To regard the lengthy bull market in gold as an isolated fact would be simplistic and superficial. The media and most of the financial community are captivated by daily price action, but see nothing more. To most, it is a speculation, probably an overcrowded trade, and maybe a bubble. It is seen in the narrowest of terms, as an odd curiosity that will at some point just go away.

Gold's advance is but one aspect of a much bigger picture. The collapse of the dot com and housing bubbles, the 2008 credit collapse, the eleven year bear market in stocks, sovereign debt woes in Europe, zero interest rates, intractable sovereign fiscal deficits, and, yes, the steady rise of gold in all currencies are rooted in the breakdown of confidence in paper currencies linked only to political agendas.

Since the demotion of gold to non-monetary status by the Nixon administration in 1970, fiat money and credit based upon it have been a fundamental source of global wealth generation. What is the value in real terms of the $200T of wealth denominated in currency if nobody wants the paper?

In golf parlance, a "mulligan" is a second chance to make good on a bad tee shot. Mulligans are routinely granted and gratefully accepted by every golfer at the beginning of a friendly match, after a bad first shot. In the world of investing, second chances, or "do overs" are not routine. Sideline huggers who have missed the bull market of a lifetime must "pay up" if they wish to participate in a long-established trend. Late to the party entry points are inherently more risky, as the sharp correction in bullion during the last week of August in bullion illustrates.

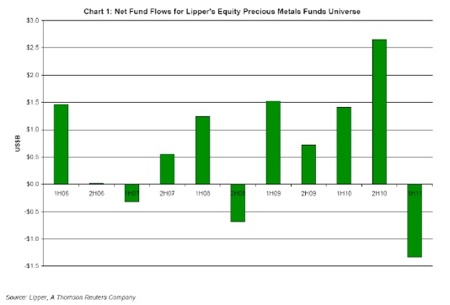

What follows is a table thumping, categorical, endorsement of gold and precious metal mining stocks. It is addressed not only to impatient and possibly dispirited holders of precious metals equities, but also to the bystanders and spectators of the past twelve years. Gold mining equities represent the closest thing to an investment mulligan as we have seen—a rational way to participate in what appears to be the end game for paper currencies on an attractive risk adjusted basis. Gold bullion is popular. Gold stocks are not. Gold bullion has become volatile. Gold stocks remain somnolent. The two have diverged widely over the past eight months, with gold rising 29.2% while the stocks (basis XAU) have declined 2.7%. Since the 1999 bear market low in bullion, the XAU has underperformed the metal by 331% or 13% per year. Based on Lipper data, precious metals mutual fund outflows during the first half of 2011 were the largest in five years:

Reasons for Underperformance

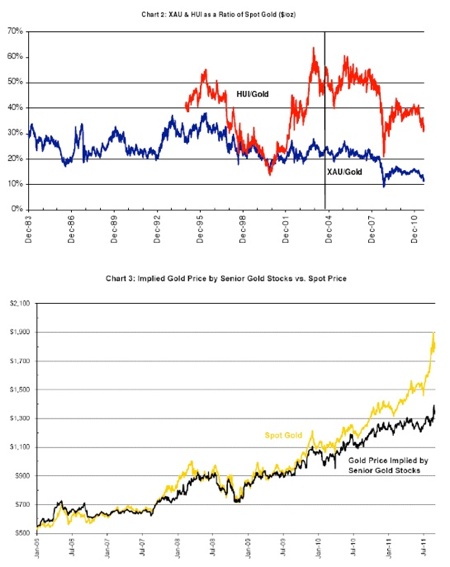

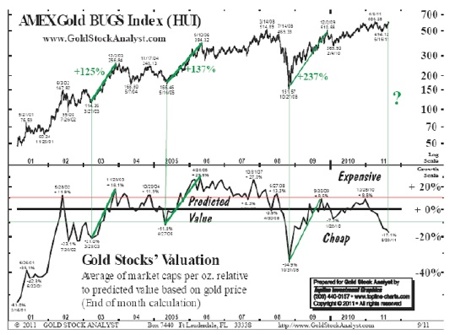

Over the past ten years, the miners, as measured by the XAU, have barely kept pace with the metal itself. Since early December 2010, gold stocks have lagged the metal substantially. The ratio of the XAU (Philadelphia Stock Exchange index of gold and silver stocks) to the metal price stands near an all time low (see Chart 2). The same can be said of the shorter-lived HUI. The basket of senior mining equities monitored by our research team to the NPV (net present value) shows a similar result. This universe implies a gold price of $1372/oz, a discount of 27% to spot (as of 9/6/11), versus a five-year average of -4%.

