joint venture lines provide a good measure of how successful the companies actually are at their generator business. From my experience all of these companies are good at the business. The variability in past expenditure reflects how long they have been in business or heavy expenditure on one project that looked particularly promising.

I personally own most of these companies and nearly every week I am tempted to add the “prospect generators” to the EI portfolio. These are some of the best and most honest explorers in the business. I think they offer very good value here depending on what factor you consider most important. However, I am focused on keeping the portfolio holdings to a minimum for now as I believe there will be even better deals as this market continues its downward spiral.

That’s the way I see it,

Brent Cook

Exploration Insights offers the sophisticated speculator independent and unbiased information analysis on the junior mining and exploration market. It is written and produced on a weekly basis by Brent Cook, a veteran geologist and mining stock analyst. To learn more about subscribing to Exploration Insights visit our web site here https://www.explorationinsights.com/

Testimonials

Rick Rule Global Resource Investments, Founder

http://www.gril.net/default.htm

“Serious mineral exploration speculators should “employ” Brent Cook. I’m supposed to be smart, and I paid him hundreds of thousands of dollars when he worked for me; you can get him for $140 per month! I got good value- imagine your potential returns. Brent is a no nonsense “boots on the ground” geo, not one of the “desk explorers” who cost the investment community so many millions. He can make you serious money with his buy recommendations, and save you much more, by counseling you on what to avoid. Most newsletters are written by journalists, if they researched publishing investments, maybe they would be credible. Brent is an exploration geologist, writing about exploration geology, what a wonderful, novel idea. Do your portfolio a favor, subscribe!”

Robert Bishop Editor, Gold Mining, Stock Report (1983-2007)

“Minerals exploration is a game of long odds and Brent Cook never lets his readers forget that. After years of visiting mining projects with Brent, and liberally picking his brain when not in the field, I have gained the utmost respect for Brent’s views on rocks. Market psychology, promotion, capital structure, people, and many other factors dictate whether a stock will rise or fall, but in the final analysis, the rocks always prevail. Brent Cook knows rocks.”

Disclaimer:

This letter/article is not intended to meet your specific individual investment needs and it is not tailored to your personal financial situation. Nothing contained herein constitutes, is intended, or deemed to be -- either implied or otherwise -- investment advice. This letter/article reflects the personal views and opinions of Brent Cook and that is all it purports to be. While the information herein is believed to be accurate and reliable it is not guaranteed or implied to be so. The information herein may not be complete or correct; it is provided in good faith but without any legal responsibility or obligation to provide future updates. Research that was commissioned and paid for by private, institutional clients is deemed to be outside the scope of the newsletter and certain companies that may be discussed in the newsletter could have been the subject of such private research projects done on behalf of private institutional clients. Neither Brent Cook, nor anyone else, accepts any responsibility, or assumes any liability, whatsoever, for any direct, indirect or consequential loss arising from the use of the information in this letter/article. The information contained herein is subject to change without notice, may become outdated and may not be updated. The opinions are both time and market sensitive. Brent Cook, entities that he controls, family, friends, employees, associates, and others may have positions in securities mentioned, or discussed, in this letter/article. While every attempt is made to avoid conflicts of interest, such conflicts do arise from time to time. Whenever a conflict of interest arises, every attempt is made to resolve such conflict in the best possible interest of all parties, but you should not assume that your interest would be placed ahead of anyone else's interest in the event of a conflict of interest. No part of this letter/article may be reproduced, copied, emailed, faxed, or distributed (in any form) without the express written permission of Brent Cook. Everything contained herein is subject to international copyright protection.