Having just returned from boating in northern Georgian Bay and an area called The North Channel, I have been by and large out of contact with gold and silver prices since July 22 and am delighted to see that prices have stabilized after dipping in late Spring to under $1,210. Over the past month, the global stock markets have all danced around all-time highs with Dr. Copper forging a break-out above the $2.90 level, marking the highest close in two years. Amazon CEO Jeff Bezos briefly became the richest man in the world as his stock traded up over $1,080 per share and Twitter closed a couple of dollars off the 52-week lows and over $9 below its IPO price of $26. And yet, despite all of this, the CNBC bubbleheads continue to spew out complete nonsense as to why they remain "positive" on the outlook for equities. The name of the game in asset management is the fee structure and if you suddenly get "cautious" as opposed to "positive," investors yank their money out and the wealth advisors take a serious pay cut. And we KNOW how Wall Street feels about pay cuts. . .

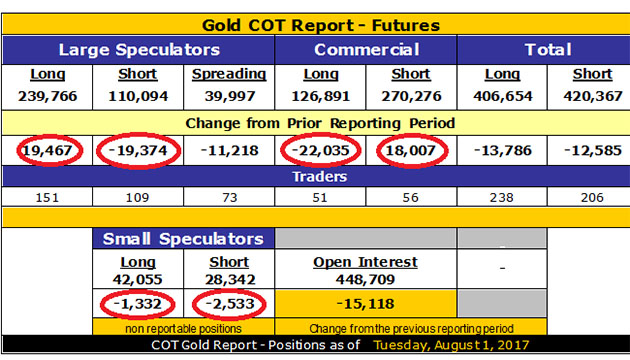

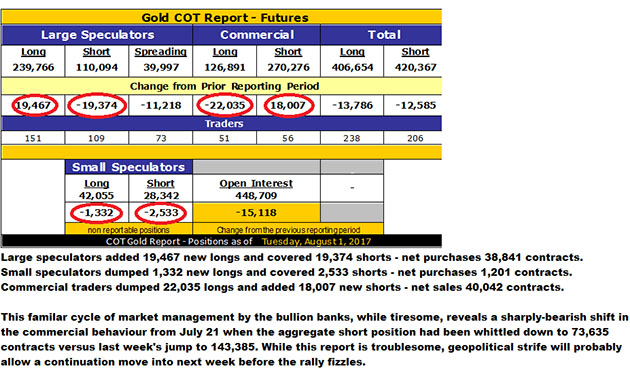

Of note this week is the sharp increase in Commercial shorts revealed in the August 1, 2017 COT whereby the bullion bank criminals fed 69,750 contracts representing 6,975,000 ounces of gold with a notional value of around $8.9 billion of phony, synthetic "gold" into the market during the two-week period that began on July 21. While I was moored in breathtaking fjords in northern Georgian Bay, swimming next to snapping turtles with shells two-feet in diameter, I was unaware that reptiles of a similar disposition were snapping up shorts at an alarming rate. We have seen this epic movie before; we will see it again; and we know that it will end with the Large Specs covering shorts and ramping up their net longs at the top of the rally while the bankers feed out fictitious "supply" before the inevitable reversal that punctuates the advance with felonious certainty.

COT Report August 1

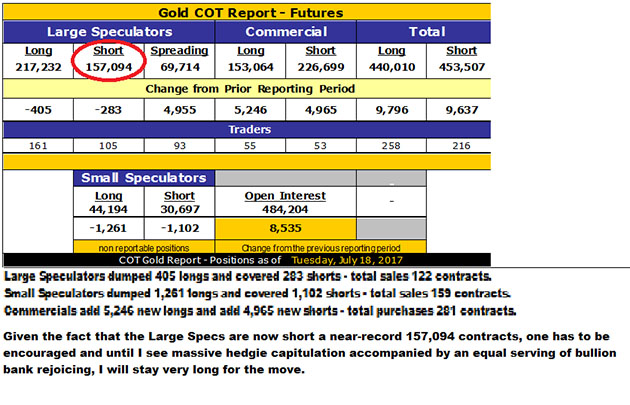

Shown below is the COT from July 18 so that we may all observe how nauseatingly predictable this exercise has become. The large specs represent investors by way of either mutual or hedge funds and in many cases pension funds that use technical analysis as a trading tool. My beef with the system is that the bullion banks can act under the guise of "client hedging" (producer hedging) while in most cases taking equal (or larger) proprietary positions for the house account. Since they are not actually hedging anything other than their end-of-quarter bonuses, they are still allowed to sell an infinite number of notional product without proof of ownership. It is the ultimate rigged casino because they know precisely when they will strike and how big the move is going to be because they CREATE the move itself. And that, my friends, is market manipulation—period.

COT Report July 18

My outlook for gold was "bang-the-table-bullish" three weeks ago at $1,230 based on the COT data and I opened a position in the JNUG (Triple-leveraged GDXJ ETF) and the USLV (Triple Leverage Silver) while convincing myself to ignore the stops while out of internet range in Northern Ontario. As a result, I find myself in the rare position of being correct on precious metals prices and wrong on gold miner prices. We have rallied over $80 per ounce of the lows of early July at around $1,210 and yet the HUI (NYSE Arca Gold BUGS Index) can't even manage to get above 200 whereas it hit 205 back on June 14 with gold at these levels taking the JNUG to $21.85 during the move. The dilemma I face now lies in the seasonality associated with the August-November period when the gold and silver stocks usually have a decent pop. However, the Commercials are setting me up for a colonoscopy in the face of positive seasonal patterns and that makes it difficult to gauge the target price for the JNUG looking out to November. I am probably going to defer additions to JNUG and USLV until after Labor Day but remain long the unleveraged positions until we get some clarity.