The chart below, another measure of the unpopularity of gold stocks, tracks the discount to spot prices implied by the trading level of our index of senior gold mining equities:

Gold ETFs

In November 2004, the World Gold Council launched a gold ETF (GLD) which now has a market cap of $72 billion (B). GLD is backed by physical gold and has tracked the gold price accurately. Other gold ETFs have been launched and today the aggregate market cap is $130B, compared to an estimated market cap for gold mining equities of $500B. Chart 2 shows that the valuation of the XAU relative to the bullion price began to trend lower in the years following the launch of GLD and other gold ETFs.

It appears that the gold ETFs have been a mixed blessing for gold mining stocks. On the one hand, by making gold more user-friendly, ETFs facilitated capital flows into the metal. By making gold available to mainstream investors, they democratized what was previously an obscure asset known only to central bankers, commodity traders and coin dealers. The ETFs have had a positive, but difficult to measure, impact on the gold price. In all likelihood, and with 20/20 hindsight, this impact was probably marginal. Who is to say that given the macroeconomic tail winds for gold, that the price would be any different today in the absence of the gold ETFs? On the other hand, gold ETFs have created competition for gold mining stocks, and this seems to be reflected in Chart 2. Prior to 2004, the miners held a monopoly for equity market investors wishing to bet on a decline in the value of paper currency. This monopoly translated into an extremely low cost of capital for the gold mining industry. Unfortunately this advantage was dissipated by industry management during the 1990's and through 2007 by way of excessive share issuance, unwise capital allocations, and risky hedging practices which ultimately resulted in the destruction of shareholder capital.

Relative to gold mining equities, investment in the metal is straightforward and clear cut. There is no business risk. Investing in the business of mining gold demands more complex and specialized analysis. Given the flight to safety in capital markets, it is not surprising that investors flock first to bullion.

Doubts on Gold Price

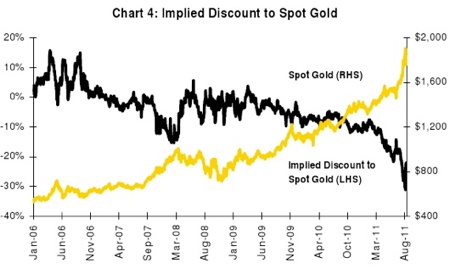

The hesitancy in gold stocks year to date reflects the reluctance of investors to incorporate higher gold prices into earnings and dividend expectations. The steep acceleration in the slope of gold prices over the past 90 days and related volatility is a near term negative because the natural expectation is for the metal price to correct. A correction in the metal price might give equity investors the confidence to project and normalize new and previously unexpected fundamentals. The steep discount to the current spot price of $1872 (-27%) (Chart 4) indicates a level of skepticism not seen since 2008.

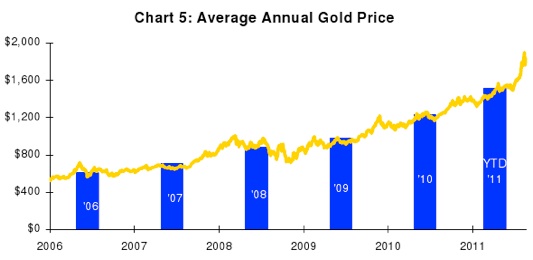

The rationale for investing in mining stocks is purely and simply a bullish view of the gold price. However, the fundamental that drives earnings is not the spot price but the average price over a period of time. As the chart below shows, the average annual gold price is in a steadily rising and bullish trend. This trend is a more reliable gauge of industry profitability than spot prices. Since the average price received is well below (-26%) the spot price, and the moving average is still climbing, we expect the best is yet to come for gold mining earnings.

We also expect the price behavior of gold to become ever more astonishing. As long as favorable macroeconomic conditions prevail, especially negative real interest rates, marginal capital flows into the metal will have an outsized impact on the metal price. The reason is that the available supply of investment gold increases slowly while the quantity of paper currencies and sovereign debt proliferates at comparative warp speed. The addition to the above ground gold stock of 170,000 metric tons from annual mine production is only 2,698 metric tons or 2%. $100 swings in the daily price are likely to become routine. Those who view the metal's price as a vehicle for trading profits will in all likelihood fail to capture the full return from the substantial and permanent devaluation of paper currencies against it. The record of the high profile pundits in calling short term tops and lows in the price action is abysmal. We graciously do not reproduce any of their inaccurate calls as evidence. It raises the question of why anyone would want to trade in the midst of a tectonic shift in global monetary arrangements.