Stock prices for the major averages have been on a tear lately—well, they have been on a "tear" since April 2009 when the global central banks decided to act as a collective placing a floor on volatility and an arm lock on prices. Last November 8 at approximately 10:30 in the evening, the Dow Jones was down a whopping 1,000 points on the eve of the Trump victory. Being long a number of S&P put options and a goodly position in the UVXY, I went to bed happy with visons of sugar plum profits dancing in my head for the next morning only to rise to the horror of that overnight reversal where the bankers decided to re-jig perceptions of a Trump victory.

The narrative changed from disaster to euphoria as stock prices began was has been an incredible show of strength ("interventions") in ignoring the near-farcical conditions in the White House. This has occurred week after week after week despite a raging battle between Trump and virtually anyone that defies him starting with the mainstream media to the point where the new "traders' perspectives" have become completely polarized. You now reside in either "The Bubble Will Live Forever" camp or the in "The Crash is Coming Tomorrow" camp with virtually no one in between.

Since I have long opined that "One can never underestimate the replacement power of equities within an inflationary spiral," I get perpetually shouted down because of the absence of any serious CPI or PPI increases. However, monetary inflation ("Printing" by the central bankers) has been ongoing since the financial crisis of 2007-2008, and that is what has propelled stocks. It certainly isn't productivity gains and it certainly isn't a manufacturing renaissance, and with the Amazon-Walmart slugfest for retail dominance, the major driver is multiple expansion brought about by excess liquidity so when the Fed's Janet Yellen talks about "normalizing the balance sheet," it is actually a signal that she is about to remove liquidity and that is BAD for stocks. The replacement value of stocks in a "quantitative tightening" ("QT") environment is diametrically opposite to where we have been since April 2009 when the S&P hit the 666 (Sign of the Beast) level, so depending how fast and furiously they decide to "normalize", stock prices are perched on a "permanently perilous ledge" as opposed to Irwin Fisher's famous "permanently high plateau" that preceded the 1929 Crash.

Moving along to the topic of the junior miners, I am delighted to see that my number one pick for 2017, Canuc Resources Corp. (CDA:TSX.V) recently hit a record high at $0.60 per share, largely on speculation surrounding the San Javier project. In the interest of full disclosure, I have assisted this company and participated in private placements for both CDA.V and the privateco (Santa Rosa Silver Mining Company) that was RTO'd into CDA earlier this year (which means I was compensated by CDA and Santa Rosa). The San Javier project was introduced to me in 2014 and after some careful consideration, I decided to do what it would take to keep it alive with the help of a number of key investors with financings at the equivalent price of $0.10 per CDA share with the final raise at $0.25 per share in March 2017.

This is my premier holding in both size and effort and is the direct result of an assessment made by current V.P. Exploration John Nebocat back in 2014. You will all recall that John was V.P. Exploration for Tinka Resources and was directly responsible for the Ayawilca zinc discovery that is now making the rounds of the newsletter, blogster and chatroom arenas. His favorable assessment in 2014 made me think that there was a big silver (and gold) resource to be established here and while assays have yet to be reported, I have never doubted for a moment that drilling was going to reveal some big and very impressive surprises. Because of the workings down to the 125 meter level, the 43-101 confirmed the presence of an average grade of 11.3 ounces per tonne of silver and 0.06 OPT gold, commanding an ore value per tonne of nearly U.S.$300 per tonne (at today's prices).

Since the project had never actually been drilled, I surmised that a resource estimate could quite easily be established at minimal cost and with maximal certainty. The upside surprise would be how far to depth this vein system extends and how many more veins are present. They are on the last of a five-hole program and are expected to report assays after Labor Day but judging from the action in the stock, it sure looks like speculators like what they either hear or see and are willing to place bets on the outcome. I have privately thought that an initial resource of 100 million silver-equivalent ounces was possible and that the valuation would be roughly $2 per ounce, so with 54.2 million shares issued (including all warrants and options) and assuming that they will issue another 10 million by year-end to further finance the project, a valuation would be slightly north of U.S.$3.00 per share. Now, the initial resource calculation is many months away but this first-ever set of drill results will serve to advance the needle and increase investor confidence in the likelihood that the San Javier project carries scale and grade, which in turn will attract the attention of the major silver miners all of whom are active and comfortable with the jurisdiction.

So, with the S&P off, the all-too-familiar month of August, being a harbinger of sorts, is threatening to do it again. I recall that in August of 1987 we had a fairly severe correction and one that preceded the 22.6% single-day drop seen in October of that year. It was a nightmarish event and one that evoked the usual macabre salvos of dark humor jokes like "How do you get your broker out of a tree? Answer: Cut the rope!" or "It's raining financial advisors today!" but all I remember was my beloved Fido clinging to the ceiling with embedded claws as I ranted and raved at my quote screen. The Fed and its lip service surrounding "balance sheet normalization" would be well-advised to heed the forebodings of the month of August because the mere mention of "QT" is nothing more than fanciful folly, if executed.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Michael Ballanger: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: A family member owns Stakeholder Gold. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: I am currently a consultant to CDA, SRC, and WUC by way of Bonaventure Explorations Limited. My company has a financial relationship with the following companies mentioned in this article: Bonaventure Explorations is 50% owned by me. It has in the past been paid consulting fees by CDA, SRC, TK, GI and WUC. I determined which companies would be included in this article based on my research and understanding of the sector.

2) The following companies mentioned in this article are sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Stakeholder Gold (and owned securities of Santa Rosa Silver Mining Co. prior to the RTO) companies mentioned in this article.

All charts courtesy of Michael Ballanger.