The basis for expecting sustained high gold prices is the erosion of confidence in central banking and fiscal and monetary policy in Western democracies. Low esteem for paper currencies has the appearance of permanence. Reclaiming confidence in paper currency will be no easy task. The challenge was discussed in our previous web site article: Another Volcker Moment At Hand? Until confidence is restored, there will be no substitute for gold. Once the point of no return for confidence in fiat money has passed, there is no self-correcting market mechanism to drive down the price of gold. Gold is unique in this respect. Unlike the price of oil, base metals, grains and other economically sensitive commodities, its price is not restricted by conventional market forces.

Margin Pressure

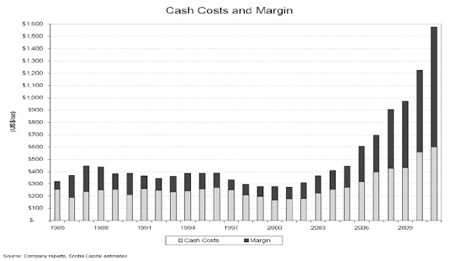

Pressure on gold mining margins is often mentioned as a reason for lackluster stock performance. However, the facts do not support the argument. In 2007, oil prices approached $150/Bbl, and today are hovering in the mid $80's. Energy, one of the key variable cost components of producing gold, has not kept pace with the gold price. Almost all of the others that one could name, including steel, chemicals, rolling stock and labor have not kept pace either. Given a world economy that seems to be stuck in perma-mud, we do not see input costs becoming problematic. Should inflation accelerate due to monetary laxity, we would expect the gold price to continue to outpace variable costs. The chart below shows that the spread between the global cash cost of producing gold has widened significantly since the watershed of 2008:

Prior to 2008, margin pressure was a legitimate concern. The costs of producing were outrunning the gold price. Skinny margins translated into high potential shareholder dilution if the industry was to reinvest sufficient capital to maintain production and reserves. Following the credit implosion of 2008, profit margins on existing mines have steadily expanded.

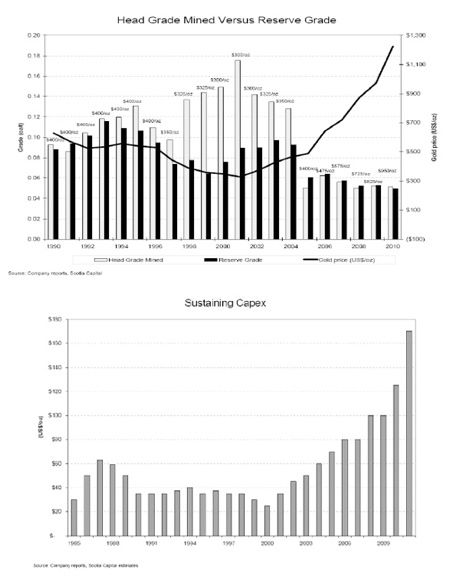

If there is a legitimate margin/return on capital issue, it relates to mines of the future. The steady decline in head grades requires disproportionate and possibly geometric increases in capital to produce the same volume of gold. More capital translates into heightened project risk. Companies that choose to avert dilution in favor of cash distributions on highly profitable existing assets are more likely to find favor with investors and will be rewarded in terms of equity valuation, in our opinion. Those that choose to pursue growth strategies that require capital-intensive new projects in risky political jurisdictions may well fail to achieve the privileged equity valuations that we envision for those that don't.

Resource nationalism directly impacts the economics of existing and future mines. The term is new but the practice of nickel and diming the profitability of successful business in the commodity sector is time honored. Host countries, especially those in the developing economies of the world, have honed this practice to a fine art. The issue is most relevant for large, highly visible new mine projects and indisputably adds risk in terms of capital, time and project economics. However, the predisposition of governments to penalize success, especially when soaring commodity prices produce "undeserved" profits cannot be used as an explanation for the recent underperformance of gold mining stocks since it has always been part of the landscape for extractive industries.

Hangover from 2008

It goes without saying that mining stocks are riskier than the metal itself. Periods of sustained equity market weakness create drag for gold mining equities, even if the gold price itself is strong or holding steady. The weak equity market in 2011 and 2008 are two recent examples. Bear markets inevitably raise concerns over the viability of a strategy of investing in gold mining stocks. Investors in gold bullion are for the most part risk averse, while investors in gold mining equities are opportunistic or risk takers.

The dreadful performance of gold mining stocks in 2008 in our opinion remains an important negative weighing on the group and an important explanation for their recent sluggishness. Gold bullion rose 5.8% in $US and proved to be the only safe haven other than cash in the instance of asset deflation. Gold mining equities (XAU) declined 27.8% in 2008.

Investors in gold mining stocks during 2008 quite possibly celebrated the unfolding collapse of the credit markets. The premise of their investment was the expectation of the very events that took place. However, despite their foresight, the gold and precious metal share investor lived the same nightmare experienced by all equity market investors. At that time, equity investors meeting margin calls had no time to consider the distinctions between gold mining and other equities. Within the confines of 2008, gold stocks did not insulate against the implosion of credit.

For this reason, in our opinion, they are still viewed with skepticism.

The Case for Gold Stocks

Gold bullion and gold stocks are completely different, similar only in their attraction to investors who distrust paper currencies. Gold is inert. Gold stocks are claims on the enterprise of finding and extracting gold from the core of this planet. Think of them as long term, deep in the money, long duration income producing options on the gold price. Perhaps their suitability is limited to a range of investors narrower than bullion itself. However, for that narrower slice of the investment universe seeking a more dynamic exposure to currency debasement than the metal itself can provide, they are the only game in town.

In terms of potential return, gold stocks have inherent advantages over the metal itself: income, growth, and takeover potential. These three possible sources of return are beyond the scope of physical gold. As obvious as these attributes may seem, they have been periodically over looked.

One possible reason is that the bid for gold is global. It emanates from China, India, South East Asia, and other diverse global locations where gold mining stocks are all but unknown. Aside from speculators in Western capital markets, gold is purchased not for its return potential but rather for its traditional attributes as a safe haven and a store of value. The demand for gold stocks comes mainly from a much narrower base of investors. In the primal scramble for safety, the nuanced advantages of gold mining equities have been heavily discounted. To our thinking, the discount is sufficiently excessive to spell extraordinary opportunity.

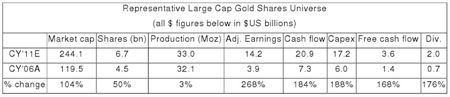

The higher gold price, in our opinion, has transformed our representative universe (see appendix for detail) of large cap gold mining equities from fantasies on the future course of the gold price (2006) to solid value propositions (2011) providing compelling valuations, attractive current returns and a virtually free ride on future gains in the gold price. Our sample universe consists of eleven companies accounting for approximately 40% of global gold production in 2010:

The $14.2B of aggregate earnings is based on the 2011 run rate at $1450 gold/oz, which is slightly below the average gold price received year to date by the industry. The incremental leverage for earnings, cash flow, and EPS for each $100/increase in the gold price is 16%, or 68% at the current gold price of $1872. The gold price has advanced sharply in 2011 and has averaged $1514 year to date versus $1227 in 2010.

The robust level of profitability means that capital structures are healthy and that the threat of chronic share issuance is reduced. Over the past five years, share issuance increased 50% and the economic gains were decisively accretive on a per share basis.

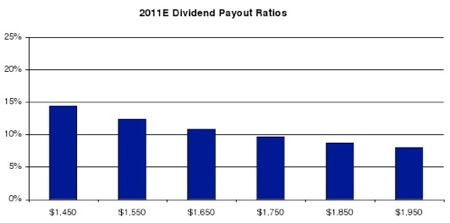

Although dividends have nearly tripled over the past five years, dividend payout ratios are still on the miserly side at 14%, based on $1450 gold. Should gold prices stabilize at $1750/oz, 5% below the current spot price, those payout ratios (as of 6/30/2011) could drop to 10%. The chart below shows the prospective payout ratios for the group at different gold prices:

Newmont Mining has linked its dividend to the gold price (as of 4/7/11), when gold was trading at $1458. For each $100 increase or decrease in the gold price, the dividend increases or decreases $0.20 per share, or $99M. While other leading companies have yet to follow suit, we expect similar announcements to follow once industry management becomes comfortable with gold prices at $1500 or above. Gold is not a growth business. Annual gold production of 2,698 tons has not changed significantly since 1999 despite the strong increase in gold prices. Grades have dropped steadily over the past decade from 0.15 oz/ton to the 0.05 oz/ton (est) in 2010. We believe the larger companies will have limited choices in deploying their free cash flow, other than to increase dividends or to diversify away from gold mining at the risk of losing the premium equity valuations still enjoyed by precious metal producers.

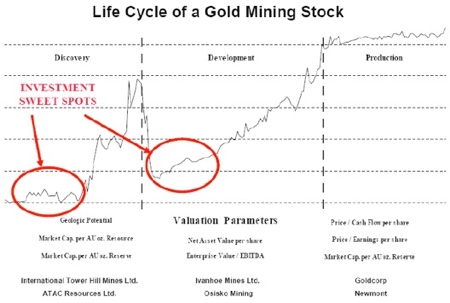

Although gold is not a growth industry, smaller companies routinely grow into larger companies through discovery, mine development or acquisition. Returns generated through corporate development accretive on a per share basis are incremental to the effect of rising gold prices. The most efficient exposure to such returns is to invest in early stage or small cap companies where entrepreneurial success in discovering new, economically significant precious metals deposits, or in developing new deposits into cash flow producing mines can yield quantum increments in per share valuation. Larger cap producers also make significant discoveries and are constantly upgrading their asset mix, but the net impact on overall corporate valuation is typically more muted:

The disconnect between gold bullion and gold equities works both ways. When the metal is rising rapidly, it is not uncommon for the equities to lag. Following peaks in the metal, performance of the equities has often been positive. Gold peaked in 1980, but gold equities peaked nearly a year later. There was a second peak in gold equities, lower than the first peak, but still higher than trading levels in 1980 when the metal itself peaked. Based on this history, we find that the fear that returns from gold equities are circumscribed by peak gold prices is unsubstantiated.

The Gold Stock Analyst chart (9/1/11) shows that returns from investing in gold mining equities are greatest when the stocks trade at a discount to the metal:

Conclusion

Gold mining stocks provide dynamic exposure to rising metal prices, but frequently with a lag. If one believes that the current gold price is sustainable, the historically high discount between the shares and the metal represents a compelling opportunity. The industry, once marginal, is now on solid footing with durable free cash flow. With more enlightened management, decisions on the deployment of free cash ought to result in substantial dividend increases. Mainstream investors agnostic on the prospects for monetary debasement may well come to regard gold stocks as generic yield plays. Quoting Jim Sinclair: "Gold stocks are the utilities of the future." Still ahead is the possibility that gold will be reintegrated into the international monetary system.

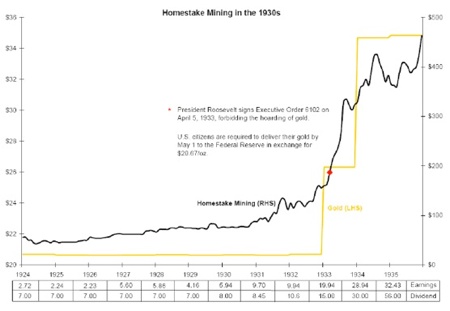

Should desperate governments grasp at this straw, they will have to fix the price of gold at a level sufficiently high for investors to prefer government paper to the metal. While it is hard to imagine a repeat of the Roosevelt administration's confiscation of gold from U.S. citizens on a global scale, it is worth recalling that gold mining stocks benefitted while those who dutifully turned in their coins and bullion did not:

The case for the sustainability of high gold prices rests on whether the present international system of money and banking has passed a point of no return. If Western political leaders and policy makers prove unable to restore credibility to the financial model of the democratic welfare state, a permanent devaluation of paper money against gold will be unavoidable, whether it takes the form of high inflation or a resumption of the gold standard. Either outcome implies political and social changes not currently imagined by the financial markets.

For gold mining equities, the valuation implications would be profound. Resulting earnings would, in our opinion, be supported by permanent, not cyclical change. Multiples of earnings and cash flow would not assume a reversion of the business cycle from peak to trough but on a new international order of credit and banking. For acrophobic investors, paralyzed by the steep advance in the gold price, we believe gold mining equities offer a safety net of valuation and mispriced optionality. It is a second chance well worth taking.

John Hathaway

Portfolio Manager and Senior Managing Director

© Tocqueville Asset Management L.P.

September 6, 2011

This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any projection, forecast or opinion will be realized.

References to stocks, securities or investments should not be considered recommendations to buy or sell. Past performance is not a guide to future performance. Securities that are referenced may be held in portfolios managed by Tocqueville or by principals, employees and associates of Tocqueville, and such references should not be deemed as an understanding of any future position, buying or selling, that may be taken by Tocqueville. We will periodically reprint charts or quote extensively from articles published by other sources. When we do, we will provide appropriate source information. The quotes and material that we reproduce are selected because, in our view, they provide an interesting, provocative or enlightening perspective on current events. Their reproduction in no way implies that we endorse any part of the material or investment recommendations published on those sites.